From the desk of Willie Delwiche.

Key Takeaway:

- Patient investors will let the bulls prove their case.

- Economic risks on the rise as data disappoints.

- Central bank action adding pressure to market and economy.

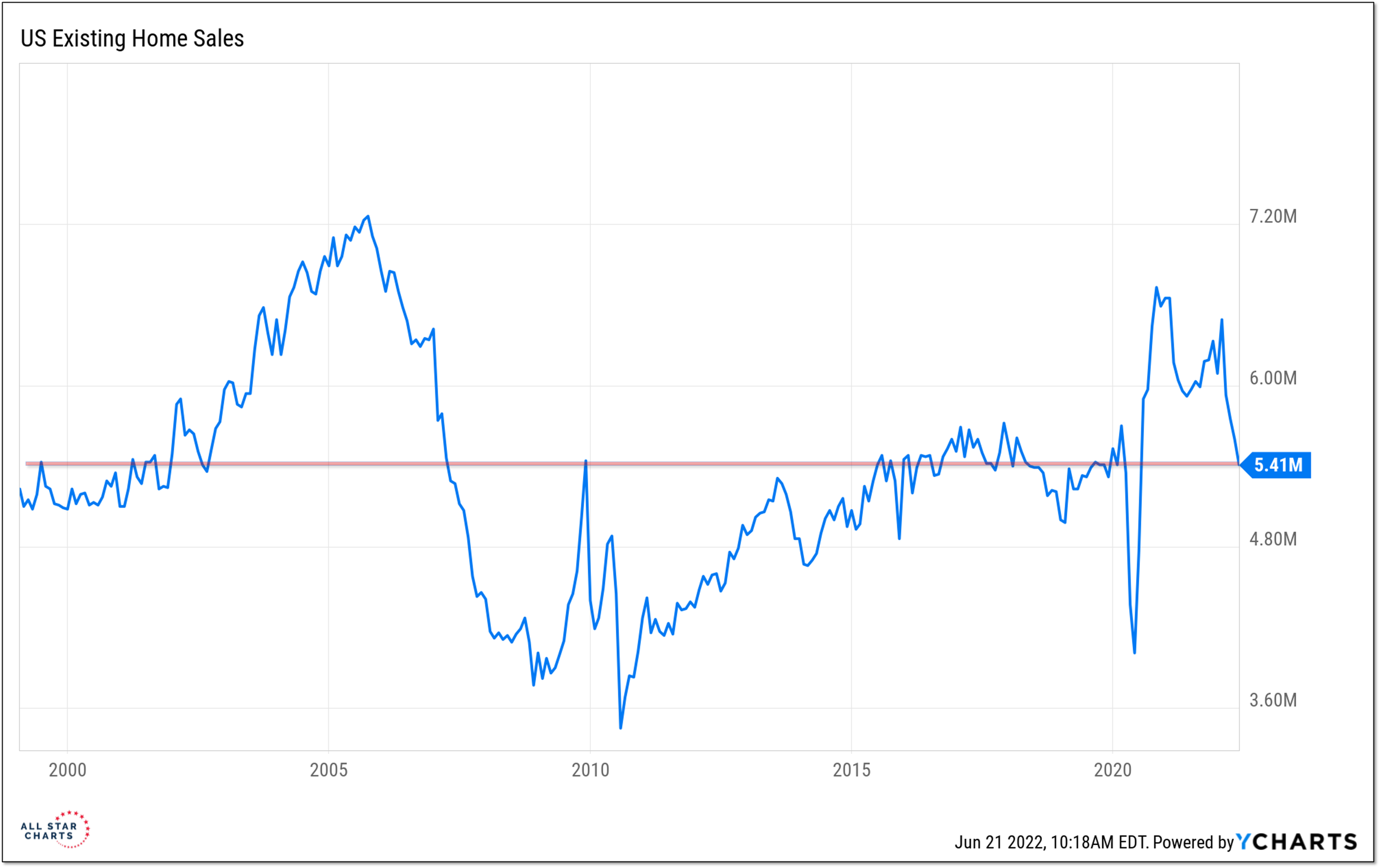

When we look at the data we have in hand, avoiding recession is looking more and more like a dubious proposition. Last week’s retail sales data showed that adjusted for inflation, retail sales in May were below year ago levels. While COVID-related distortions have added to the volatility in sales data, the last three recessions have all been associated with year over year declines in retail sales. XRT (the Retail ETF)is currently more than 40% below its November peak and the two prior times it found itself in a 40% drawdown (2008 and 2020), the economy was already in recession. New orders data from the Philly Fed show an abrupt slowing in business activity. Housing market activity is cooling rapidly. The May existing home sales report was released this morning. Sales are now down nearly 20% from their recent peak, below their pre-COVID highs and near where they were five years ago. That boom is now a whimper.

{kind=link}