This is the video recording of the March 25th Town Hall Meeting w/ Willie Delwiche & JC Parets

03/25/21 2PM ET [Read more…]

Expert technical analysis of financial markets by JC Parets

This is the video recording of the March 25th Town Hall Meeting w/ Willie Delwiche & JC Parets

03/25/21 2PM ET [Read more…]

From the desk of Willie Delwiche.

From the desk of Willie Delwiche.

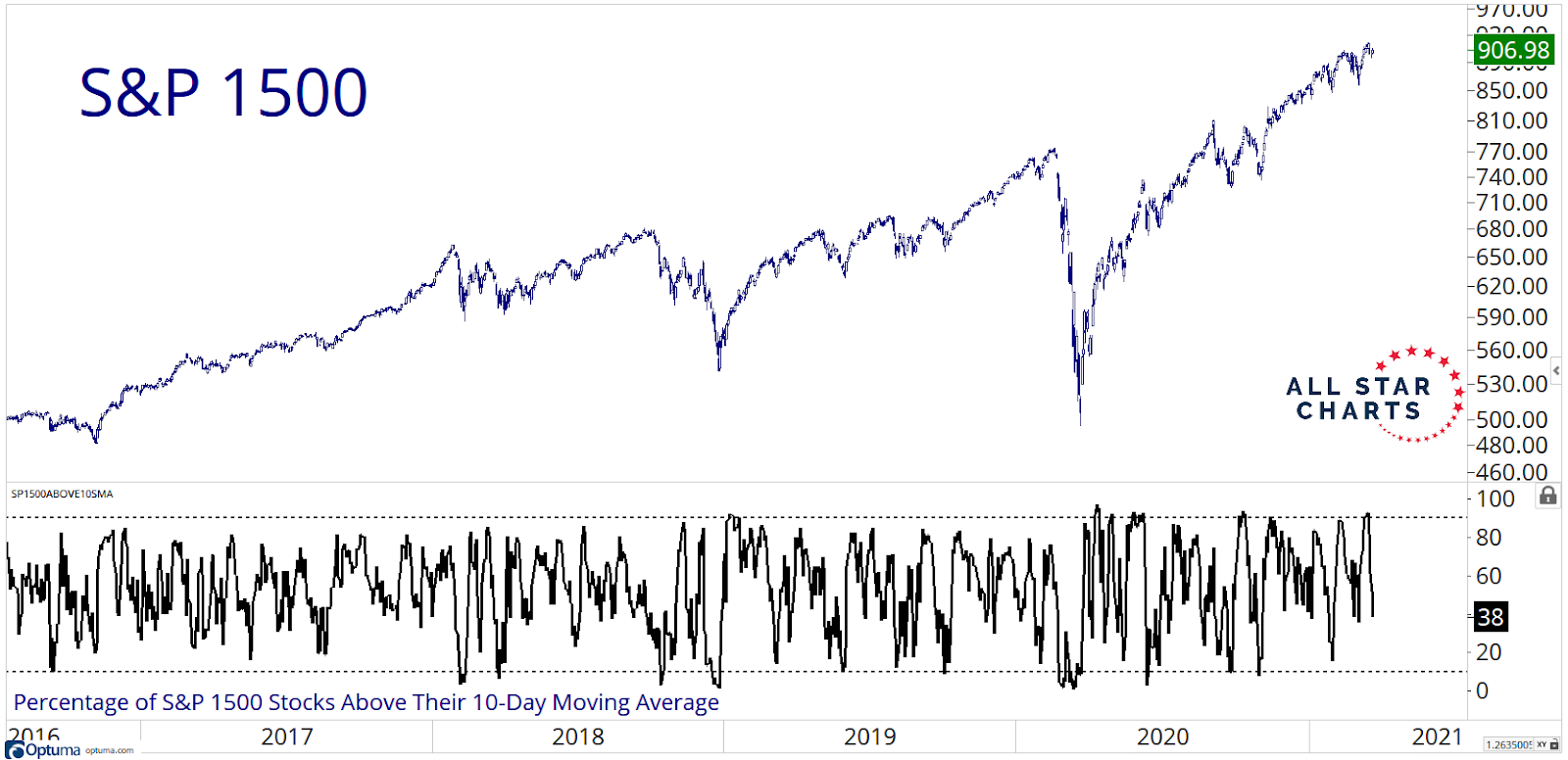

Key takeaway: After a healthy unwind over the past few weeks that allowed sentiment to reset to neutral, we are seeing optimism rebuild. This uptick in optimism has been accompanied by (as we show in our chart of the week) another breadth thrust. There is room for a further expansion in optimism before it becomes an excessive headwind – and continued broad market strength diminishes such a signal in any event. The combination of breadth thrusts and persistently elevated optimism is reminiscent of the late-2016 to early-2018 period. Then, equity ETFs saw 20 consecutive months of in-flows – we are currently in our 10th consecutive month of inflows (although the pace is quickening, with a record $100 billion over the past four weeks). Equities ran into trouble in early 2018 when breadth thrust tailwinds subsided but elevated optimism remained.

Sentiment Chart of the Week: Another Breadth Thrust

The percentage of stocks in the S&P 1500 above their 10-day moving average rose above 90% last week, signaling yet another breadth thrust. This is very constructive for equities as both optimism and breadth expand.

From the desk of Willie Delwiche.

Key Takeaway: Small-caps hit pause but remain market leaders. Another breadth thrust shows rally participation remains robust. Bond yields are digesting recent rise, but the path of least resistance remains higher.

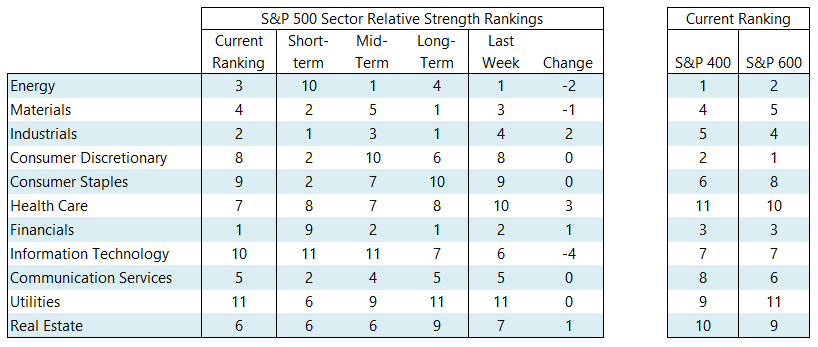

The Technology sector continued its descent toward the bottom of the relative strength rankings. It dropped to its lowest ranking since mid-2016 and fell out of the sector leadership group (which based on a three-week smoothing of the current ranking) for the first time in two years. Technology is joined in the cellar by Utilities, Consumer Staples and Consumer Discretionary. Cyclical value leadership remains intact. Even though small-cap groups led the way lower last week, our industry-group rankings continue to show leadership from small-caps and mid-caps.

From the desk of Steve Strazza

Don’t miss this weeks Momentum Report; our weekly summation of all the major indexes at a Macro, International, Sector and Industry Group level. As a reminder, we analyze this shorter-term data within the context of the structural trends at play.

From the desk of Willie Delwiche.

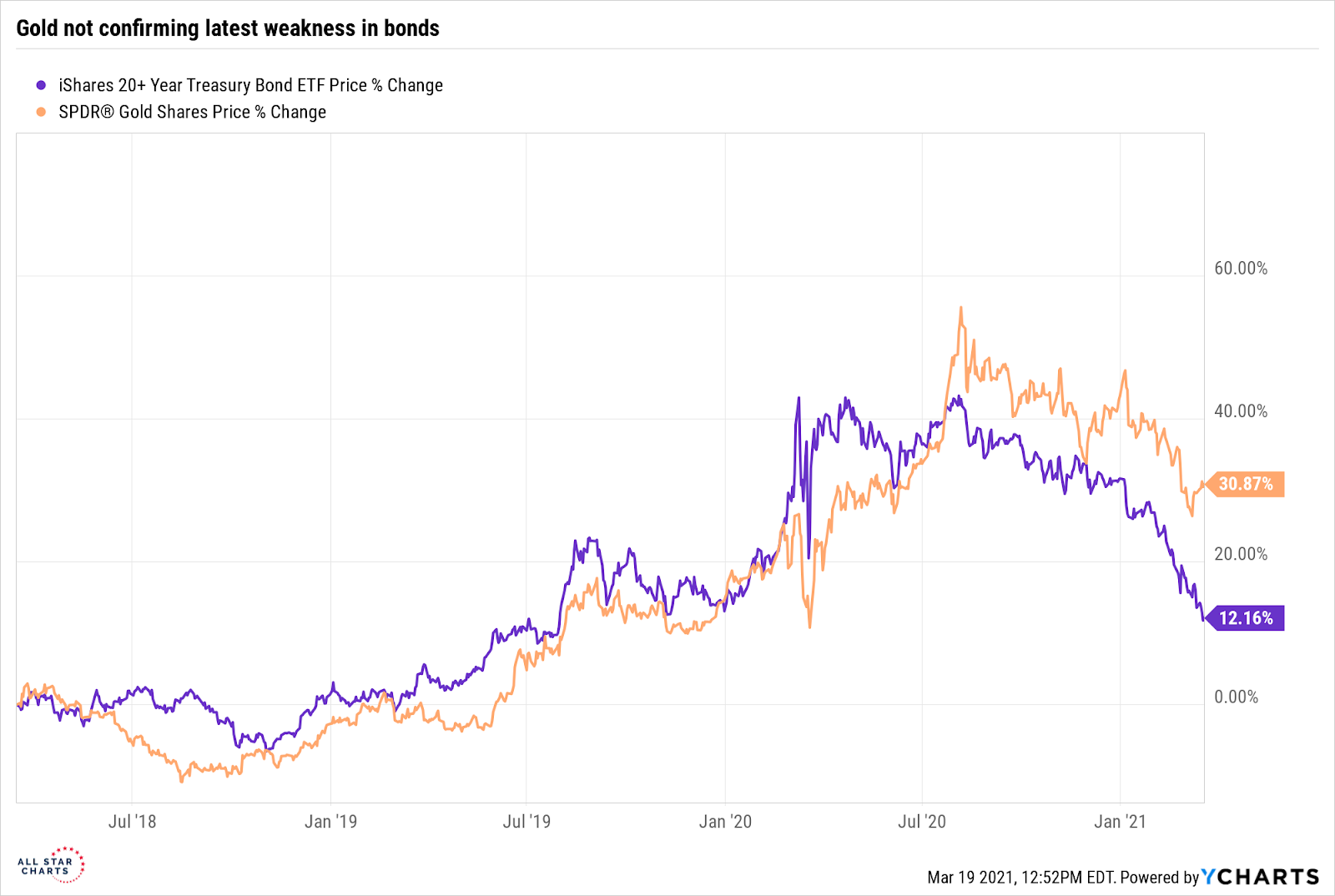

The recent uptick in US Treasury yields has not been confirmed by other areas of the bond market (specifically Bunds & JGBs). Bonds at this point are extremely oversold and sentiment indicators are pointing to excessive pessimism. The caveat is that bonds are in a bear market and so this sort of behavior should not come as a surprise. Still, there may be some room for yields to consolidate or even pullback from here. If that happens, it could provide a chance for gold to gain some traction. Gold & bonds have moved similarly in recent years, though gold has started to firm up even as bonds sold off this week. What sort of retracement of their recent weakness either bonds or gold can achieve remains to be seen – but an opportunity for that may be emerging.

From the desk of Willie Delwiche.

Earlier this week JC referenced the 1966 Western “The Good, the Bad, and the Ugly”. Labelled a “Spaghetti Western” because it was directed by Italian director Sergio Leone, the movie and the genre overall have become cultural icons. Little did JC know that I had just watched this movie with my son within the past week (much the way that I had watched it with my father when I was growing up). Beyond just seeing the market metaphor in the movie’s title, the reference had the movie’s theme music again ringing in my ears.

It’s been a volatile week from a sector level performance perspective, but this is still how I am looking at the market:

From the desk of Steve Strazza @Sstrazza

Let’s play a little devil’s advocate. Do you know what a common characteristic of market tops is? Failed breakouts. We see them everywhere at significant peaks – just look back to February of last year, there were plenty of textbook examples. The Russell 2000 just printed a failed breakout and confirmed a bearish momentum divergence as price sliced below its February highs. Making matters worse, RSI couldn’t even register an overbought reading with the most recent highs.

So, how serious is this? While anything can happen and this could certainly be the beginning of a significant selloff, that’s not what the broader evidence suggests. This is likely a garden variety correction at worst. And after the recent performance, that would be completely normal. We continue to keep our eye on 216 as our tactical level. As long as we’re above it, there’s little cause for concern. On the other hand, if price violates that level things could get dicey and would likely warrant a more neutral outlook in the intermediate-term.