From the desk of Willie Delwiche.

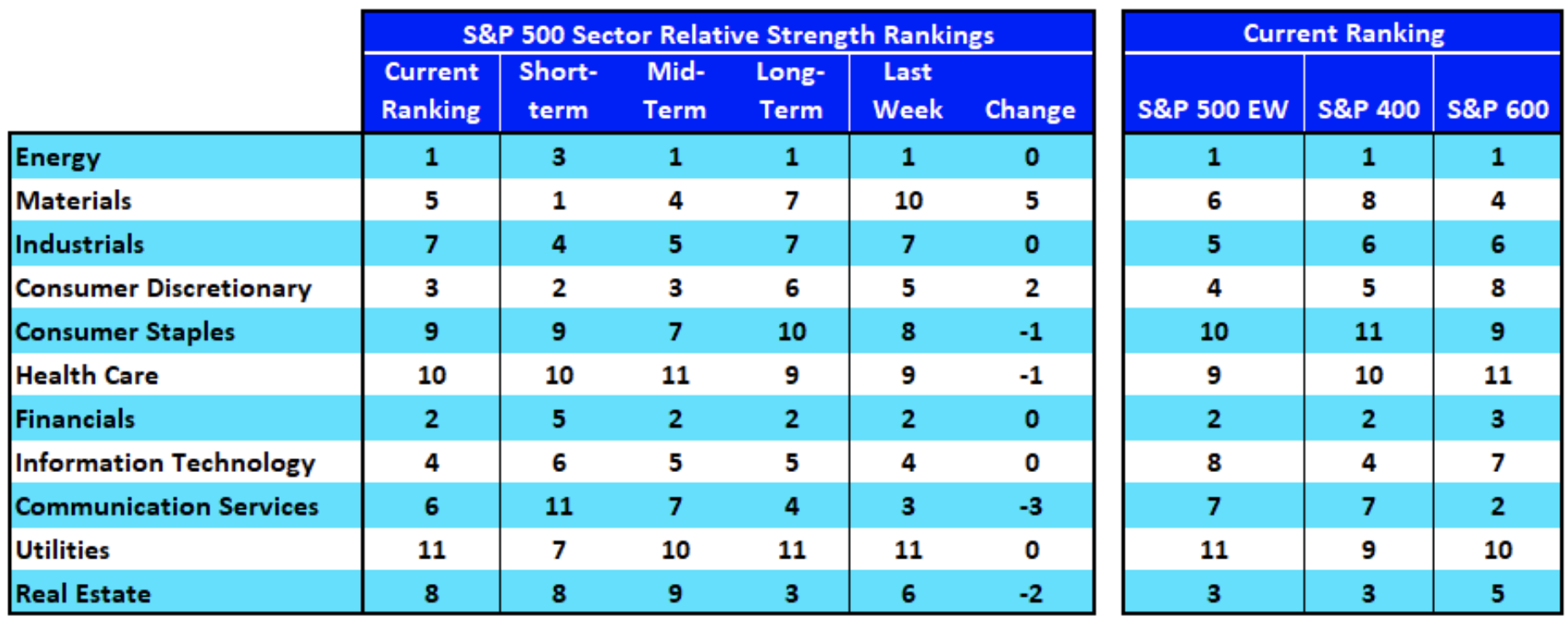

- Paying attention to relative strength can help in two ways. It identifies leaders, to whom active investors can tilt toward, and laggards, from whom those same investors can tilt away. Up and down the size scale, Energy and Financials are leaders, while Utilities, Health Care and Consumer Staples are laggards.

- At the industry group level, mid-cap groups are seeing improving relative strength, while large-cap groups are seeing their relative strength deteriorate.