This is the video recording of the October 20th, 2022, Weekly Town Hall w/ Willie Delwiche.

10/20/22 2:00 PM ET [Read more…]

Expert technical analysis of financial markets by JC Parets

This is the video recording of the October 20th, 2022, Weekly Town Hall w/ Willie Delwiche.

10/20/22 2:00 PM ET [Read more…]

From the desk of Willie Delwiche.

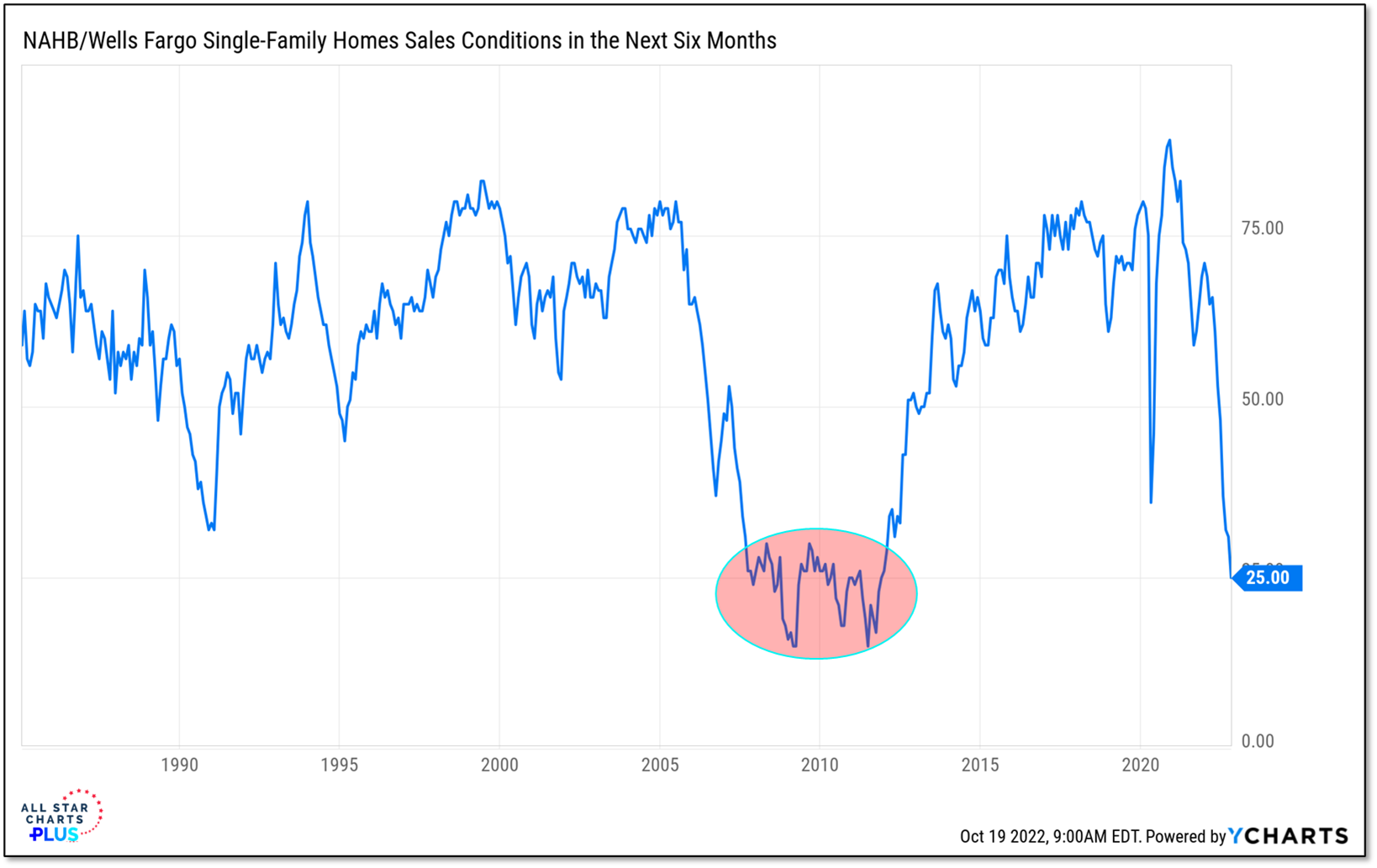

Feeling More Like The Financial Crisis

Mortgage rates are soaring and housing market conditions are deteriorating. Sentiment is sour in both the financial markets and the economy.

The Numbers: Expectations for home selling conditions are at a level that have been seen leading up to, through, and in the wake of the financial crisis. This isn’t an isolated report and its both sides of the market. Data from the University of Michigan shows that the fewest survey respondents since the early 1980’s see this as a good time to buy a house (and that was prior to the most recent spike in mortgage rates).

Why It Matters: Economic sentiment, whether on buying houses or CEO confidence, is usually self-fulfilling. This may seem to be at odds with the idea of using sentiment as a contrarian indicator, but it isn’t all that different. We can look at past sentiment extremes to gauge the possibility that moods have moved too far, but it takes bulls to have a bull market in the same way it takes optimism to have an economic expansion.

In this week’s Sentiment Report we take a closer look at the persistent pessimism that can be seen across the market. While the conditions might be ripe for a rally, the longer the bears have the upper hand, the more risk there is to stocks.

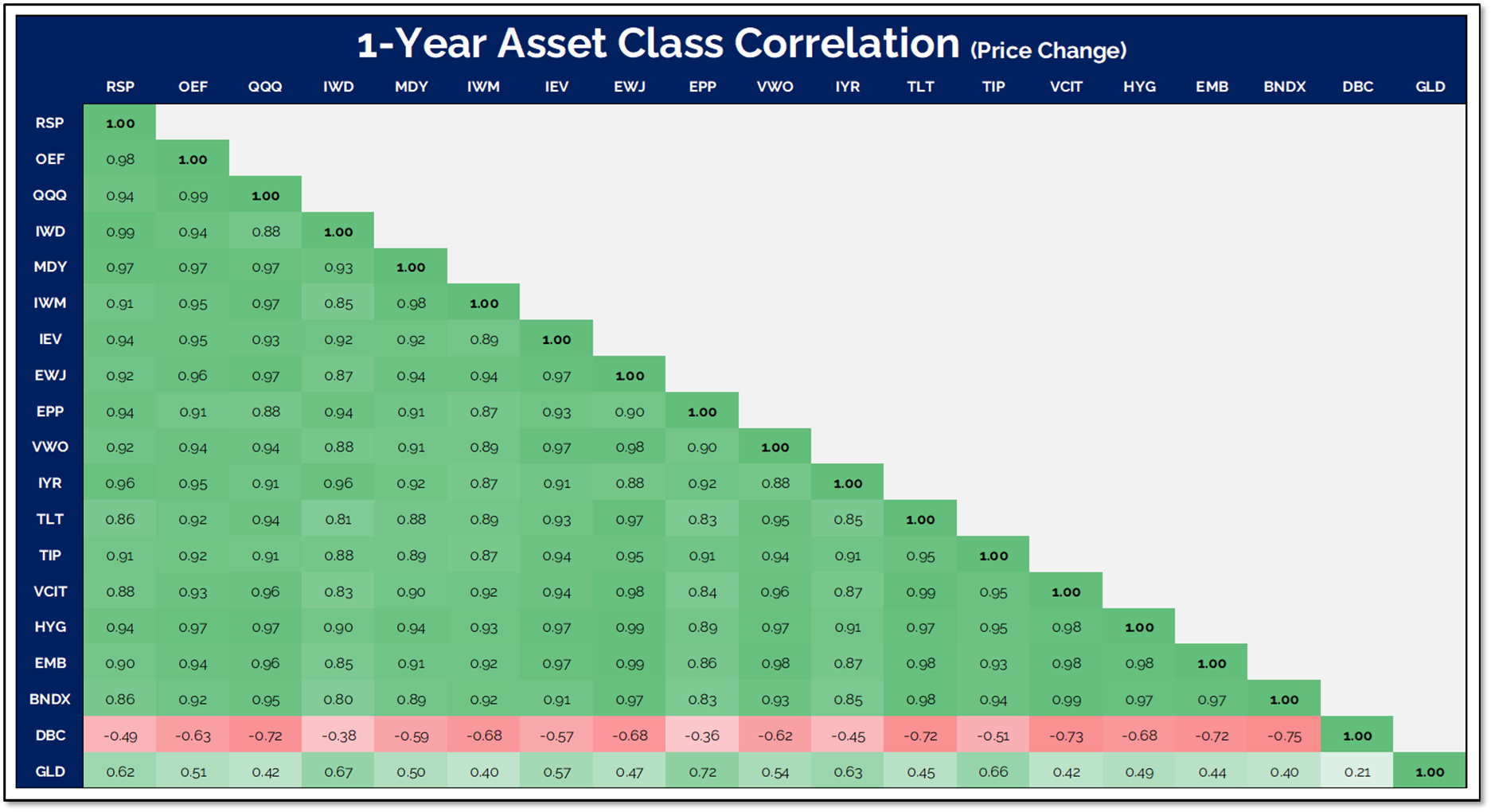

Over the past year, this old Wall Street saying has been more than an adage. It’s been a reality. Correlations across the ETFs that we use as proxies for various asset classes are overwhelmingly positive and on the rise. The exception has been Commodities (DBC), though many asset allocation conversations don’t even include commodities.

Why It Matters: Elevated correlations have left investors with no places to hide as stocks enduring historic levels of volatility and weakness. 2022 has been a risk off environment where risk off assets have been as weak as risk on assets. Trying to navigate this backdrop has led to frayed nerves and impatience for the arrival of better times. Unfortunately this year has done little to show it deserves the benefit of the doubt so far.

In taking a Deeper Look we put 2022 into context, review our indicators of risk behavior and highlight some areas where risk appetite may be improving.

From the desk of Steve Strazza @Sstrazza

Our Top 10 Charts Report was just published.

In this weekly note, we highlight 10 of the most important charts or themes we’re currently seeing in asset classes around the world.

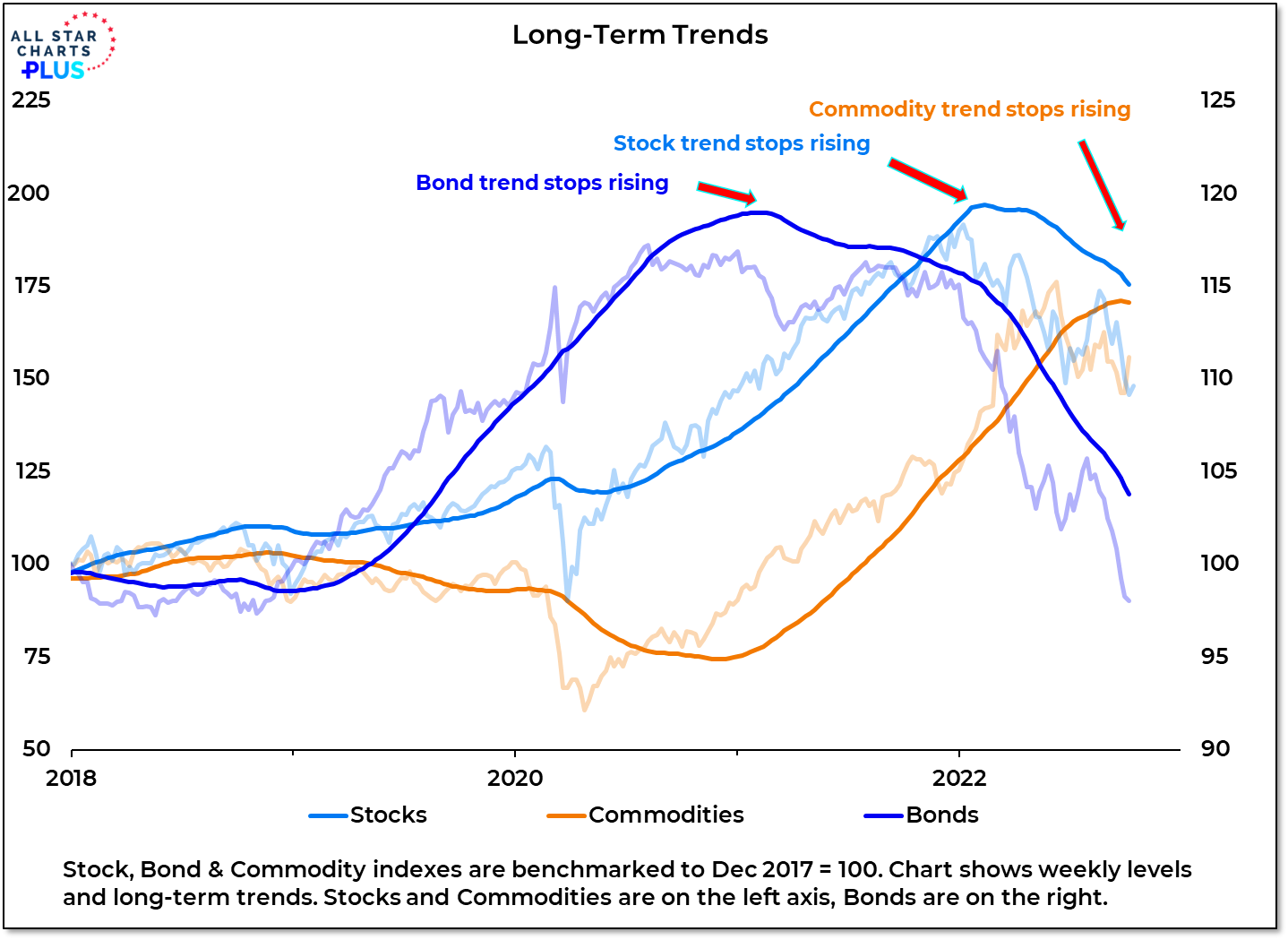

Bonds Lead

First bonds, then stocks, and now commodities have rolled over, following the traditional intermarket cycle. If the pattern holds, we should expect bonds to bottom first and eventually lead the way higher. With yields on the rise, there are no signs of this yet, but even a transition to a sideways trend could bring some stability to other asset classes.

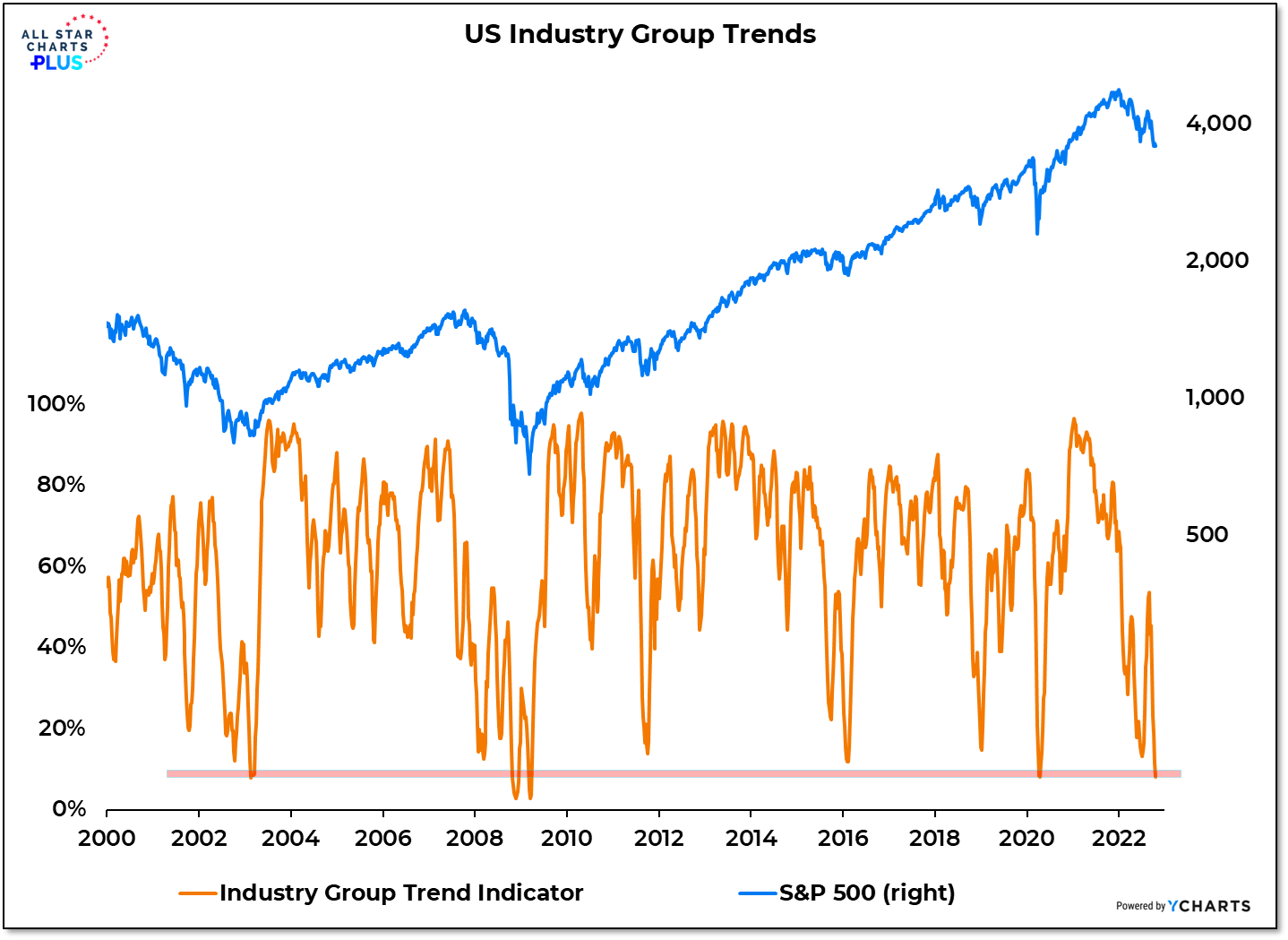

Taking Out The COVID Lows

US industry group trends are at a new low for the year and are approaching washed out levels. Take out the Energy groups and virtually nothing is in an up-trend.

The Details: The industry group trend indicator looks at 4 weekly trend metrics for each of the 72 industry groups in the S&P 1500 (24 each for small-caps, mid-caps and large-caps). The higher the number, the broader the strength at the industry group level.

More Context: From an industry group trend perspective, this is as bad as it got during COVID and during the bursting of the Tech Bubble. It was worse than this during the Financial Crisis (both during October 2008, which was not the low and March 2009, which was the low). We cannot know how bad it will get this time and so rather than anticipating a turn higher and improving conditions, I would rather wait for evidence of a turn and follow the trend higher.

We take a Deeper Look at what would give us confidence that a turn higher for stocks could be sustainable and where we are already seeing evidence of improvement.

From the desk of Steve Strazza @Sstrazza

Check out this week’s Momentum Report, our weekly summation of all the major indexes at a Macro, International, Sector, and Industry Group level.

By analyzing the short-term data in these reports, we get a more tactical view of the current state of markets. This information then helps us put near-term developments into the big-picture context and provides insights regarding the structural trends at play.

Let’s jump right into it with some of the major takeaways from this week’s report:

* ASC Plus Members can access the Momentum Report by clicking the link at the bottom of this post.

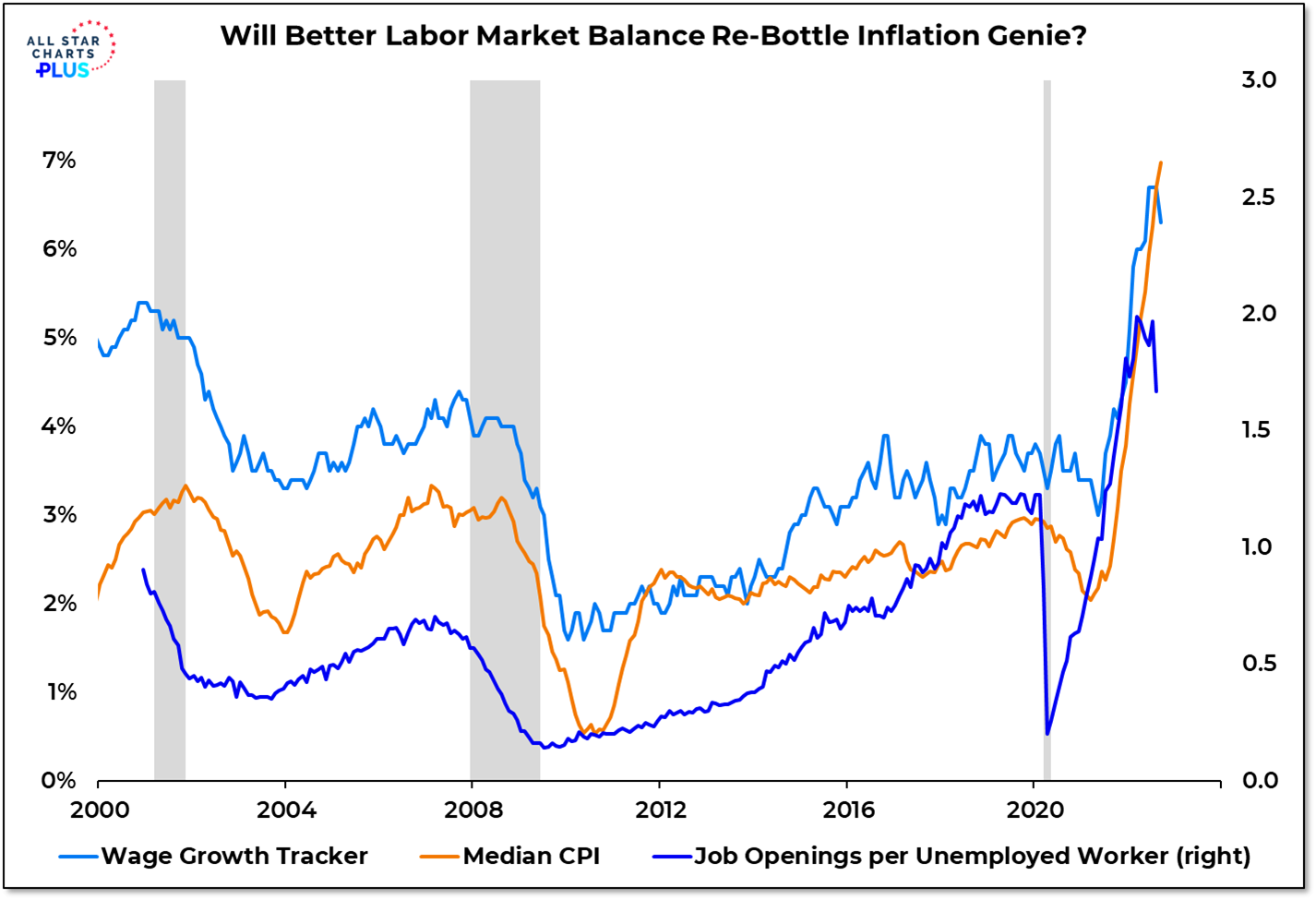

From the Desk of Willie Delwiche.

Labor Pressure Eases – Is Inflation Next?

The Chart:

On the labor front, job openings turned lower in August and the Atlanta Fed’s Wage Growth Tracker for September seems to have followed suit. On the inflation front, the year change in the median CPI reached another new high (its 7th in a row) in September.

Why It Matters:

Despite a bevy of other explanations, surging inflation has had more to do with imbalances in the labor market than anything else. A drop in job openings (while not a sign of strength) is a more preferable way to restore labor market balance than increased layoffs and unemployment. With wage growth now slowing, the hope is that inflation could soon peak. The challenge is that once the inflation genie is loose it can be hard to get under control – even if the initial causes are mitigated. In that regard, this month’s jump in inflation expectations reported with the University of Michigan Consumer Sentiment Survey is unwelcome news for the Fed.

This is the video recording of the October 13th, 2022, Weekly Town Hall w/ Willie Delwiche.

10/13/22 2:00 PM ET [Read more…]