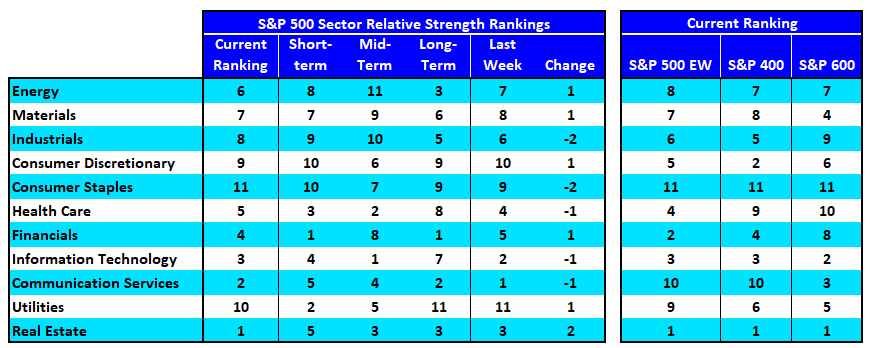

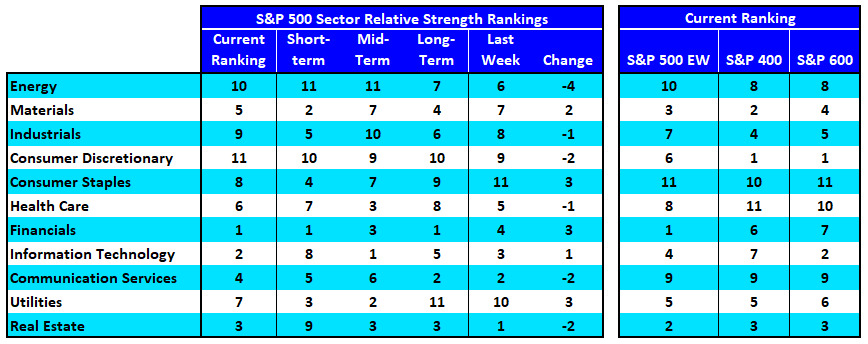

- With a handful of mega-caps driving index-level returns, we want to see sector-level leadership confirmed by similar sector strength on an equal-weight basis, as well as further down the capitalization scale.

- Financials are the top-ranked sector in our rankings on both a cap-weight and equal-weight basis. Strength fades among mid-cap and small-cap Financials. Real Estate remains a leader across the board from a weighting and size perspective, though it has slipped on a short-term basis.