This is the video recording of our May 3, 2021 Monthly Charts Live Strategy Session

RPP Report: Review. Preview. Profit. (04-26-2021)

From the desk of Steve Strazza @sstrazza

At the beginning of each week, we publish performance tables for a variety of different asset classes and categories along with commentary on each.

Looking at the past helps put the future into context. In this post, we review the absolute and relative trends at play and preview some of the things we’re watching to profit in the weeks and months ahead.

The weight of the evidence still suggests it’s prudent to be a buyer, not a seller, of risk assets for more meaningful time horizons.

Shorter-term, the market looks increasingly messy. For the first time in over a year, defensive assets are beginning to stabilize at logical levels of support, while stocks and major risk groups achieve our upside targets. Even a handful of some key Intermarket ratios are potentially diverging from the broader averages.

The macro backdrop definitely leans that this is just a sideways consolidation in an ongoing uptrend.

Let’s not forget that the S&P 500 has just recorded its greatest 52-week gain since the late 1940s, so some digestion is perfectly healthy and deserved!

RPP Report: Review. Preview. Profit. (04-19-2021)

From the desk of Steve Strazza @sstrazza

At the beginning of each week, we publish performance tables for a variety of different asset classes and categories along with commentary on each.

Looking at the past helps put the future into context. In this post, we review the absolute and relative trends at play and preview some of the things we’re watching to profit in the weeks and months ahead.

The same themes that we’ve been pounding the table on more or less continue to drive primary trends.

In recent weeks, we’ve seen some rotation back into Large and Mega-Caps, which has propelled the major indices to new highs, while SMIDs are still resiliently consolidating. While the list of negative data points has grown, it’s still not close to anything that warrants concern.

Developed Markets, particularly European equities, are resolving higher across the board — a move confirmed by strong breadth and bullish internals. In short, we continue to see strong equity market participation around the Globe.

We’re also seeing signs of another leg higher for the Commodity complex as more positive economic data pours in.

Ultimately, risk markets remain in a healthy state right now.

Global Breadth Is Bullish… But Bifurcated

From the desk of Steve Strazza @Sstrazza and Grant Hawkridge @GrantHawkridge

Following an onslaught of bullish initiation readings for US stocks last year, global equity markets began to register similar breadth thrusts earlier this year.

In this post, we’ll take a look at those thrusts in addition to the current state of international stock market internals.

We’ll even take a quick look at some of the differences we’re seeing take place beneath the surface in various global markets.

Let’s dive into it.

[PLUS] Weekly Market Notes & Breadth Trends

From the desk of Willie Delwiche.

Key Takeaway: New highs bring out the bulls. Excessive optimism offset by broad market strength in the US & around the world. Despite Fed assurances of patience, rising bond yields will soon put pressure on the liquidity backdrop.

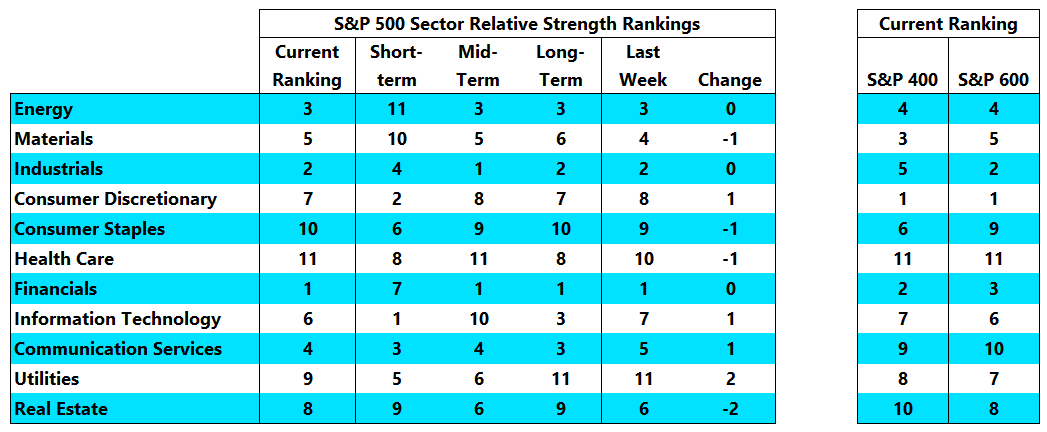

Their short-term performance has been mixed, but our relative strength rankings still have Financials, Industrials and Energy holding down the top spots. The still unanswered question from the past few weeks is whether the short-term trends (e.g., Technology in the top spot, Energy in the last spot) represent the beginning of sustainable shifts in leadership or are part of the process of digestion after longer-term trends moved too far in the other direction. A similar question presents itself when looking at the industry group heat map. Small & mid-cap groups dominate the top of the rankings, but large-cap groups appear to be on something of an upswing.

[PLUS] Weekly Market Notes & Breadth Trends

From the desk of Willie Delwiche & Ian Culley.

Key Takeaway: The overall market continues to digest gains within a larger structural advance. Market sectors that relate to tangible goods push to new highs. Traditional safe-haven assets fail to ensure safety.

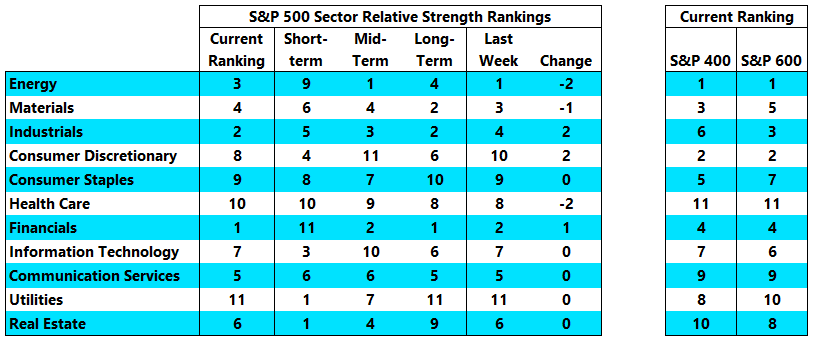

Financial, Energy, Industrial, and Material sectors continue their reign in our relative strength rankings, while mid-cap groups narrowly surpassed small-caps to command the top-tier of our industry group rankings. Though more defensive sectors continue to have the best relative strength on a short-term basis, Technology and Consumer Discretionary are starting to pick up in the near term as well. Small-cap deterioration persists at the industry group level, whereas large and mid-caps improve.

[PLUS] Weekly Market Notes & Breadth Trends

From the desk of Willie Delwiche.

Key Takeaway: Even with bottlenecks & distortions, economic recovery & cyclical rally remain intact. Tactical risks have risen as the market digests gains of last year. Watch bond yields & global participation for evidence that the rally is ready to resume.

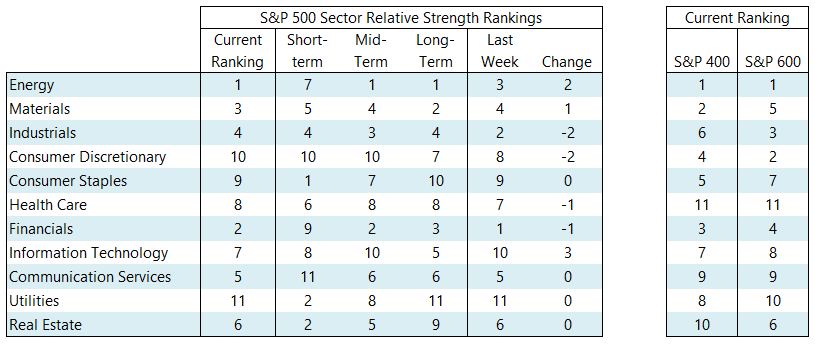

Cyclical value sectors remain the leaders in our relative strength rankings and small-cap groups continue to dominate the upper-tier of our industry group rankings. But there is evidence beneath the surface of shifting trends. Rather than seeing a reversion back to growth leadership in our sector rankings, we are seeing defensive areas of the market start to heat up. Consumer Staples, Utilities & Real Estate have the best relative strength on a short-term basis. At the industry group level, small-cap groups are deteriorating while large-cap groups are improving.

[PLUS] Weekly Market Notes & Breadth Trends

From the desk of Willie Delwiche.

Key Takeaway: Small-caps hit pause but remain market leaders. Another breadth thrust shows rally participation remains robust. Bond yields are digesting recent rise, but the path of least resistance remains higher.

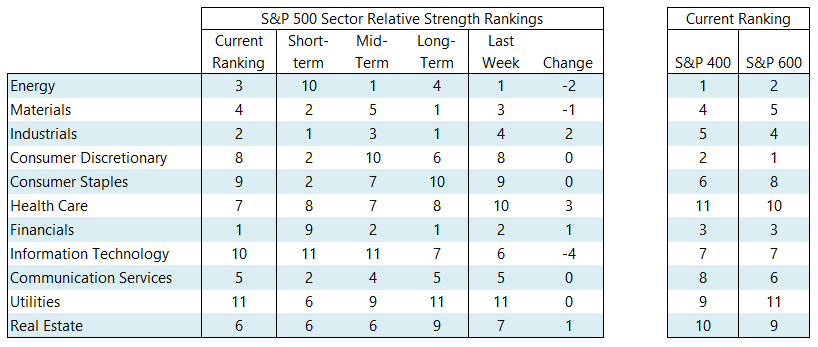

The Technology sector continued its descent toward the bottom of the relative strength rankings. It dropped to its lowest ranking since mid-2016 and fell out of the sector leadership group (which based on a three-week smoothing of the current ranking) for the first time in two years. Technology is joined in the cellar by Utilities, Consumer Staples and Consumer Discretionary. Cyclical value leadership remains intact. Even though small-cap groups led the way lower last week, our industry-group rankings continue to show leadership from small-caps and mid-caps.

- « Previous Page

- 1

- …

- 17

- 18

- 19

- 20

- 21

- …

- 34

- Next Page »