This is the video recording of the January 26th, 2023, Weekly Town Hall w/ Willie Delwiche.

1/26/23 2:00 PM ET [Read more…]

Expert technical analysis of financial markets by JC Parets

This is the video recording of the January 26th, 2023, Weekly Town Hall w/ Willie Delwiche.

1/26/23 2:00 PM ET [Read more…]

From the desk of Willie Delwiche.

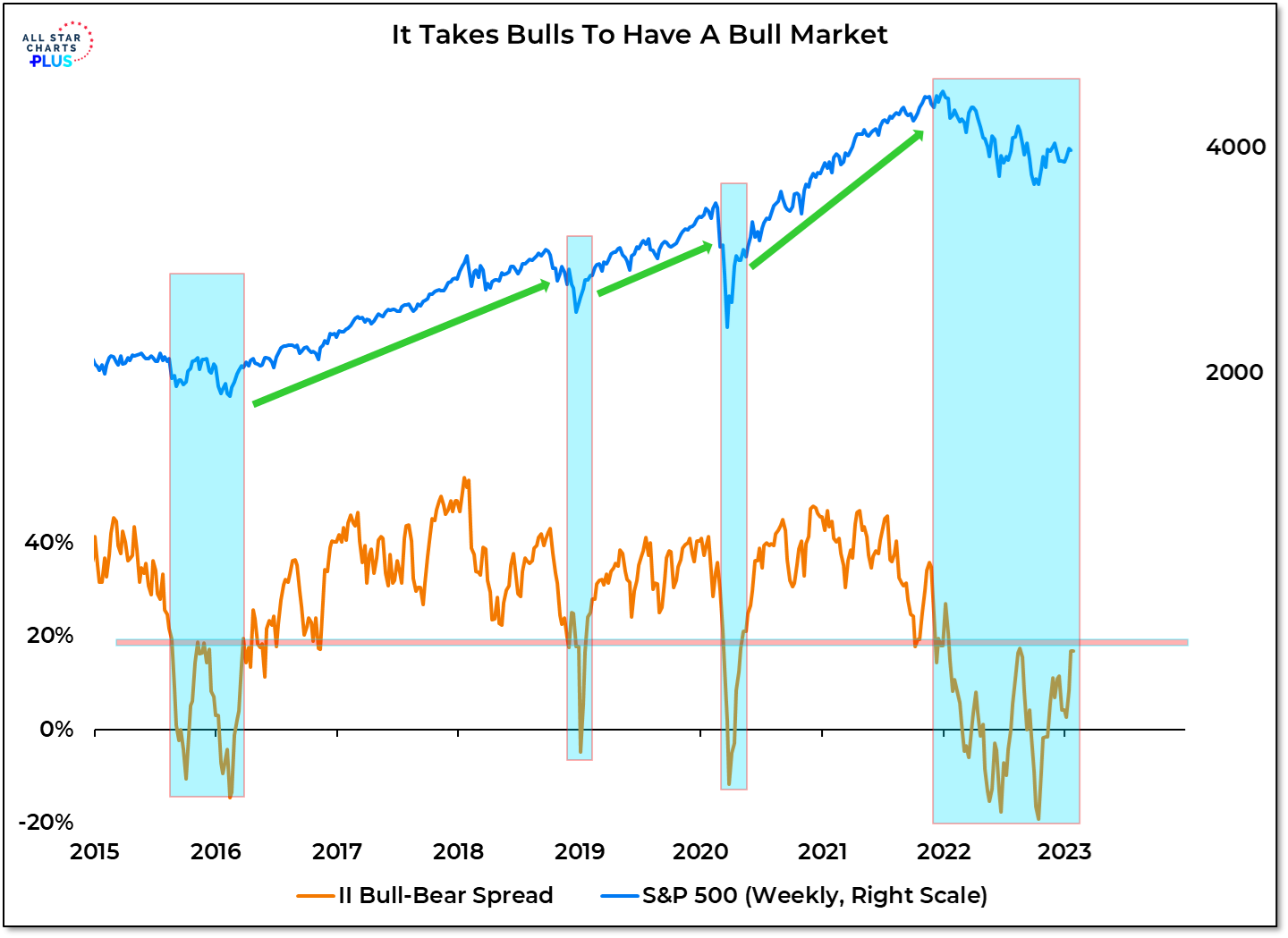

The Investors Intelligence Bull-Bear Spread was unchanged last week, remaining just beneath the level that in the past has signaled full embrace of equities and the opportunity for sustained stock market strength.

Why It Matters: Excessive optimism can signal elevated risks for equities, but since 2015, virtually all of the net gains for the S&P 500 have come when II bulls have exceeded bears by 18% or more. For the past two weeks the spread has been stuck at 16.9%. The absence of bulls and a sustained re-building in optimism over the past year have been a headwind for stocks. The shift from excessive pessimism to elevated optimism is typically when stocks do their best, but this cycle investors have been slow to embrace rally attempts. With stocks strong out of the gate to start 2023, the lack of optimism is notable. If 2023 is not going to follow the path of 2022, investor attitudes about stocks will need to change.

In this week’s Sentiment Report we take a closer look at why investors have been slow to embrace stocks and why it’s important that they do so, sooner rather than later.

Incoming economic data has been weaker than expected but our Macro Health Status report suggests the market is looking past current risks to brighter days – or perhaps it’s just whistling past the graveyard.

Why It Matters: On its surface, incoming data is consistent with recession. Aggregate hours worked in the economy are shrinking, real retail sales and industrial production are contracting and housing market activity remains a shambles. The Leading Economic Index from the Conference Board is signaling that a recession is on its way – and it has an unblemished record in this regard. But we are not seeing evidence of building stress across our macro indicators. The longer the incoming data disappoints and the longer the Fed feeds the economy a starvation diet of liquidity (M2 is declining at a never before seen pace), the harder it will be for the market to focus on a better tomorrow without a further reckoning of currently challenging conditions. The key from the perspective of our Macro Health report is which happens first: more green lights (indicating improvement) or more red lights (indicating deterioration).

Inside we take a Deeper Look at each of the macro indicators in our health status report, what they are currently signaling and where they might be going.

The S&P 500 has rallied off of its October and December lows, but the 200-day average, which rolled over in April 2022, continues to fall.

More Context: Price trends matter. Over the past 2+ decades, all of the net gains for the S&P 500 have come when the index’s 200-day average has been rising. When the trend has been falling, the index has struggled to keep its head above water. While stocks have begun 2023 in rally mode, they are still fighting a downtrend. Stocks can rally within persistent downtrends. But if stocks keep rallying, down-trends cannot persist. The math just doesn’t work. While we are seeing evidence of a tactically more constructive environment, the longer-term trend backdrop remains challenging. The recent strength has a better shot at being sustained if it can flip some of the longer-term trend indicators to a bullish setting.

In our Market Notes, we take a closer look at longer-term price trends, recent breadth improvements and paradigm shifts that are taking place within global equities.

From the Desk of Willie Delwiche.

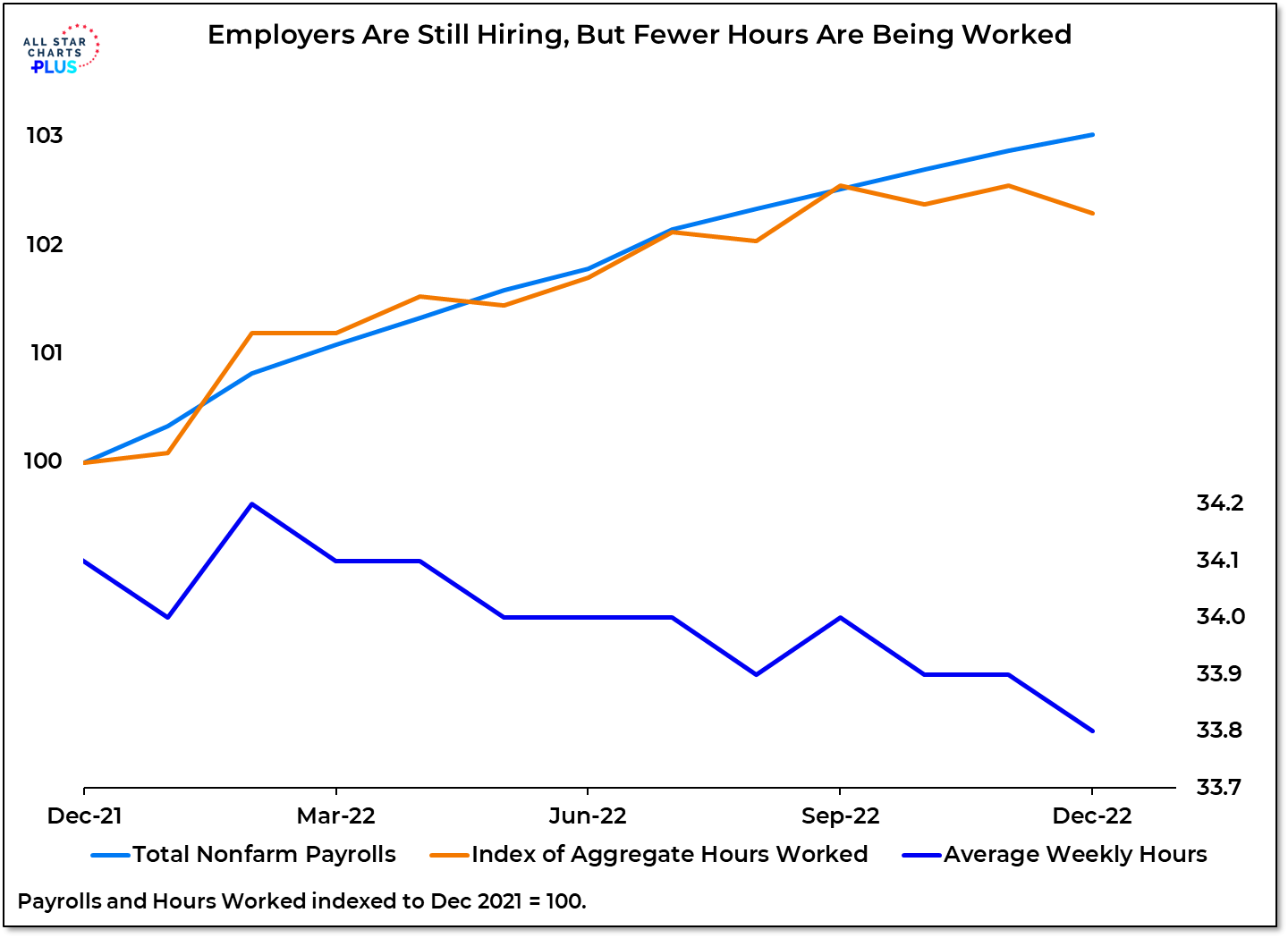

Firms are still hiring but with average weekly hours being curtailed, aggregate hours worked appear to have peaked in Q4.

Why It Matters: Talk of a soft landing has intensified, but the data paint a different picture. Real spending peaked in Q1. Housing starts in Q2. Industrial production in Q3. Payrolls are still expanding and layoffs are near historically low levels. Given the structural imbalance between unfilled jobs and unemployed workers, those metrics are unlikely to be useful indicators of what lies ahead for the economy. Don’t even start with the unemployment rate, which has long been considered a lagging indicator. Rather than firing workers who were hard to hire in the first place, firms are keeping their payrolls largely intact. They are responding to softening demand by curtailing hours worked. Payrolls and initial jobless claims are noise in this environment. The news is that the economy is weakening, inflation is lingering, and the Fed is still raising rates.

This is the video recording of the January 19th, 2023, Weekly Town Hall w/ Willie Delwiche.

1/19/23 2:00 PM ET [Read more…]

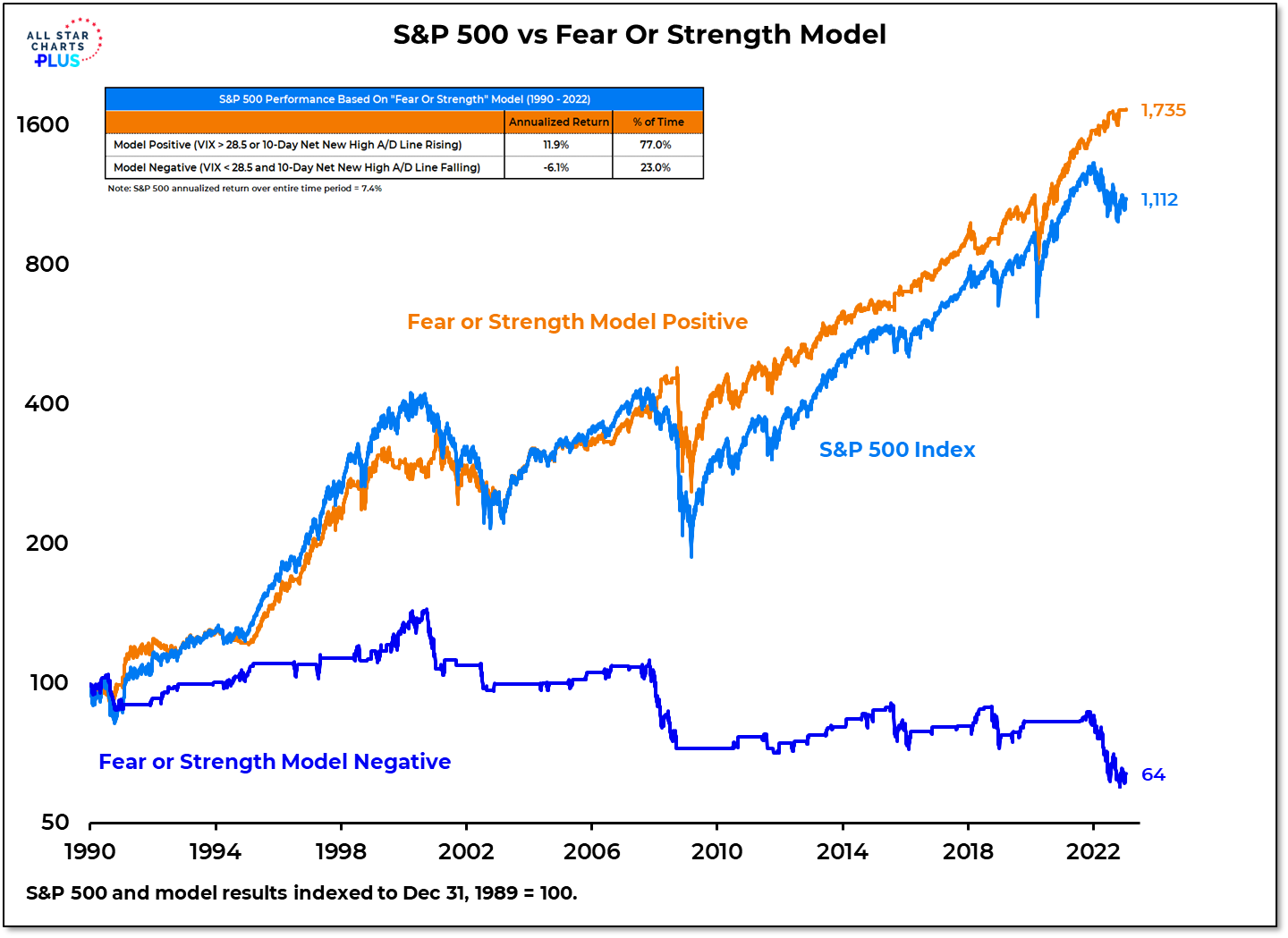

Dynamic Portfolio Update: With new highs outpacing new lows every day so far this year, our net new high A/D line has turned higher and moved our “Fear or Strength” tactical model into its bullish zone. We are following the model and increasing risk exposure in the Tactical Opportunity portfolio.

From the desk of Willie Delwiche.

The Investors Intelligence measure of advisory services sentiment shows Bulls rising to their highest level in over a year. Bears have not (yet) undercut their summer lows and the Bull-Bear spread is still just below its August peak.

Why It Matters: We need bulls to have a bull market. This flies in the face of a desire to only see sentiment from a contrarian perspective. The way I learned it, it pays to go with the crowd until it reverses at an extreme. After the persistent and excessive pessimism of 2022 (which was certainly present in word if not deed), the best prospects for a sustained rally at this juncture is for investors to shift their attitudes and embrace stocks. A failure for investors to turn more optimistic at this juncture could hasten a longer-term positioning re-balance. We have gotten hints of that in recent weeks as ETF flows show investors eschewing US equities in favor of international equities and fixed income ETFs.

In this week’s Sentiment Report we take a closer look at where optimism is showing up, where it remains absent and how investors are feeling as earnings season gets underway.