Dynamic Portfolio Update: With the weight of the evidence improving, we are putting some cash to work in the cyclical portfolio while also staying well-positioned for opportunities from a tactical perspective. In both portfolios we are leaning toward strength that we are finding in equities beneath the surface and beyond our borders.

Weekly Market Notes: Bull Market Behavior

From the desk of Willie Delwiche.

The number of stocks making new lows remains negligible. Last week, the number of stocks making new 52-week highs on the NYSE + NASDAQ surpassed a number of prior peaks (Dec 2021, Apr 2022, Nov 2022). It’s now at its highest level since November 2021.

More Context: Everyone has their own definition of a bull market. For me, it’s when more stocks are making new highs than new lows. Bear markets tend to end when new lows drop below new highs. Bull markets are sustained when new high lists expand. We are seeing that now among individual stocks and we are seeing that at the industry group level (especially outside of large-caps). In moving from 2022 to 2023 we have transitioned from broad weakness to broad strength. Big day-to-day price swings haven’t gone away, but after volatile years (like we experienced last year) that can be slow to ebb. Most of the strength that looks sustainable is happening beneath the surface of the popular benchmarks or beyond the borders of our country. It’s a new year with new opportunities, but that doesn’t mean the market will make it any easier.

In our Market Notes, we review the evidence of strength we are seeing and where we are seeing leadership and opportunity among US equities.

[PLUS] Weekly Observations & One Chart for the Weekend: Rally Gets a 5-Star Review

From the Desk of Willie Delwiche.

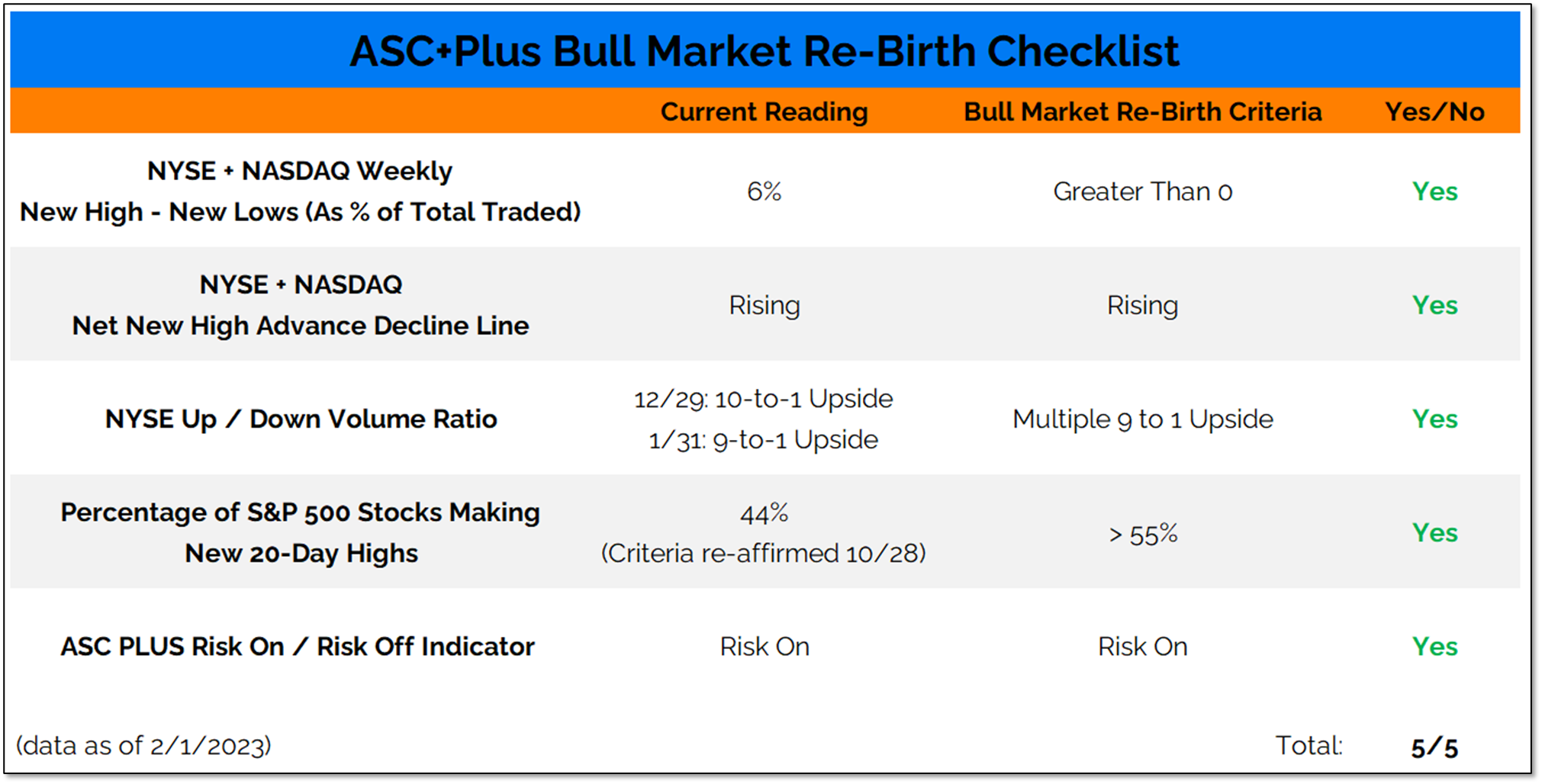

After Tuesday’s 9-to-1 upside volume day, our Bull Market Re-Birth Checklist is now five out of five.

Why It Matters: The conditions for a new bull market have been met. It’s hard to argue otherwise from a market perspective. Large-cap and mid-cap value indexes reached new all-time highs this week, and small-cap value is not too far behind. The trend for the market for the market is higher, even if not all the indexes (including the popular benchmarks) are trending higher. But when the trend is higher, leadership is evidence of opportunity.

Our Bull Market Re-Birth Checklist has served its purpose well. But it is now time to put it aside and now turn our attention to questions of sustainability and leadership. These will be best answered by price and breadth trends and not one-off surges and thrusts. We will be aggregating some of the key indicators in this regard and introducing a new bull market sustainability checklist next week. Stay tuned.

[PLUS] Weekly Town Hall w/ Willie Delwiche

This is the video recording of the February 2nd, 2023, Weekly Town Hall w/ Willie Delwiche.

2/2/23 2:00 PM ET [Read more…]

[PLUS] Weekly Sentiment Report: Unwilling To Abandon Equities

From the desk of Willie Delwiche.

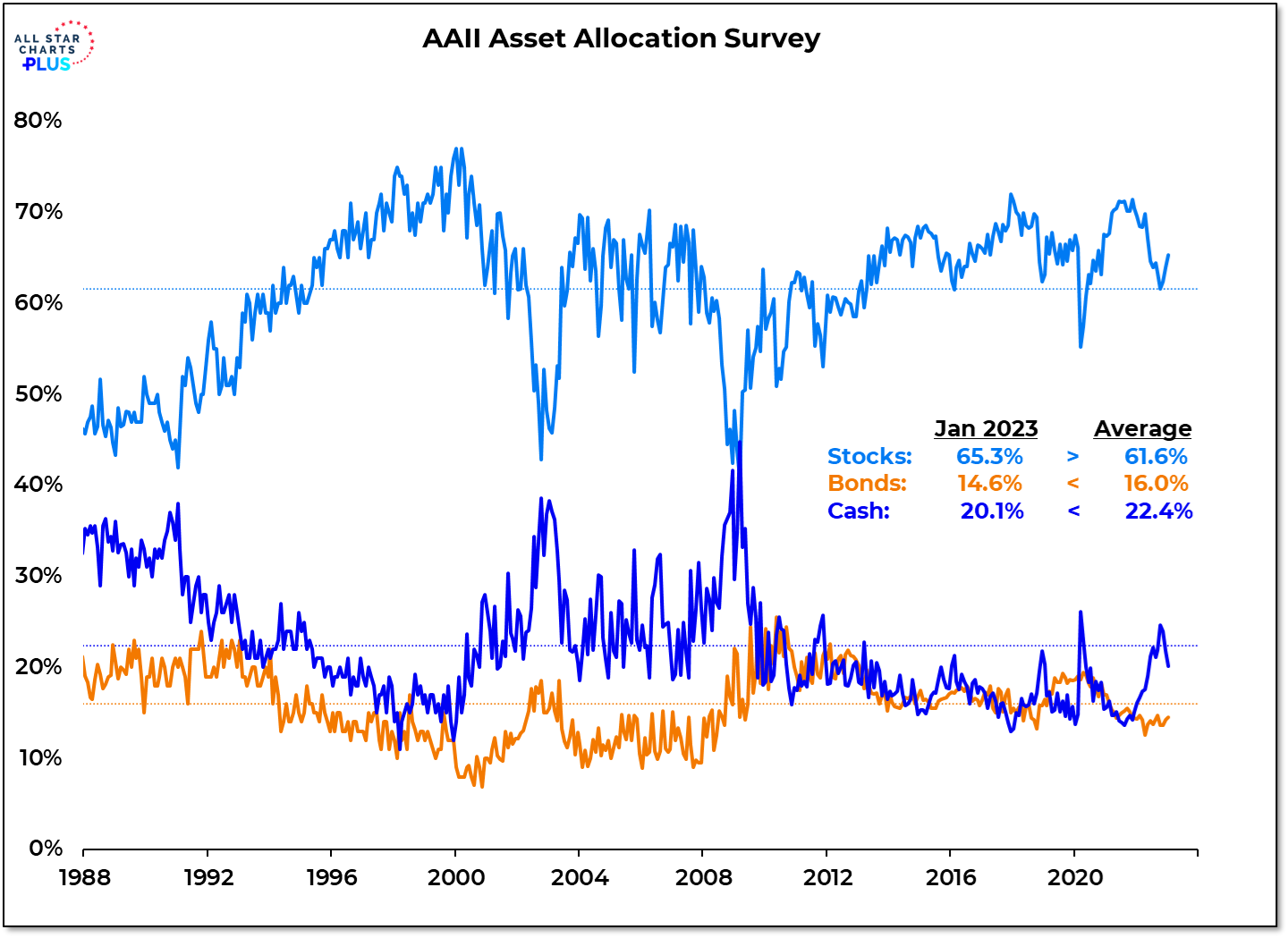

The January AAII asset allocation survey shows household equity exposure rising for the third month in a row and climbing to its highest level since May.

Why It Matters: Despite last year’s stock market turmoil and claims of pessimism, investors did not abandon equities. After approaching a 20-year high in November 2021, stock exposure waned over the course of 2022 but never did drop below its long-term average. Historically, the best gains in the market come after investors become bearishly positioned (stock exposure down and cash exposure elevated). That is a pivot that has not taken place this cycle (not yet, at least). The under-owned and unloved asset classes remain bonds and cash (and commodities, which don’t even make it as a category in the AAII survey).

In this week’s Sentiment Report we take a closer look at the implications of this positioning data, how investors are responding to stock market strength this year and what valuations tell us about risk and opportunity in the current environment.

[PLUS] Weekly Market Perspectives – Risk Appetite Returning

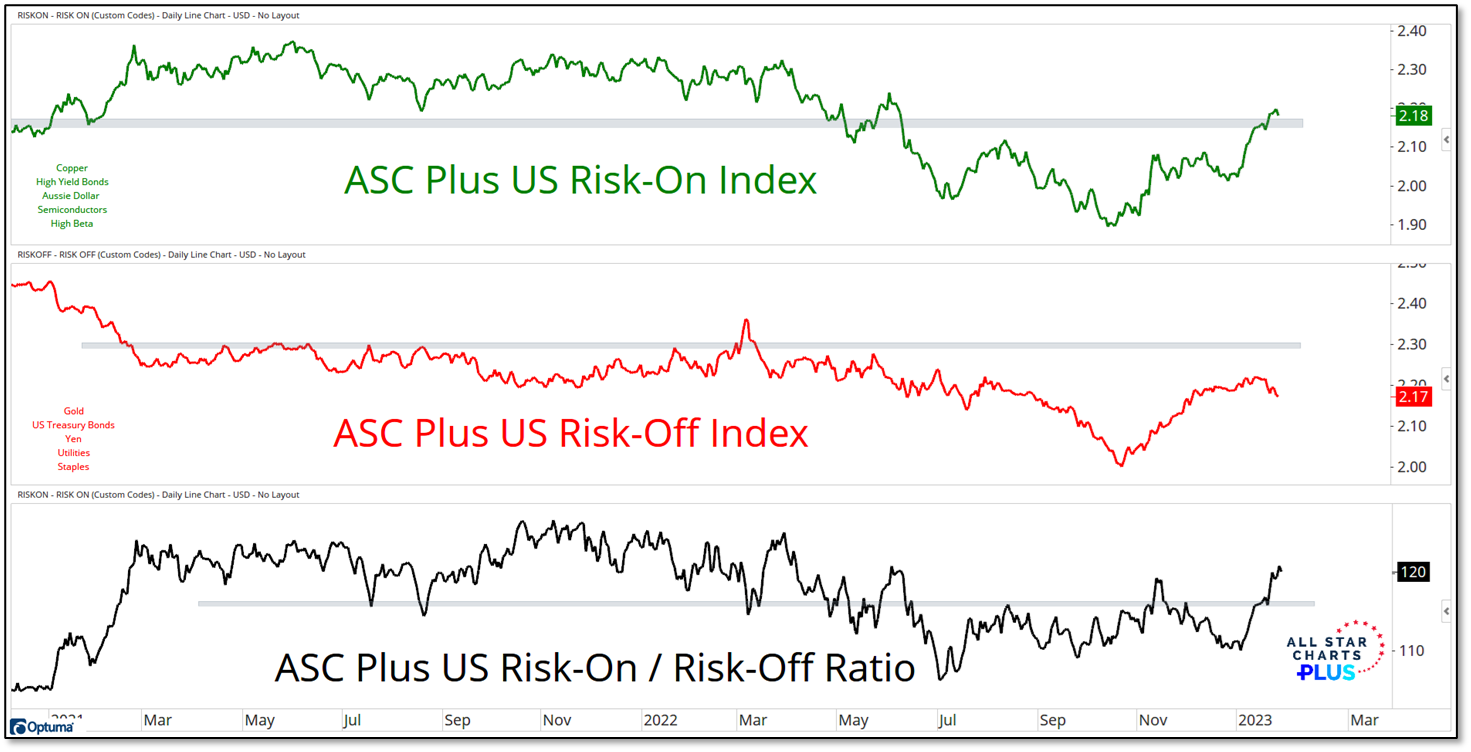

Both our Risk On Index and our Risk On and Risk Off (RO/RO) Ratio have climbed to their highest levels since early last year and in the process crossed back above key levels that provided support during 2021 but were violated as conditions deteriorated in 2022.

Why It Matters: After an unprecedented combination of volatility and weakness in 2022, we are looking for evidence that the strength that has been seen in January marks a sustainable departure from last year and not just more of the same. There is still work to be done from a longer-term trend perspective and macro questions linger. Unlike the rallies that emerged and faded in 2022, however, this year’s gains are being accompanied by more appetite for risk. As long as the Risk On index and the RO/RO ratio are showing improvement (and that improvement is being confirmed elsewhere) it is probably premature to lean against the strength we have seen. That being said, not all opportunities are created equally. Rather than trying to anticipate a turn we are most interested in following the trends that have turned higher. The strength of a move is ultimately revealed on the test.

Inside we take a Deeper Look at our Risk indexes, areas of potential improvement that would confirm recent strength and what one of the best January’s ever for the EAFE could mean for the remainder of 2023.

Weekly Market Notes: A Pivotal Level, A Pivotal Week

From the desk of Willie Delwiche.

2023 is on the cusp of producing as many days with new highs greater than new lows in its first month as 2022 produced over the course of the entire year. Yet there are hurdles to overcome to convincingly argue that this recent strength is sustainable.

More Context: From a macro data and Fed policy perspective, this week holds the promise to be pivotal. That is no less true from a price perspective. More stocks making new highs than new lows is bull market behavior. The S&P 500 not clearing its December high (in the context of still declining longer-term trends) is not. In addition to further trend improvement, renewed expansion in the number of stocks making new highs and continued recovery in our industry group trend indicator would be evidence of rally sustainability. Our equity models aren’t waiting for “what ifs” and while the S&P 500 is an option, it’s not the only one. Our equity positioning is increasingly outside of the US and away from large-cap growth stocks.

In our Market Notes, we take a closer look at longer-term price trends, recent breadth improvements and paradigm shifts that are taking place within global equities.

[PLUS] Weekly Observations & One Chart for the Weekend: What’s Old Is New Again

From the Desk of Willie Delwiche.

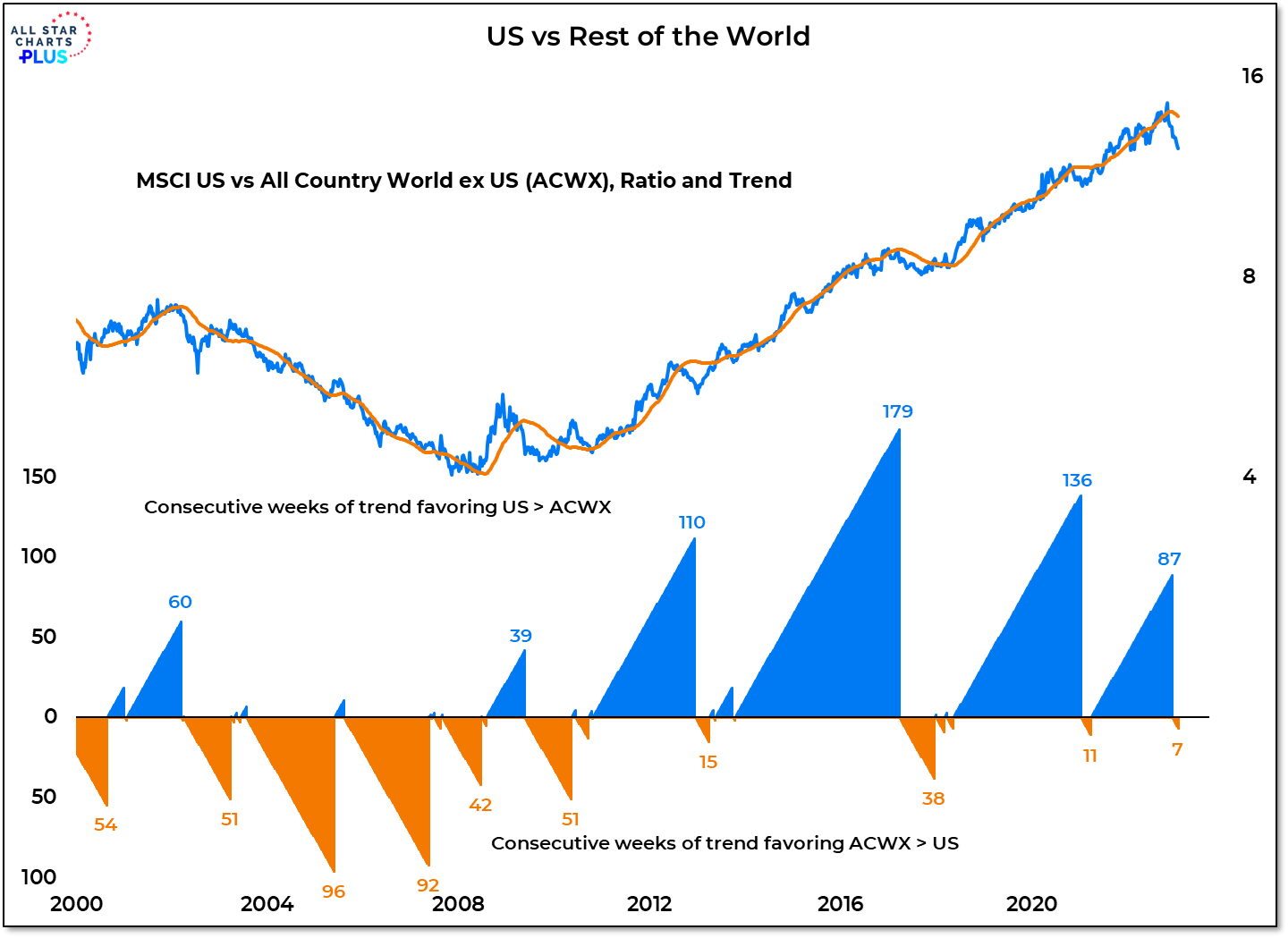

The last decade-plus has featured extended periods of US leadership and only brief bouts of with the rest of the world on top. While it may be outside of the experience or active memory for many investors, the first decade of this millennium saw the exact opposite: persistent strength from the rest of the world and little leadership from the US.

Why It Matters: When it comes to global equity exposure, diversification has been a dirty word for a decade. US investors have not been rewarded for looking overseas. Now that is changing. Absolute uptrends are more common right now outside of the US than within our borders. Our asset allocation model that uses the ACWI (60% US) as a benchmark is near max underweight equities (versus bonds and commodities), while a version that takes the US out of the equation is at max overweight equities. Investors are taking notice, with US equity ETFs seeing outflows and foreign equity ETFs experiencing a surge in inflows. The paradigm is shifting and investors are getting on board.

- « Previous Page

- 1

- 2

- 3

- 4

- 5

- 6

- …

- 80

- Next Page »