It’s hard to get away from the crowd when you only ask the questions that everyone else is. When we ask better questions, we get more relevant answers. The questions being most asked right now focus on whether we are going into a bear market and whether we are seeing capitulation (“Was that the bottom?”).

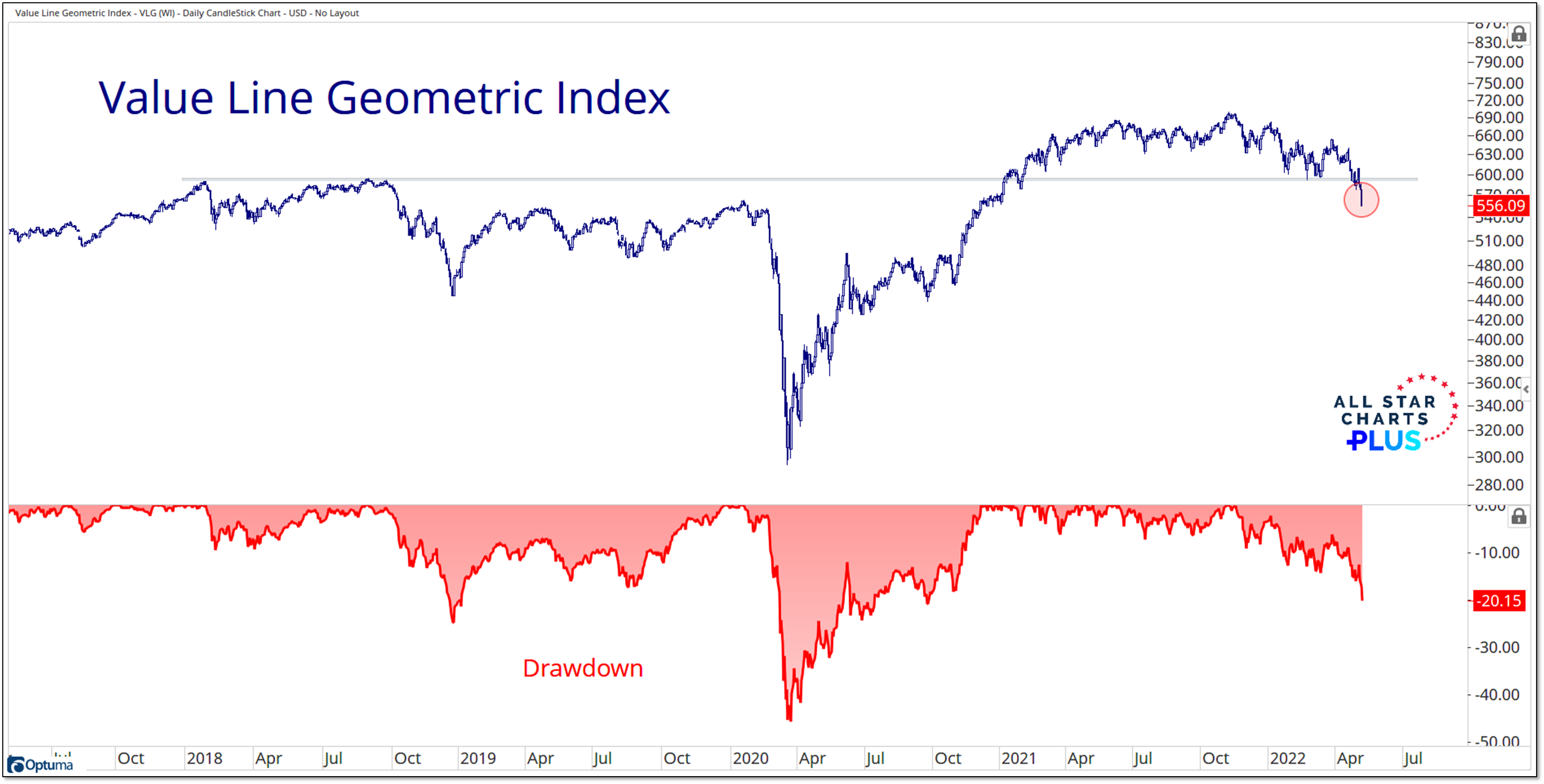

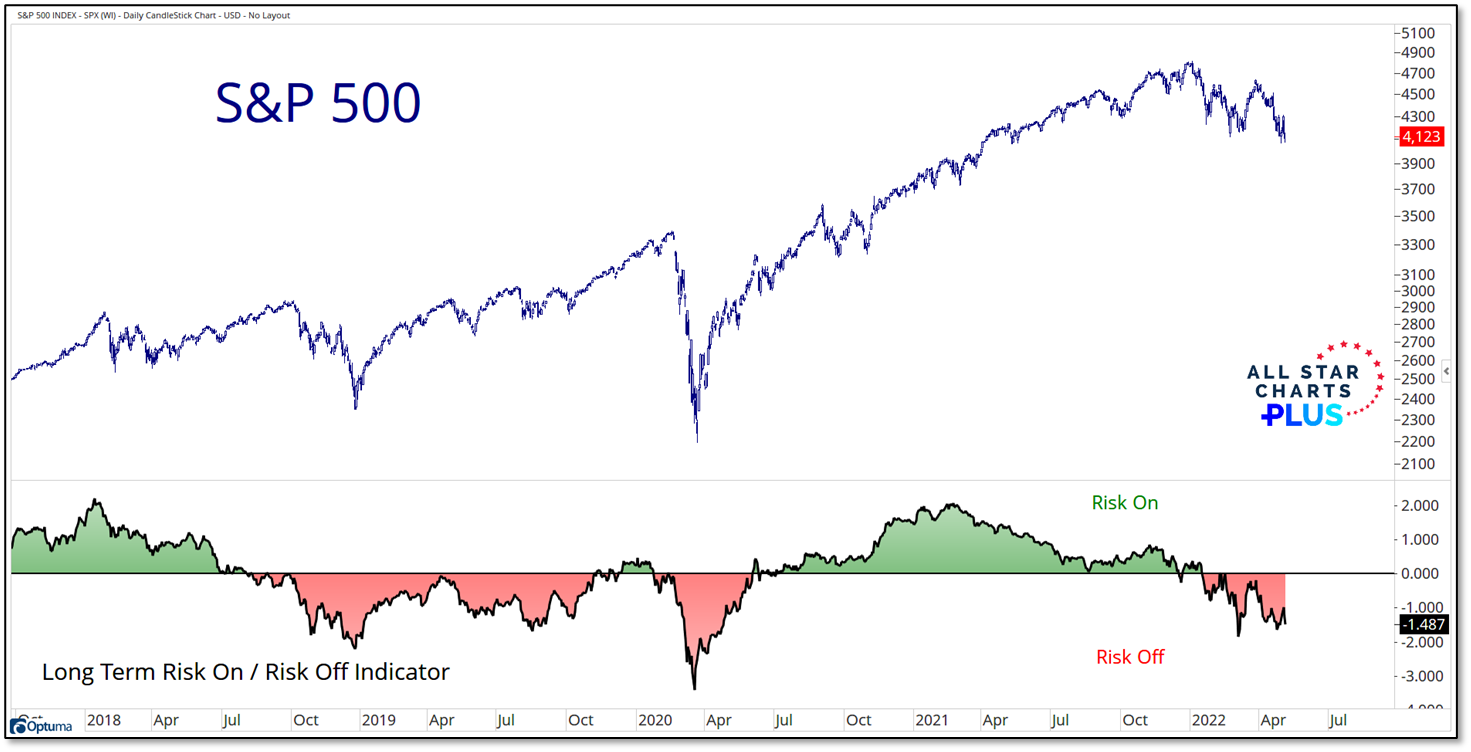

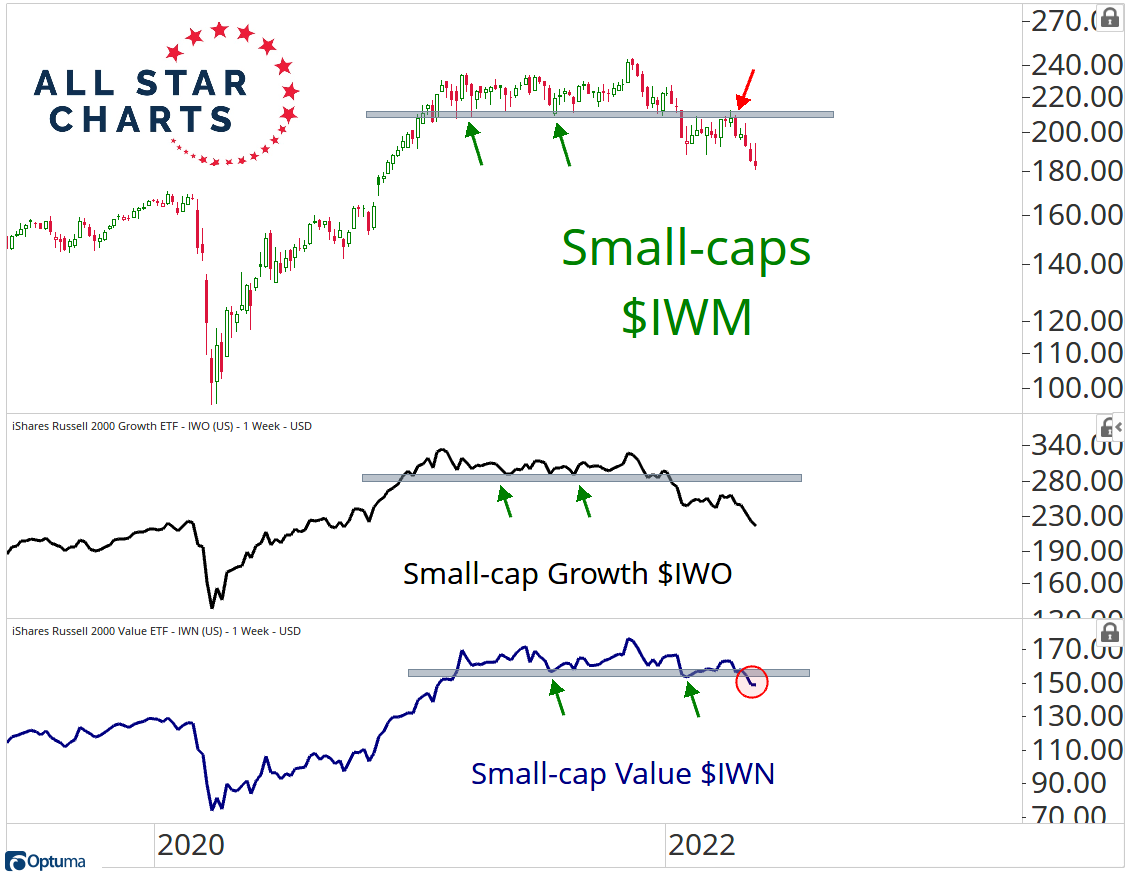

- A bear market has been evident beneath the surface (at least since late 2021, but in some ways for over a year). It’s now showing up in the indexes. The Value Line Geometric Index is below its 2018 highs (as well as its Jan 2020 pre-COVID peak) and is in a 20% drawdown (the line in the sand many use to identify bear markets).

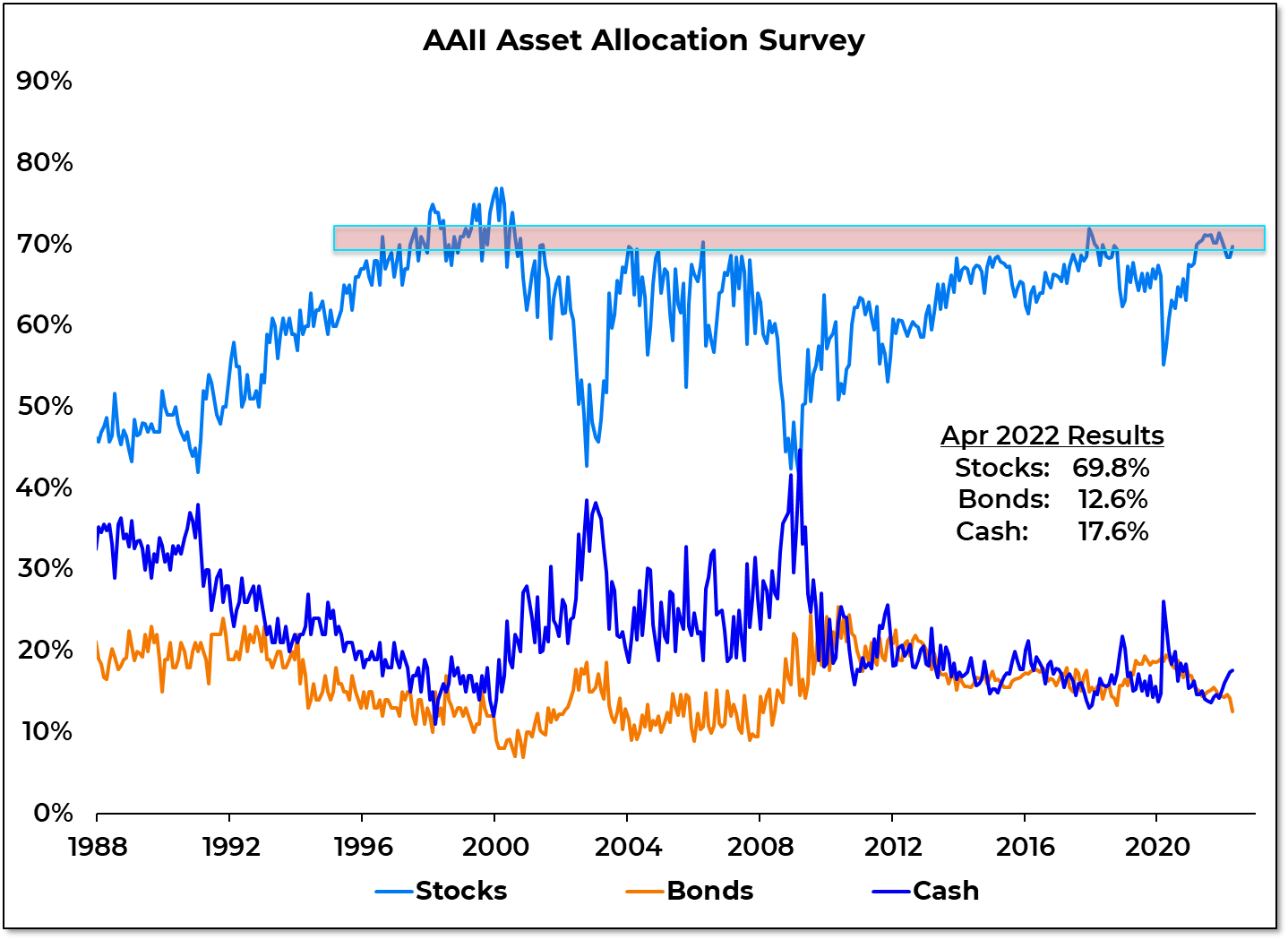

- I understand the allure of trying to call a bottom in real-time (or close to it). But I’ll let the market sort that out. The crowd, focusing almost exclusively on their favorite sentiment data, has been doing that all year and so far at least, they have been wrong.

The questions on my mind are “what do we tend to see when bull markets are re-born and what is the evidence that we are moving from a period of rising volatility to one of sustained strength.