{kind=link}

With equity market trends in the US deteriorating, we have reduced domestic equity exposure in our Cyclical and Tactical Portfolios. We are adding equity exposure where we are seeing strength overseas and remembering that asset allocation decisions don’t just come down to stocks vs bonds, but include commodities and cash as well.

[PLUS] Weekly Town Hall w/ Willie Delwiche

This is the video recording of the February 24th Weekly Town Hall w/ Willie Delwiche

02/24/22 2:00 PM ET [Read more…]

[PLUS] Weekly Sentiment Report

From the desk of Willie Delwiche.

Key Takeaway: Optimism wanes, and pessimism builds as the II bull-bear spread narrowed last week to just 1.2%, down more than 4% from the previous week. That brings the spread to its smallest difference since early April 2020. But it’s not until bears outnumber the bulls that we reach levels associated with significant market bottoms. Nevertheless, a surge in pessimism could become reality with active equity managers continuing to reduce exposure, consensus bulls dropping, and major equity indexes testing their respective January lows. Whether sentiment has completely unwound or is still in the process of unwinding is yet to be determined.

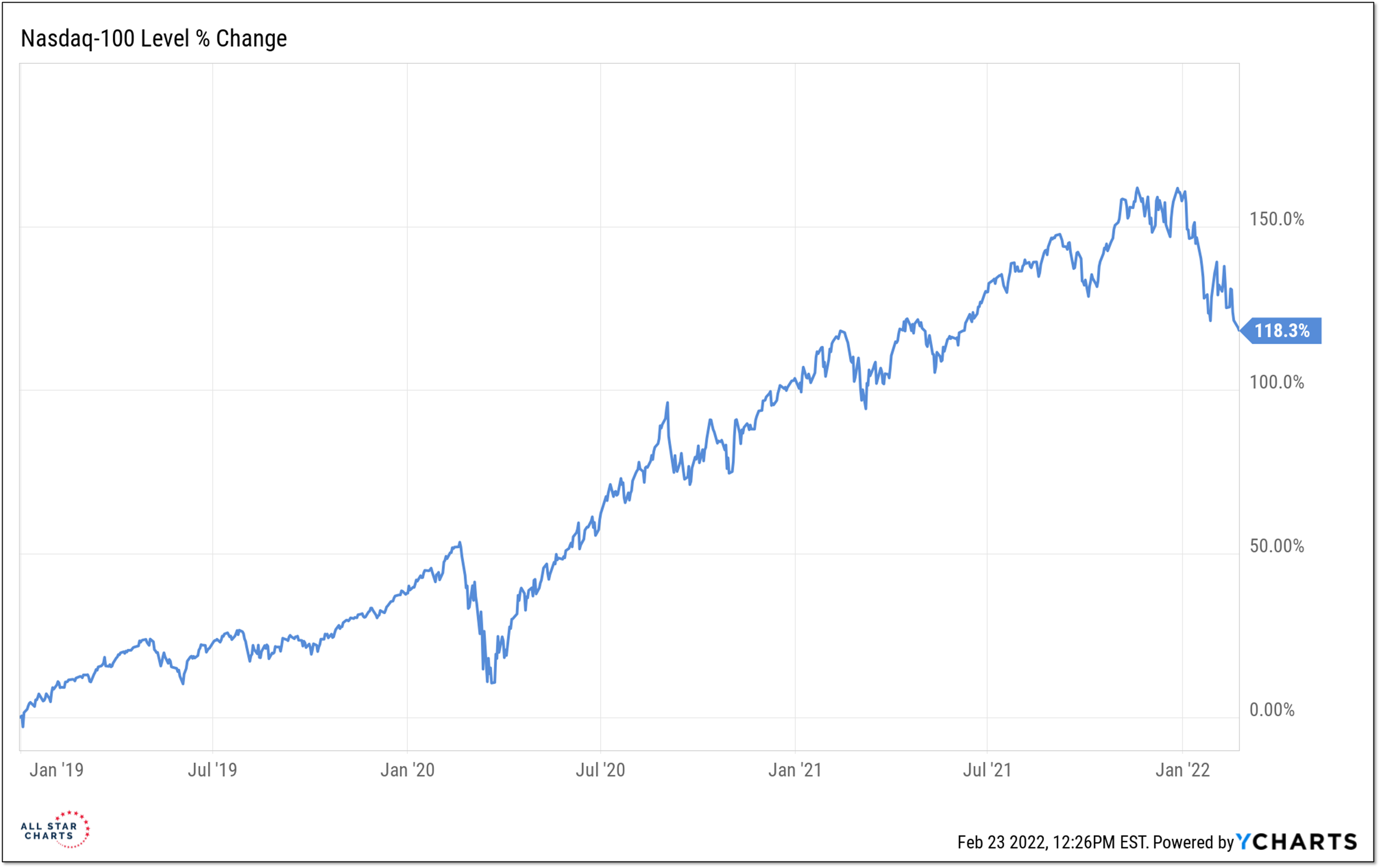

Sentiment Report Chart of the Week: Unwound or Unwinding

The NASDAQ is getting plenty of attention for the carnage that is occurring beneath the surface. The stat that really sticks out for me is that 95% of the trading days over the past three months have seen more new lows than new highs. That weakness is now hitting the index and while the NASDAQ 100 is making new YTD lows it’s still more than twice as high as it was at the start of 2019. So while we are seeing evidence of fear and pessimism in the sentiment data, the question I wrestle with from a price perspective is whether we have unwound or are still unwinding. If it’s the former, we should soon find support and start seeing more new highs than new lows. If it’s the latter (which is the direction I am leaning), then there is room for pessimism to continue to rise and the NASDAQ 100 could soon be in the red on a year-over-year basis.

[PLUS] Weekly Market Notes & Breadth Trends

From the desk of Willie Delwiche.

- News headlines exacerbating underlying trends.

- Leadership rotation has accelerated in 2022.

- Time in the market is a waste of time if you are in the wrong market.

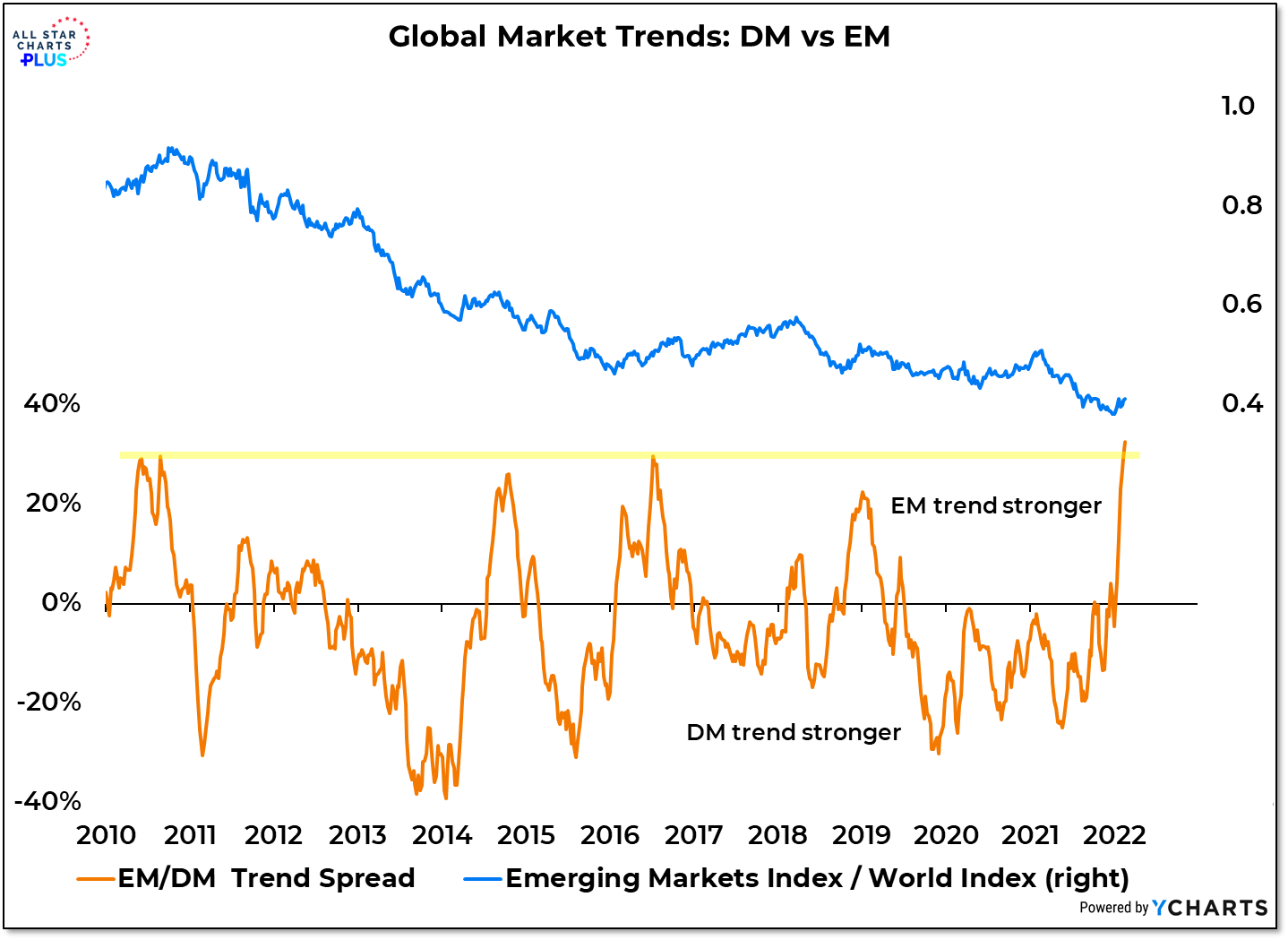

While the leaders of the last decade are weakening, the laggards of the last decade are gaining strength. Commodities are making new highs and Energy, which is the worst performing sector over the past 10 years, is the only sector in the S&P 500 in positive territory on a YTD basis. Globally, we are seeing strength and leadership from the rest of the world versus the US. Trends in Emerging Markets versus Developed Markets are as strong as they have been in over a decade. As we see these shifts, staying in harmony with the trend is critical. “Time in the market” can be a waste of time if you are in the wrong market.

[PLUS] Weekly Observations & One Chart for the Weekend

From the desk of Willie Delwiche.

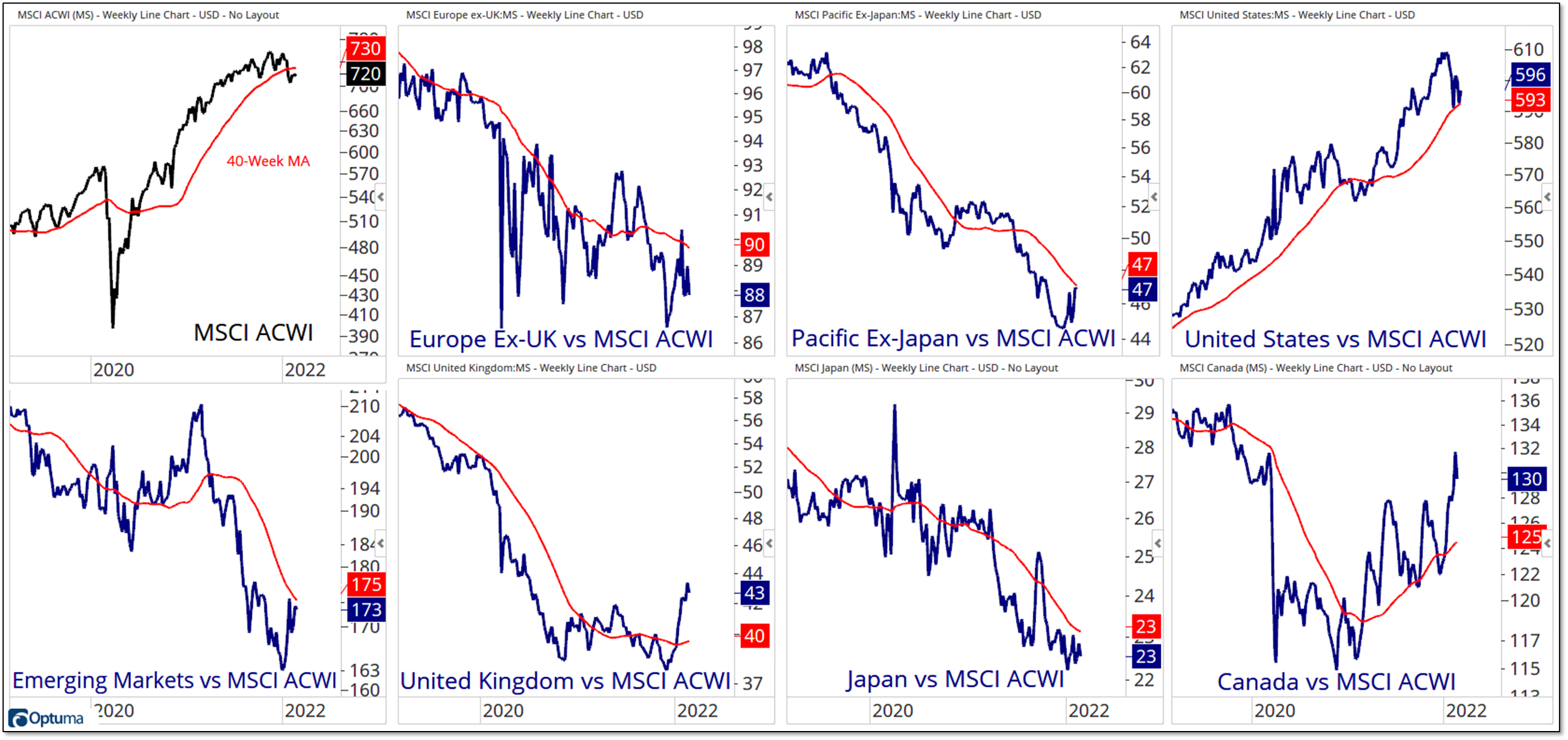

There are plenty of ways in which we make our lives more complicated. There’s an endless list of things we could look at that would obscure our perspective. If I’ve learned anything in nearly a quarter century in this business, it’s that simple trumps complicated and clarity beats obscurity. That’s what makes this week’s one for the weekend so lovely. The 48 markets that make up the ACWI can be summed up in seven charts: 3 regional composites and 4 individual countries. A single slide provides a great starting point for identifying new opportunities and increasing risks on a global scale. The message now is straightforward. The UK and Canada have broken out on a relative basis and EM looks like it wants to. The US has pulled back to an important juncture and the rest of the world remains messy. (Shout out to Grant for putting this global dashboard together.)

[PLUS] Weekly Town Hall w/ Willie Delwiche

This is the video recording of the February 17th Weekly Town Hall w/ Willie Delwiche

02/17/22 2:00 PM ET [Read more…]

Breadth Thrusts & Bread Crusts: A Big Test For Passive Investors

From the desk of Willie Delwiche.

I’m reading the book “Trillions” by Robin Wigglesworth right now. It’s about the rise of passive index investing – or, according to its sub-title, “How a band of Wall Street renegades invented the index fund and changed finance forever.”

It’s been an enjoyable read so far. I’m about halfway through the book and am excited to see how it finishes.

While Wigglesworth’s book has been written and published, the story of passive investing overall remains unfinished. If it is like other investing fads that have come and gone, some of the most exciting times (for better or worse) may lie ahead. History is littered with investment approaches that move from novelty to seemingly foolproof only to end in heartbreak and tears for those left holding the bag.

[PLUS] Weekly Sentiment Report

From the desk of Willie Delwiche.

Key Takeaway: Speculative excesses have been unwinding for a year and that has taken its toll on investor sentiment. The overall mood is characterized by a lack of optimism rather than rampant pessimism. This is consistent with the grind lower in many areas of the market since new highs peaked in February 2021. The damage done beneath the surface has only in recent months impacted the indexes, but if that impact intensifies a further expansion in pessimism would not be surprising. Benchmark 60/40 portfolios have gotten off to their worst start in a quarter century and our strategic positioning indicators continue to point to a high risk backdrop. If there isn’t much of a reward at the end of the volatility rollercoaster, passive participants may start to actively question whether the ride was worth it.

Sentiment Report Chart of the Week: Unwind Continues

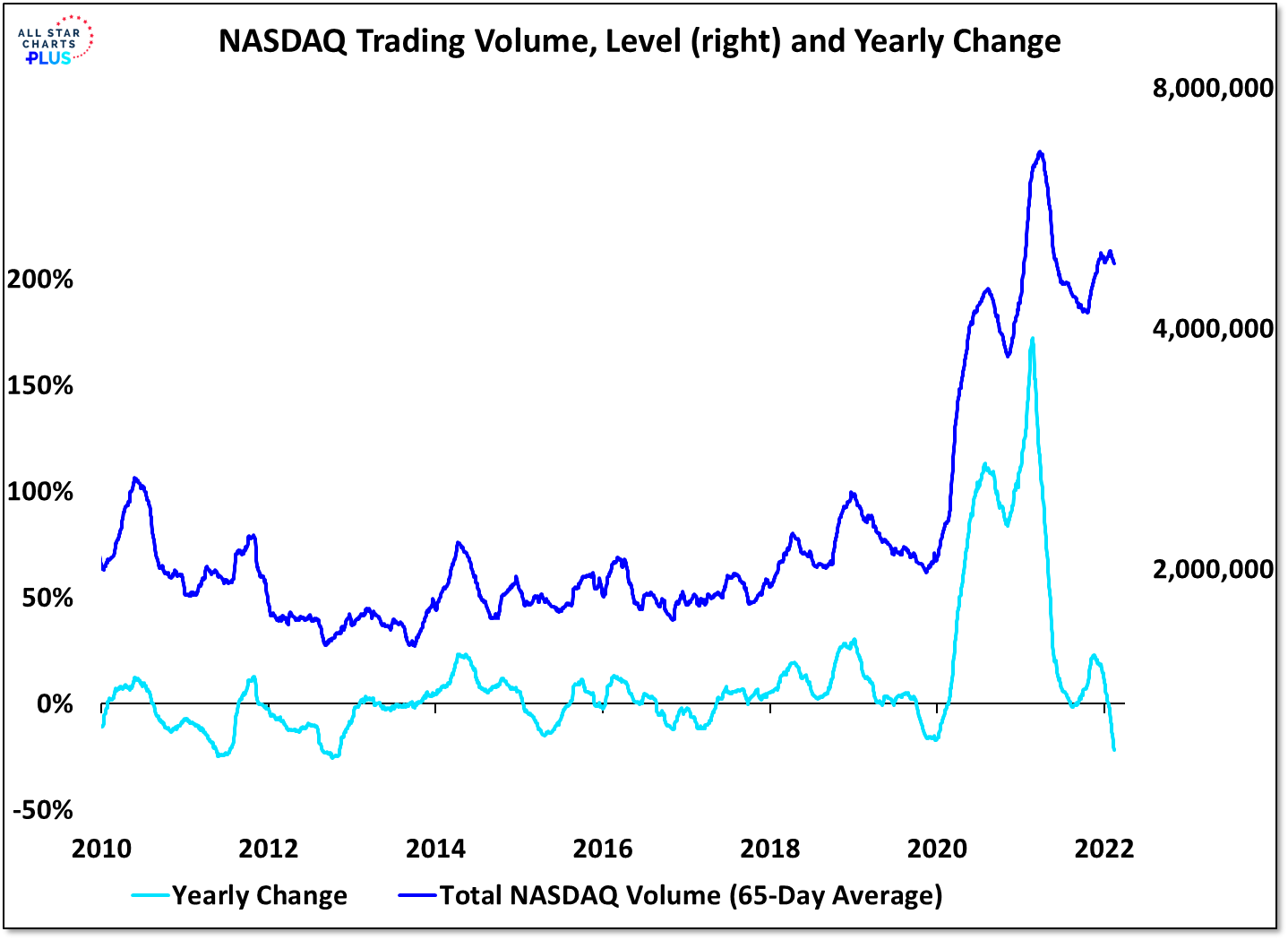

While the popular averages peaked more recently, there is plenty of evidence to suggest we are now a year into an unwind in speculative activity. This time last year, more than a quarter of the issues on the NYSE+NASDAQ were hitting new highs (the peak for the cycle) and NASDAQ trading volume was 150% higher than it had been the year prior. Fast forward to this year and we see half of the stocks on the NYSE and three-quarters of the stocks on the NASDAQ are down 20% or more from their highs (nearly half of the stocks on the NASDAQ have been cut in half). NASDAQ trading volume is 20% (and falling) lower than it was a year ago. Sentiment is sour and the risk appetite unwind continues. The question isn’t whether US stocks are going to enter a new bear market, but when they will emerge from the one that many find themselves in already.

- « Previous Page

- 1

- …

- 35

- 36

- 37

- 38

- 39

- …

- 79

- Next Page »