From the desk of Willie Delwiche.

Key Takeaway:

- Optimism fades as risk off reigns.

- Inflation hopes spring eternal.

- Beneath the global trends it’s Pax Britannica.

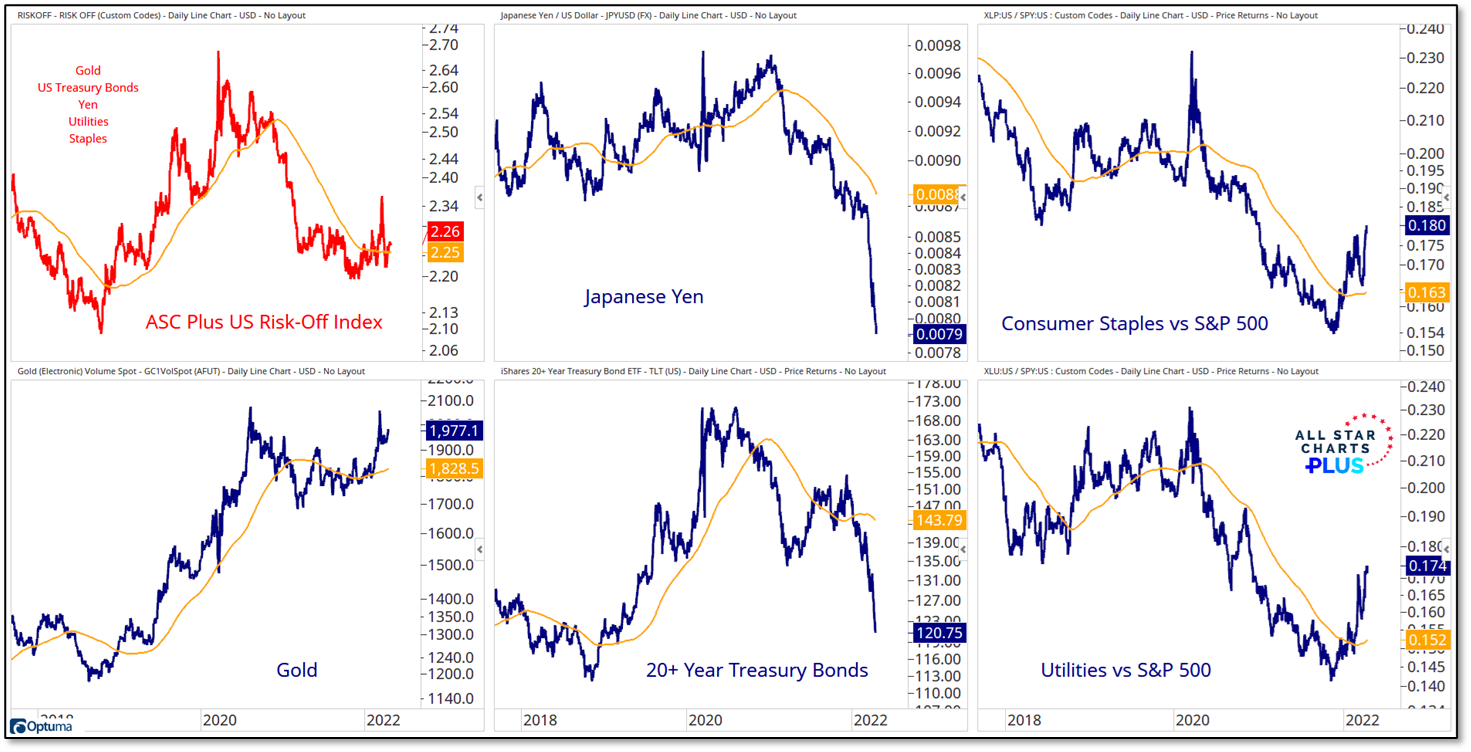

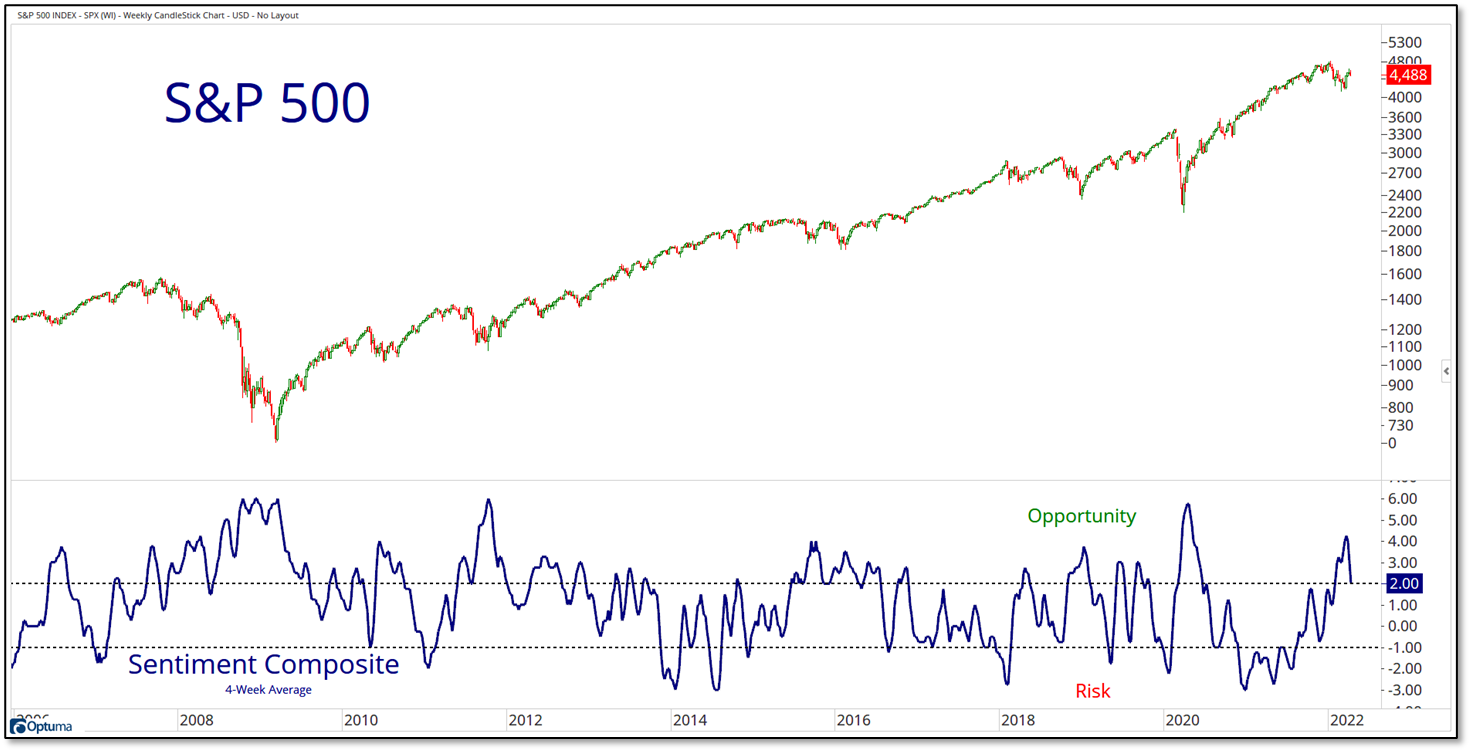

The hope that emerged from the epic March bounce and the promise of seasonal tailwinds has run into the harsh reality that the breadth backdrop remains challenging and the risk environment has not meaningfully improved. Simply put, this was not the April the bulls were looking for. Optimism has been nipped in the bud (AAII bulls dropped to their lowest level since 1992 last week) and our longer-term risk on /risk off indicator has fallen back toward its March lows. But nothing is actually that straight forward. Looking within our US Risk Off Index, we see three of them are at or near new highs, while two are breaking down to new lows. Even within areas that typically move together, we are seeing evidence of bifurcation.