From the desk of Willie Delwiche.

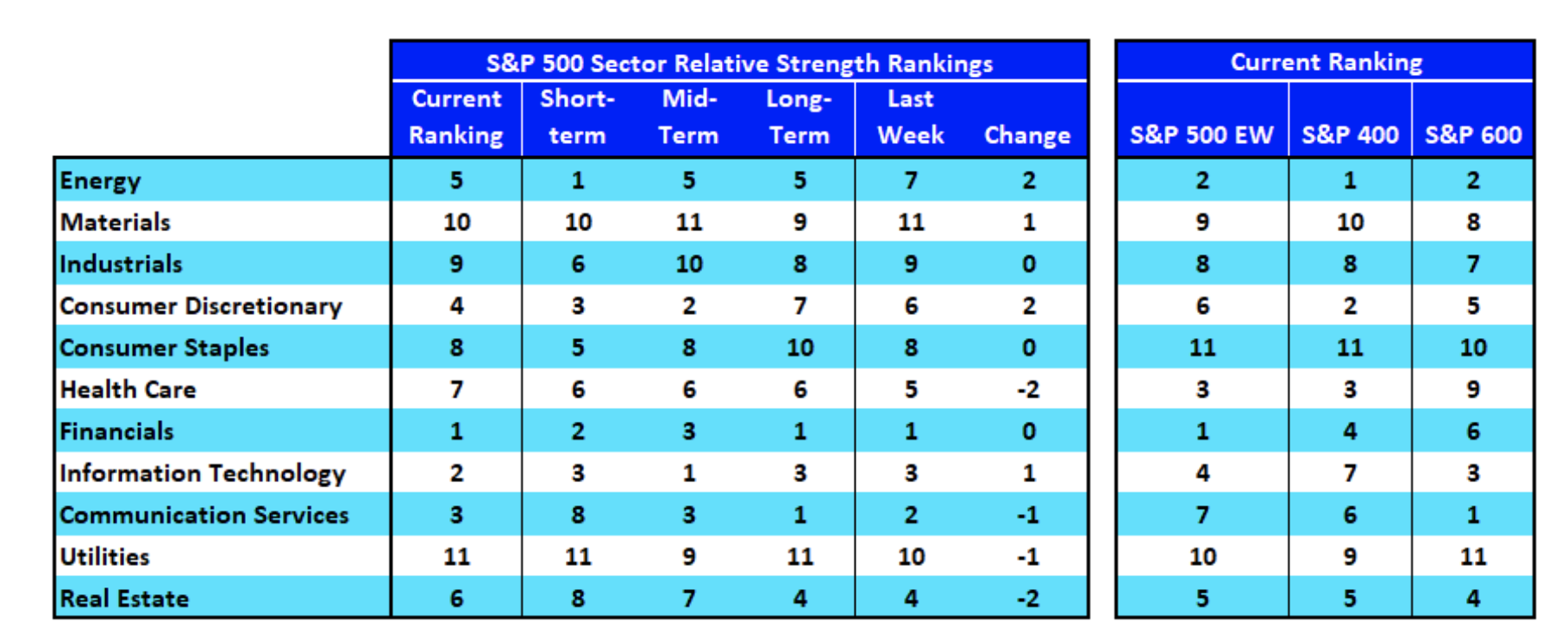

- Energy, which was near the bottom of the rankings from both a cap-weight and equal-weight basis as September began, has continued to gain strength. It has been the top performing sector on a short-term basis (as well as on a YTD basis) and has climbed into the middle of the overall rankings and is at number 2 on an equal-weight basis.

- Health Care and Real Estate have dropped in the rankings, though the industry group heat map shows there remain pockets of strength at the industry group level within the Health Care sector.