These are the registration details for our Weekly Town Hall. [Read more…]

[PLUS] Weekly Sentiment Report

From the desk of Willie Delwiche.

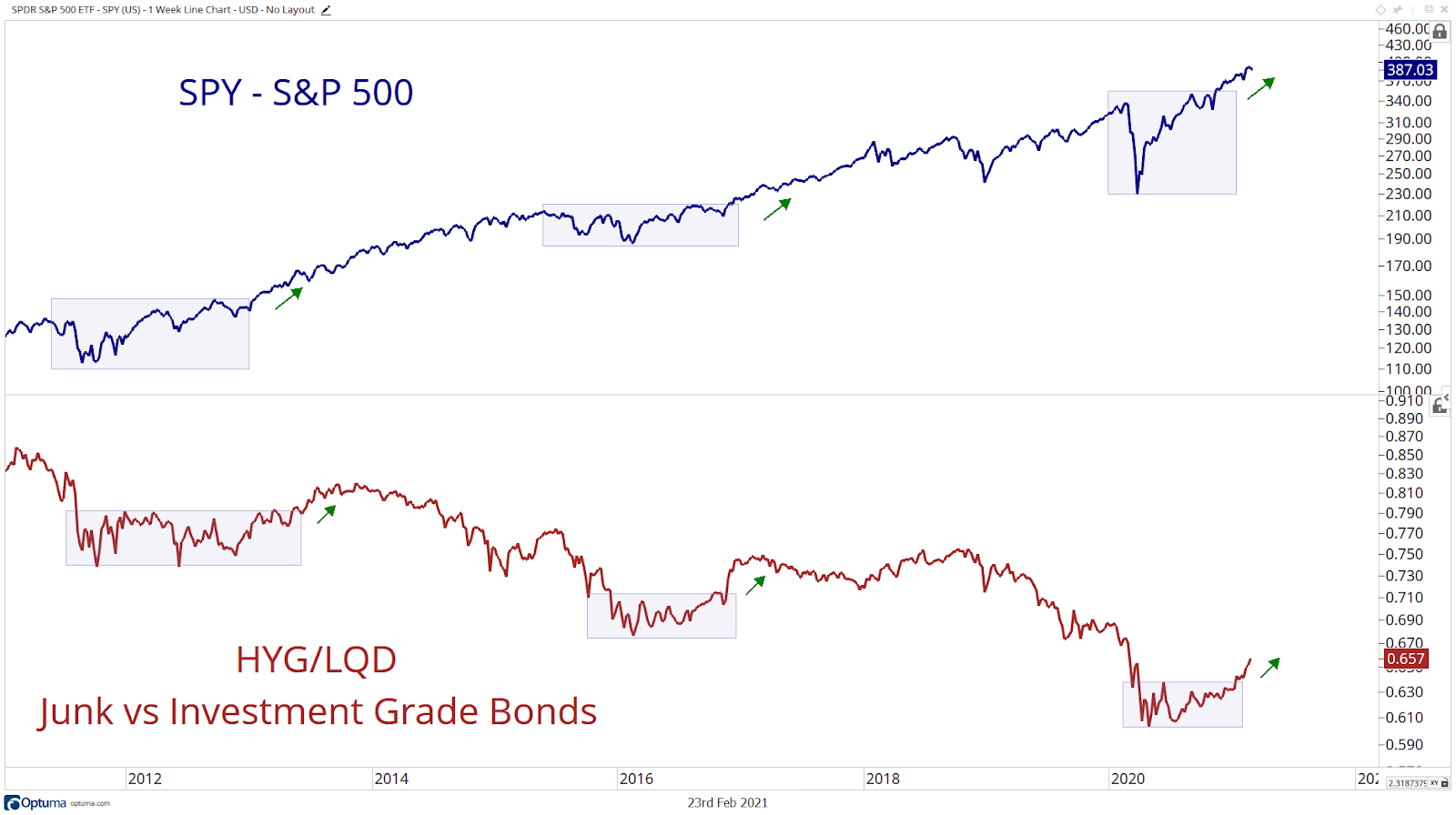

Key takeaway: Optimism remains elevated when looking at investor positioning (equity ETFs have seen a quarter trillion dollars of inflows since the end of Q3) and demand for call options (up 60%+ over the past year). But sentiment concerns become more acute (and stocks more vulnerable) when optimism shows evidence of meaningfully unwinding. This week’s featured sentiment chart (ratio between HYG and LQD) suggests that rather than pushing back from the buffet and beginning to tighten their belts, investors continue to have a robust risk appetite. That doesn’t preclude an uptick in market volatility, but it reduces the risk of sustained weakness at this point.

Sentiment Chart of the Week: HYG/LQD Ratio and S&P 500

Stretched optimism becomes more problematic once risk appetites reverse & the HYG/LQD ratio suggests this is not yet the case. In fact, this ratio is more consistent with the healthy commencement of a new uptrend.

[PLUS] Weekly Market Notes & Breadth Trends

From the desk of Willie Delwiche.

Key Takeaway: After record strength, breadth is taking a well-deserved breather.

This has the hallmarks of digestion more than divergence, especially after recording yet another breadth thrust. Re-opening optimism is running high and bond yields around the world are climbing.

With earnings and economic expectations still being revised higher, the path of least resistance for stocks remains higher even if we are starting to see a few more tripping hazards.

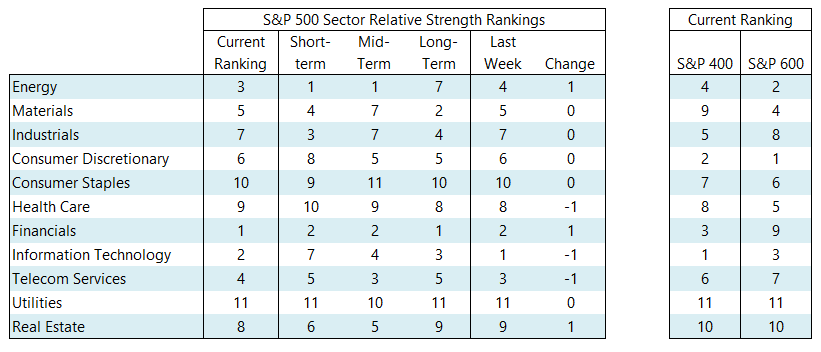

The Financials sector took over the top spot in our large-cap relative strength rankings even though leadership has not been as evident at the mid-cap and small-cap level. Our industry group heat map shows that while banks are improving at all cap-levels, no Financials-related industry groups are near the top of the rankings. Energy climbed into the third spot in our rankings, strength that is supported at the mid-cap & small-cap level. Technology remains in the leadership group, but there is some deterioration being seen at the large-cap and mid-cap level. Small-cap Technology-related industry groups remain quite strong.

[PLUS] Weekly Momentum Report

From the desk of Steve Strazza

Don’t miss this weeks Momentum Report; our weekly summation of all the major indexes at a Macro, International, Sector and Industry Group level. As a reminder, we analyze this shorter-term data within the context of the structural trends at play.

[PLUS] Weekly Observations & One Chart for the Weekend

From the desk of Willie Delwiche.

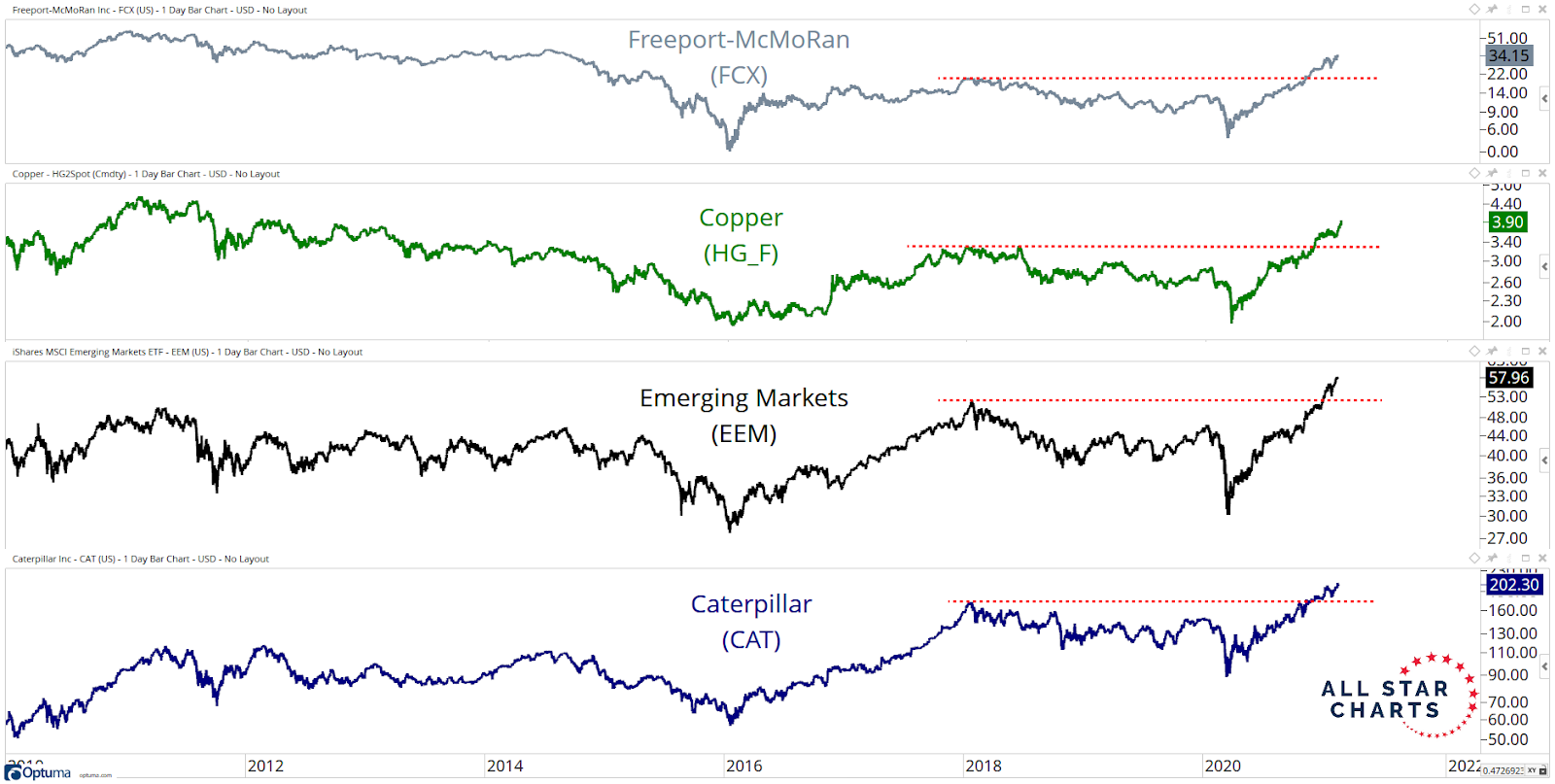

Constructing a narrative can be risky behavior if you end up trusting the story more than the incoming evidence. When you can remain objective, however, it allows you to position for an expected outcome and then test whether that outcome is being realized. Form a hypothesis and test it. Know your parameters beforehand, don’t seek to justify the action after the fact. If the facts change, change your mind. We’ve been discussing the prospects of a global coordinated rebound in growth. The evidence at hand suggests we are indeed seeing that. I see the chart below as the who, what, where, and how of this story. FCX is mining for Copper in EEM using CAT. If any of these start to falter, it will suggest the story is changing. Currently, that is not the case.

[Plus] Weekly Town Hall Meeting w/ Willie Delwiche & JC Parets

This is the video recording of the February 18th Town Hall Meeting w/ Willie Delwiche & JC Parets.

02/18/21 2PM ET [Read more…]

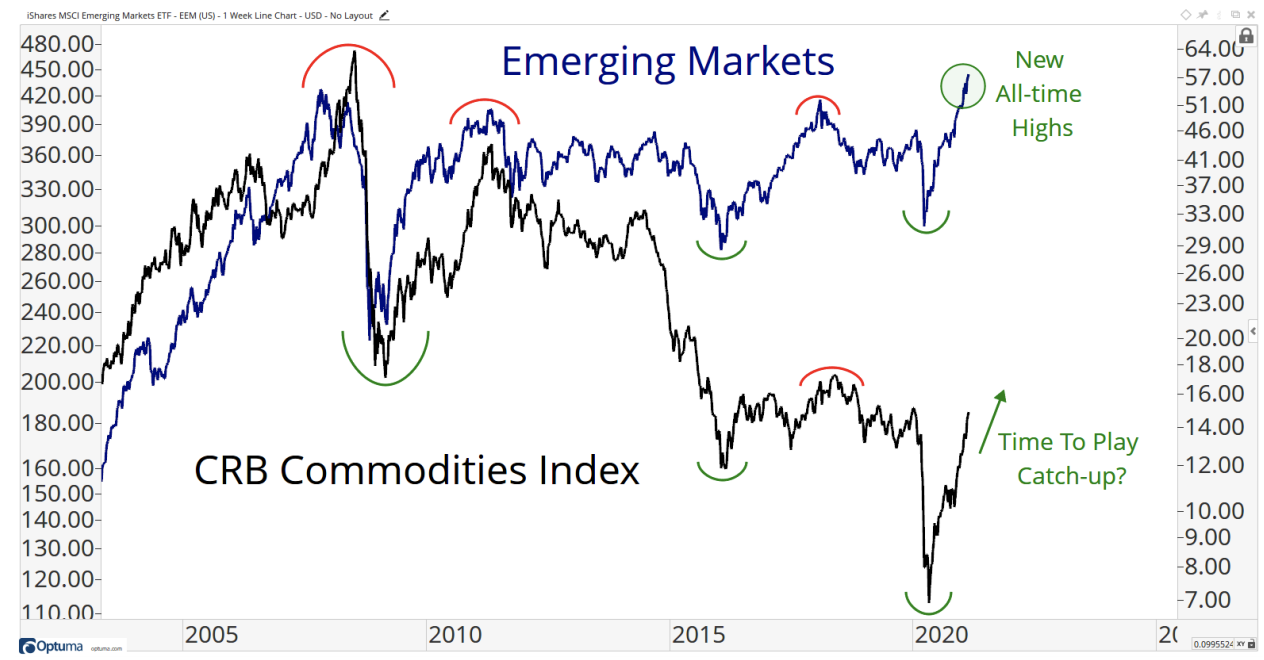

[PLUS] Weekly Top 10 Report

From the desk of Steve Strazza

Emerging Markets hit new all-time highs last week. This is supportive of the bullish action we’re seeing from stocks in other regions of the globe as well as economically-sensitive commodities. It is no coincidence that the Emerging Markets ETF $EEM and the CRB index tend to peak and trough in unison throughout history. They relay a similar message of “risk-on.” The big question now is whether it’s time for Commodities to play catch-up with Emerging Markets.