This is the video recording of the April 1st Town Hall Meeting w/ Willie Delwiche & JC Parets

04/1/21 2PM ET [Read more…]

Expert technical analysis of financial markets by JC Parets

This is the video recording of the April 1st Town Hall Meeting w/ Willie Delwiche & JC Parets

04/1/21 2PM ET [Read more…]

From the desk of Willie Delwiche.

I’m now into my second year of working from home.

Moving to my home office began as a temporary situation during the height of COVID uncertainty. But a day at home turned into a week, which turned into a month. You know the rest.

I was fortunate that I had an office of sorts set up in my basement prior to the pandemic. If ever a basement room could be cozy, this might be the one — wood plank floor, brick walls, south and east-facing windows that provide some natural light and the opportunity for the dogs to look in on me while they play in the backyard.

Of course, I had to make some changes to my permanent basement headquarters. I’ve rearranged the room several times to accommodate a growing array of equipment and an always increasing supply of books. I’m on my fifth or sixth iteration of a desk setup as I’ve moved from sitting on a couch hunched over a laptop to standing at a desktop of salvaged planks and looking at a couple of monitors.

I am thankful for what I have at home, but there definitely are a few things I appreciated about working downtown…

From the desk of Willie Delwiche.

From the desk of Willie Delwiche.

Key takeaway: The evidence continues to suggest we have recently undergone a healthy unwind in excessive optimism. Investment manager’s equity exposure has dramatically pulled back from extreme readings but remains above levels that signals a shift toward risk aversion risk that can weigh on price. Combining that with budding optimism among individual investors and a supportive, neutral backdrop in sentiment arises. Though global markets lack strength from a tactical perspective, the message remains digestion over deterioration given recent breadth thrusts and that the majority of international markets are in uptrends. For now, the reset in sentiment provides upside potential for both optimism and price.

Sentiment Chart of the Week: Risk Appetite Remains Healthy

The recent unwind in optimism has been met with sustained risk appetite levels. Both High Yield Bonds and Copper hold above key levels relative to their safer alternatives, suggesting a market environment characterized by digestion, not deterioration.

From the desk of Willie Delwiche.

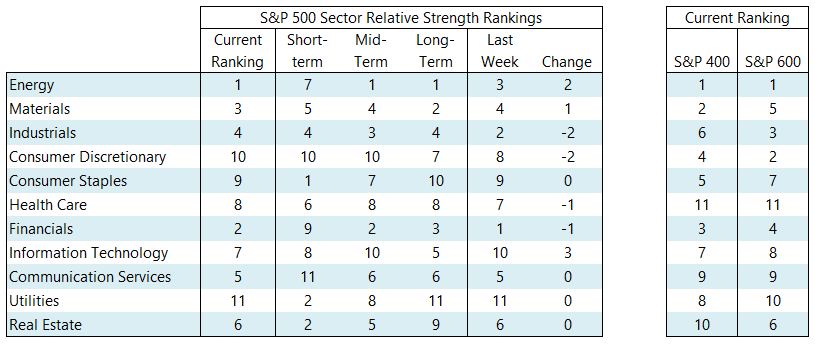

Key Takeaway: Even with bottlenecks & distortions, economic recovery & cyclical rally remain intact. Tactical risks have risen as the market digests gains of last year. Watch bond yields & global participation for evidence that the rally is ready to resume.

Cyclical value sectors remain the leaders in our relative strength rankings and small-cap groups continue to dominate the upper-tier of our industry group rankings. But there is evidence beneath the surface of shifting trends. Rather than seeing a reversion back to growth leadership in our sector rankings, we are seeing defensive areas of the market start to heat up. Consumer Staples, Utilities & Real Estate have the best relative strength on a short-term basis. At the industry group level, small-cap groups are deteriorating while large-cap groups are improving.

From the desk of Steve Strazza & Grant Hawkridge

Don’t miss this weeks Momentum Report; our weekly summation of all the major indexes at a Macro, International, Sector and Industry Group level. As a reminder, we analyze this shorter-term data within the context of the structural trends at play.

From the desk of Willie Delwiche.

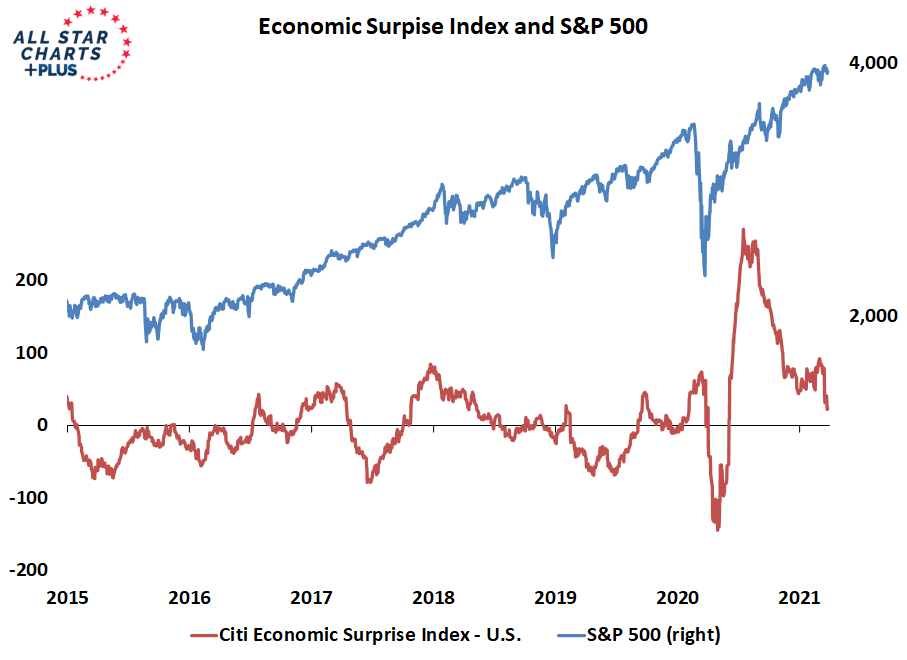

The rally in the stock market over the past year has been buoyed by many things and its shows. The year-over-year change in the S&P 500 reached its highest level ever this week as the index moved past the anniversary of its COVID lows. One of the sources of support in recent months has been economic data that have been consistently better than expected. Stocks have tended to do well when economic data surprises to the upside and they tend to struggle when the surprises have been to the downside. While the Economic Surprise Index is still positive, it has come under pressure in March. First, expectations for the recovery are being revised higher, but more immediately, there were a number of data misses in recent weeks. For example, housing market activity for February was weaker than expected (we touched on this in this week’s Perspectives piece). Economic optimism is generally welcome and tends to be self-fulfilling, but if expectations move too far ahead of reality, stocks can find themselves on a rocky path.

From the desk of Willie Delwiche.

March in Wisconsin (especially here in Milwaukee close to Lake Michigan) is a season of it being already and also not yet Spring. Depending on whether the wind is blowing out of the warm Southwest or coming at us right off of the lake, temperatures can swing dramatically. But the consistent warmth of the Sun heats the Earth and gets the soil ready for planting.

It’s one of the most exciting times of the year for me, full of promise & expectation. I’ve already been at work in the garden (the areas, that is, that are already receiving enough sunlight to soften the dirt). One of several changes in my life over the past year was last Fall’s rebuilding & re-arranging of the raised beds in our backyard. I’m excited by the new layout but it means more work getting them ready for planting. The beds are pretty barren at this point. Rhubarb and horseradish will soon provide some evidence of life, and I tried to work around the asparagus, so hopefully that survived. Garlic, unfortunately, did not get planted.