From the desk of Willie Delwiche.

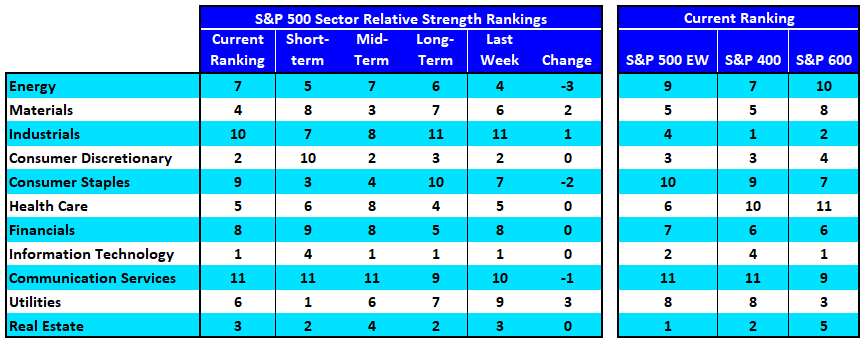

- Energy slipped three spots (from 4th to 7th) in the large-cap rankings last week, and the sector appears even weaker beneath the surface. It’s in the ninth spot on an equal-weight basis, and conditions are deteriorating within the mid-cap and small-cap energy space.

- Technology remains atop the overall rankings, but relative strength on a short-term basis is from coming from Utilities, Real Estate and Consumer Staples.

{kind=link}