This is the video recording of our March 6th Monthly Charts Live Strategy Session

[PLUS] Weekly Sentiment Report: Higher Rates = Second Thoughts On Stocks

From the Desk of Willie Delwiche

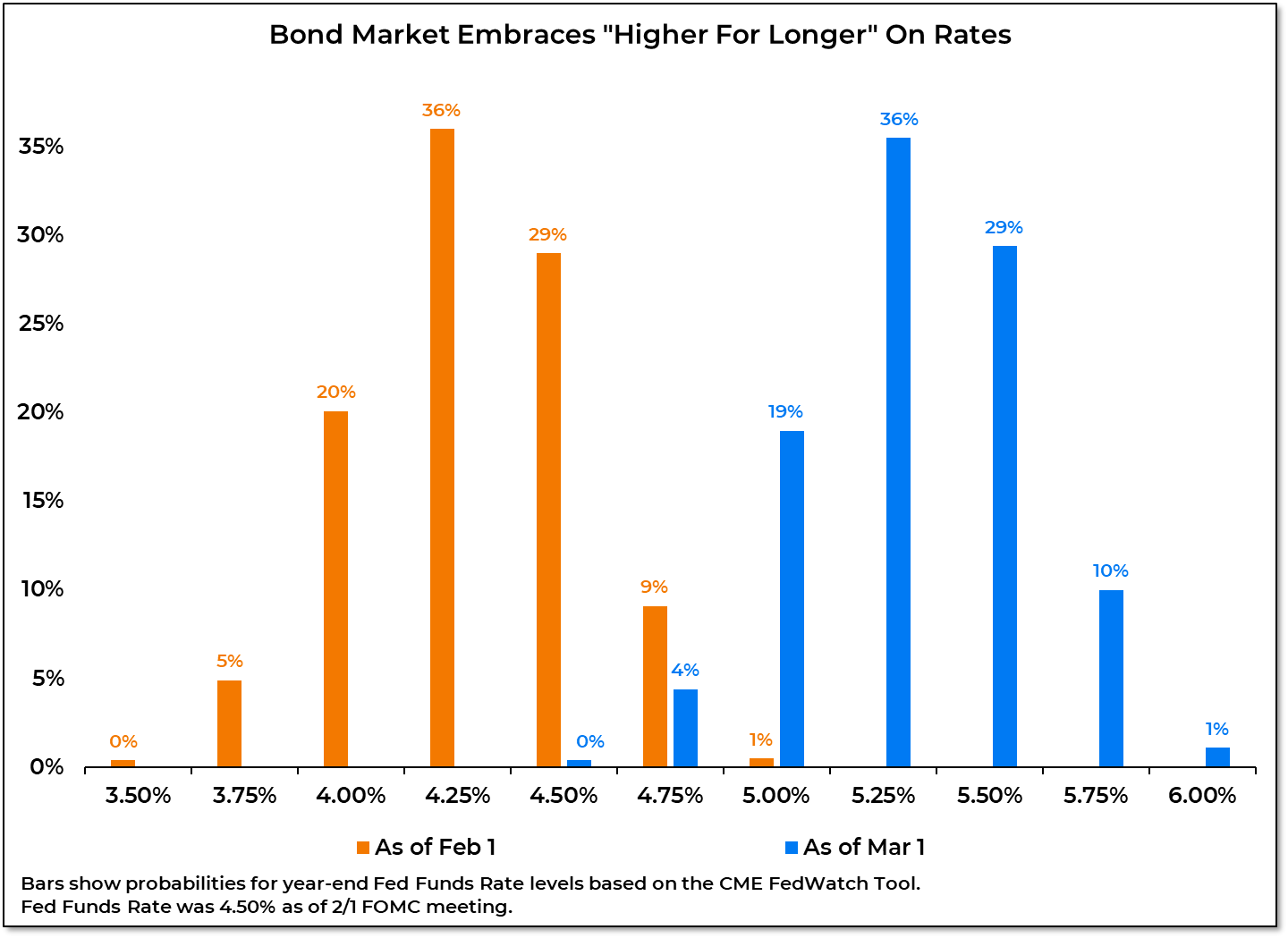

When the Fed raised rates to 4.50% in early February, the market was expecting that any additional tightening this Spring would be taken back (and then some) and that by the end of the year the Fed Funds Rate would be at 4.25%. Now, the market is pricing in a year-end Fed Funds Rate of at least 5.25%. Over the course of a month, market expectations for rates have shifted higher by a full percentage point.

Why It Matters: Stocks stumbled in February as the markets digested the shift in expectations from “rate cuts by the end of the year” to a “higher for longer” reality. This led to investors who had been slow to embrace stock market strength to reconsider recently discovered optimism. We have documented that stocks tend to do well in the wake of persistent pessimism. Under-pinning this analysis is the assumption that pessimism is indeed fading. If expectations for higher rates lead to renewed pessimism, it will be difficult for sustainable strength to emerge. You need to have bulls to have a bull market. As we move into March we see evidence that investors are saying “thanks but no thanks.”

In this week’s Sentiment Report we see that investors are having second thoughts on stocks, how volatility has remained persistent and even with yields still rising, why bonds are relatively more attractive than stocks.

Sell Side Analysts Are Chasing

[PLUS] Weekly Sentiment Report: A Dose of Buyer’s Remorse?

From the Desk of Willie Delwiche

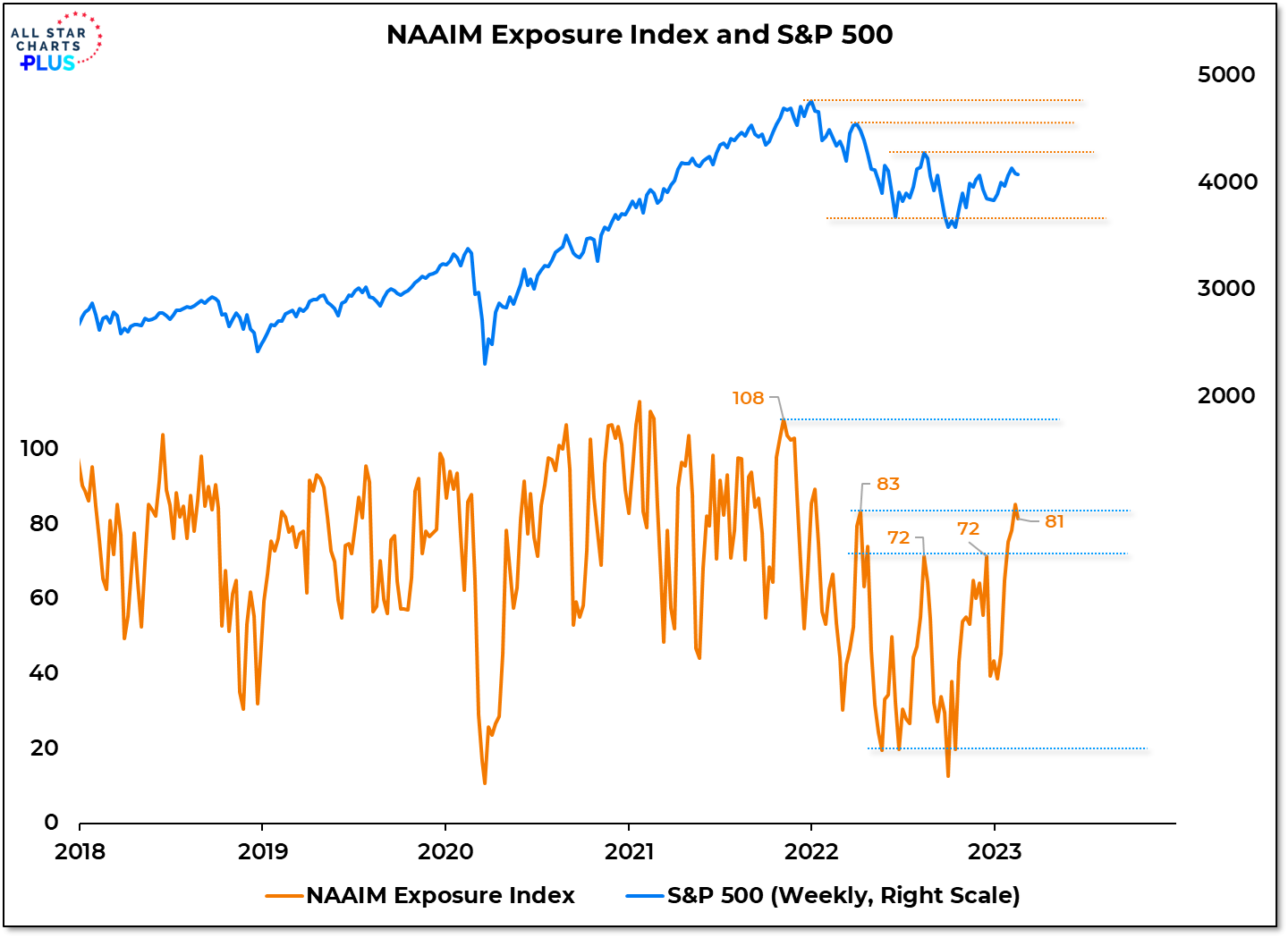

The NAAIM exposure index surpassed its August high last month and has been on either side of its April high over the past two weeks. With price action cooling, active investment managers may regret their eagerness to increase equity exposure.

Why It Matters: Active managers led the recent shift from pessimism to optimism. While sentiment overall doesn’t look ready to boil over at this point, there are some hot spots that could benefit from cooling. The NAAIM data, which has outpaced the recovery in price, is in that category. The broader sentiment risk is that a period of sideways price action leads reluctant optimists to turn bearish again. At this stage in the cycle we need bulls to have a bull market and a return to pessimism would likely add to downward pressure on price. This is all the more likely if volatility remains undiminished (only 4 years in the past quarter century began with more 1% swings in the S&P 500 than we have experienced so far this year) and breadth meaningfully deteriorates.

In this week’s Sentiment Report we take a closer look at how investors have embraced this year’s strength and what could get them to have second thoughts about their recent optimism.

[PLUS] Weekly Sentiment Report: Moving Away From Persistent Pessimism

From the Desk of Willie Delwiche

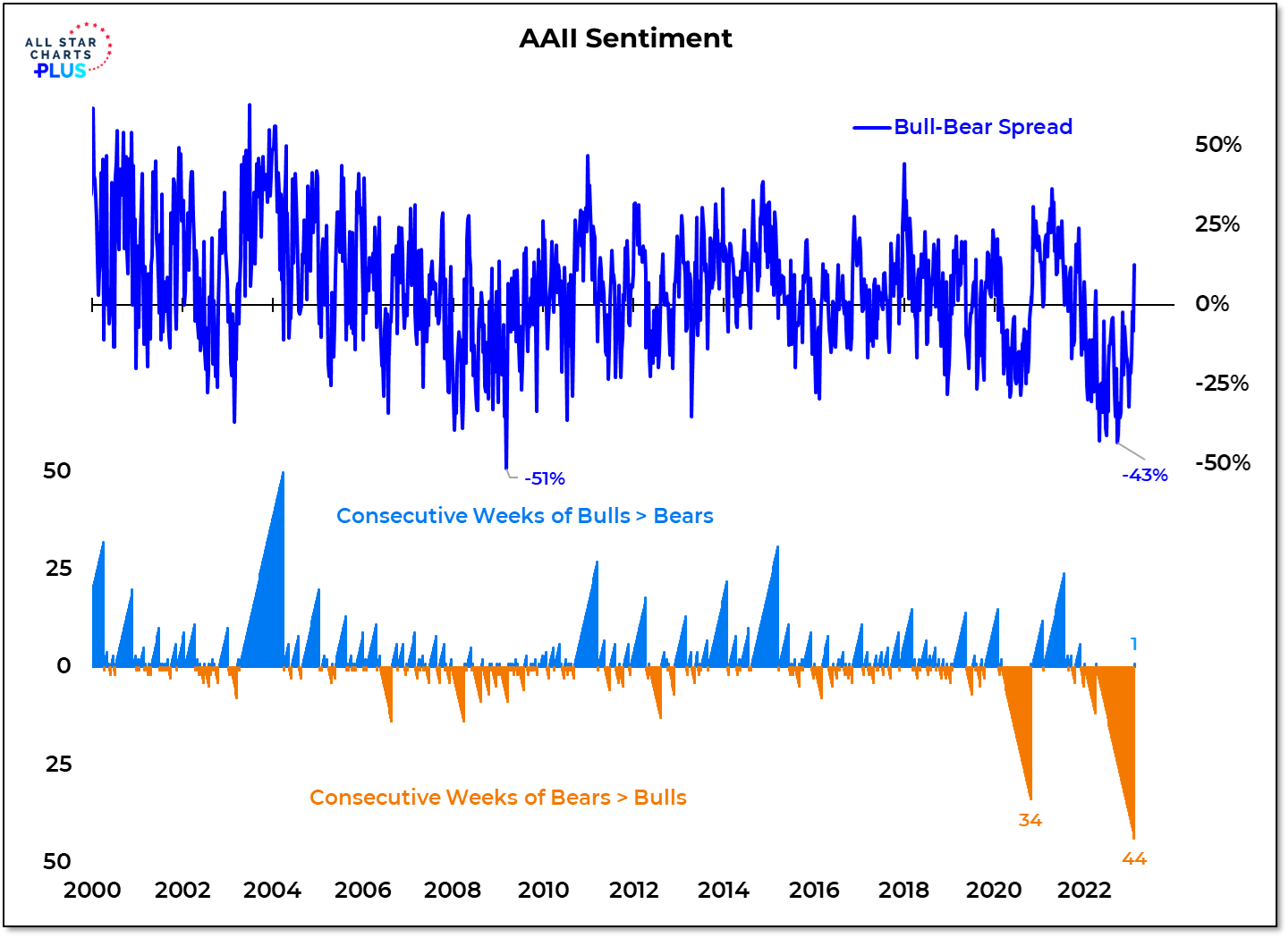

Last week was the first time in 45 weeks that the weekly AAII survey showed more bulls than bears. The most recent stretch of pessimism did not eclipse the Financial Crisis in terms of intensity (the bull-bear spread bottomed last year at -43%, versus -51% in March 2009). But it did set the record for persistence.

Why It Matters: This newfound optimism is leading to some concern that the rally off of last year’s lows has run its course. This is based on the idea sentiment is always best used as a contrarian indicator. Leaning against sentiment tends to be most successful after it has reversed at extremes. The path higher for stocks becomes more clear as bulls replace bears. Rallies that are accompanied by rising optimism tend to be more sustainable. Optimism becomes a headwind after it becomes excessive and begins to fade. While on the watch for excesses, mostly we are seeing investors finally beginning to embrace stock market strength. At this point in the cycle, strength fuels optimism and optimism fuels strength. Increasing optimism after persistent pessimism is a welcome sight.

In this week’s Sentiment Report we take a closer look at how we need bulls to have a bull market and where to look for early signs that optimism could be getting excessive.

Re: Goldman Sags

Is this Euphoria? Doubt it.

[PLUS] Weekly Sentiment Report: Seeing Is Believing

From the desk of Willie Delwiche.

Bulls on the Investors Intelligence survey continued to climb while bears fell for the fifth week in a row. The bull-bear spread has now decisively cleared its August high as investors move to embrace the stock market rally.

Why It Matters: One of the missing ingredients for sustained stock market strength last year was the embrace of investors. To be fair, investors did not abandon equities from a positioning perspective and, in fact, during the record stretch of more bears than bulls on the AAII survey, equity ETFs have still seen nearly a quarter-trillion dollars of inflows. Nonetheless, rally attempts last year brought neither broad market strength (in the form of new highs > new lows) nor a meaningful expansion in optimism. In 2023, investors are seeing strength and believing that it can persist. That can become a self-fulfilling prophecy (at least for a while). Almost all of the net gains in the S&P 500 since 2015 have come with the bull-bear spread above 18.

In this week’s Sentiment Report we take a closer look at how investors are updating their views in light of the strength that has been seen in the early going of 2023.

- « Previous Page

- 1

- …

- 4

- 5

- 6

- 7

- 8

- …

- 24

- Next Page »