With volatility on the rise and increased evidence of fissures beneath the surface of the market, we have reduced equity exposure in our Tactical Opportunity portfolio. The deterioration at this point has not been significant enough to warrant reducing equity exposure in our Cyclical portfolio, though we have made some changes there as well to stay in harmony with the relative leadership trends we are seeing both in the US and globally.

[PLUS] Weekly Market Perspectives – Rising Rates A Risk When Indexes Lack Broad Support

Key Takeaways:

- Bond yields rising as pressure mounts for Fed to raise rates

- From hints of new highs to expansion in new lows, the broad market is being tested.

- Commodities, currencies & bonds struggle with risk on message

With schedules of all sorts thrown off by travel and the Thanksgiving holiday (no Townhall conversation this week), this seems like a good chance to review a handful of charts that I’ll be keeping an eye on as we move toward year-end and into 2022.

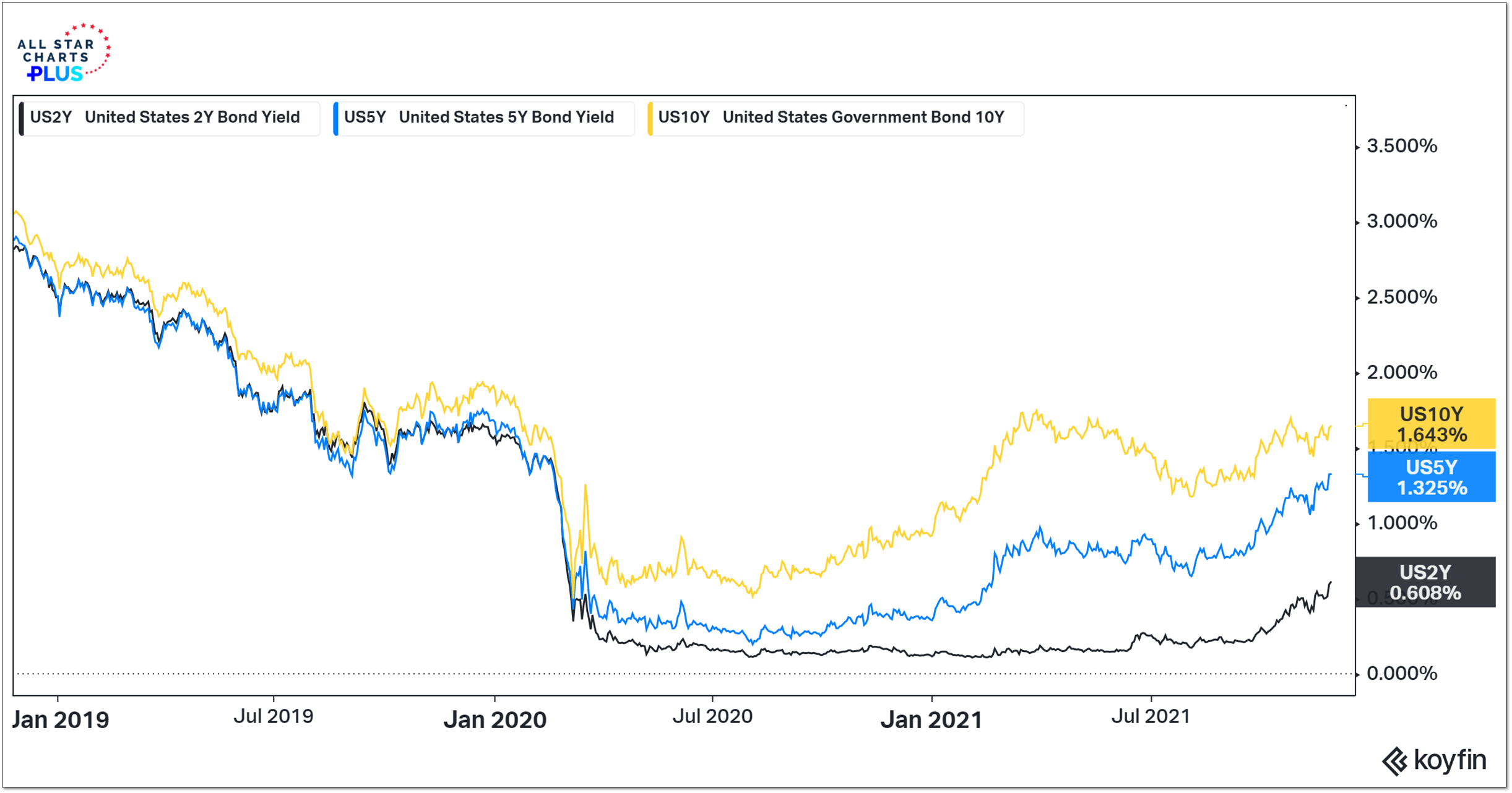

The 10-year T-Note yield continues to move between its March high (near 1.75) and its August low (below 1.20%). Yields on 2-year and 5-year Treasuries have climbed to new recovery highs as the market has priced in Fed tightening. Given the inflation outlook, much of the debate is on why bond yields are still so low. Take a look at a chart of a global bellwether like Caterpillar (CAT) and the question might become, why are bond yields so high.

[PLUS] Portfolio Perspectives – Market Looking For Inflation; Investors Looking For Options

Key Takeaways:

- Inflation pressures surge and market is looking for more

- Bonds pricing in rate hikes but real yields remain buried in negative territory

- Gold finally taking a shine to favorable fundamentals as price action improves

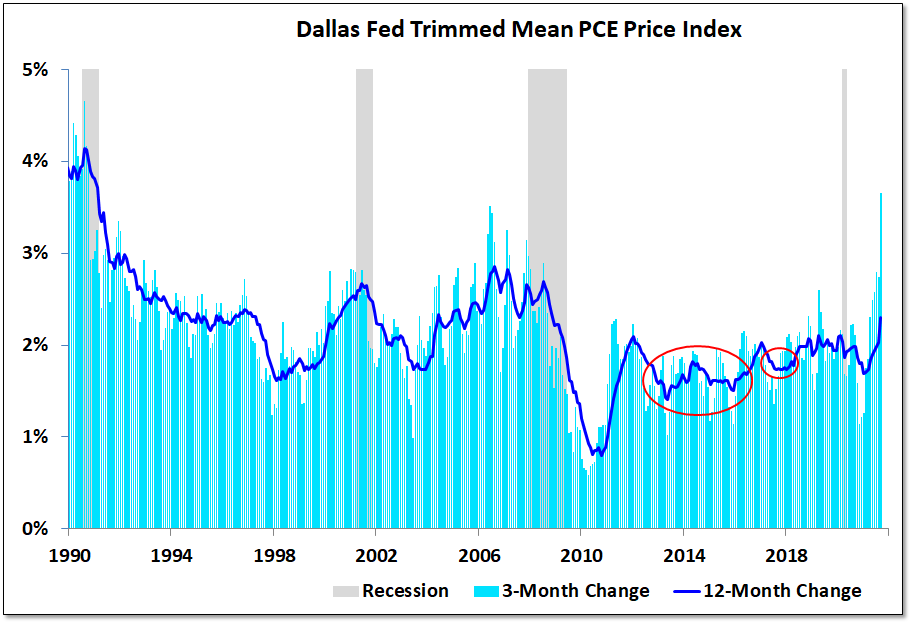

Fed Chair Powell has referred favorably to the Trimmed Mean PCE Price Index, published by the Dallas Fed, as a gauge of inflation that does a good job of tuning out noise and distilling the trend. Looking at this index, there have been a couple periods over the past decade when price pressures softened and inflation unexpectedly fell short of the Fed’s 2% goal. Even still, inflation bottomed in the immediate wake of the Great Recession and has been trending higher since. In the months prior to COVID, the Fed was hitting its inflation goal and the 12-month change in this index was edging up to its highest level in over a decade. Inflation has intensified over the past year for a variety of reasons, not least of which is the pressure that was already building beneath the surface. The market now is pricing in both elevated inflation and increasingly aggressive actions by the Fed and that has investors evaluating their options.

[PLUS] Portfolio Perspectives – Following Strength As World Looks For More Energy

Key Takeaways:

- Despite macro concerns, evidence tilts toward opportunity

- Energy sector strength benefitting active asset allocators

- Country-level leadership favors dirty energy over clean plays.

A recently published article in the Wall Street Journal reviews “5 reasons why stocks might be weaker in 2022.” Mostly it’s a list of macro concerns, from liquidity constraints to slowing profit growth to elevated valuations. I am sympathetic to a number of them – to a greater or lesser extent they factor into my consideration of the weight evidence. We need to balance our thinking about various things that could happen against an assessment of what is happening. As any sailor might attest, there can be a big difference between risks on the horizon and conditions that need to be navigated. You don’t make much progress if you drop the sail the moment there are storm clouds in the distance. There may be a time to reckon with some (or all) of those clouds at some point, but as we have been discussing in recent weeks, the evidence right is tilting toward opportunity. Market trends and momentum have turned bullish and expanding rally participation points to improving (not deteriorating) breadth.

[PLUS] Portfolio Perspectives – Bullish Evidence calls for Deploying Cash

We’ve made some changes to our ASC+Plus Dynamic Portfolios.

With the weight of the evidence turning more bullish, we have increased our equity exposure in the cyclical and tactical opportunity portfolios.

Within these portfolios we have also moved away from equity areas that are struggling to participate in the rally and re-focused exposure on areas that are experiencing upside momentum.

[PLUS] Weekly Market Perspectives – Positioning For Strength Around The World

Key Takeaways:

- China weakness has meant moving away from EEM for Emerging Market Exposure

- New highs from Taiwan could point to improving trends for China and EEM

- Canada benefitting from exposure to Energy & Financials

Emerging markets have been dealing with the opposite problem that we have discussed in the US. In the US, mega-cap strength has supported the indexes as conditions beneath the surface struggled. In Emerging Markets, mega-cap weakness (China accounts for nearly 22% of EEM) has weighed on the indexes as conditions beneath the surface improved. The goal of this piece is to help discuss how we will know if and when that condition changes.

Given the struggle at the top of the index, we have been utilizing India, Russia, and Saudi Arabia (which together account for 19% of EEM) for Emerging Market exposure. All three of these (as well as FM, Frontier Markets) have made frequent appearances on our new high lists.

[PLUS] Weekly Market Perspectives – Market Sending A Risk-On Message

Key Takeaways:

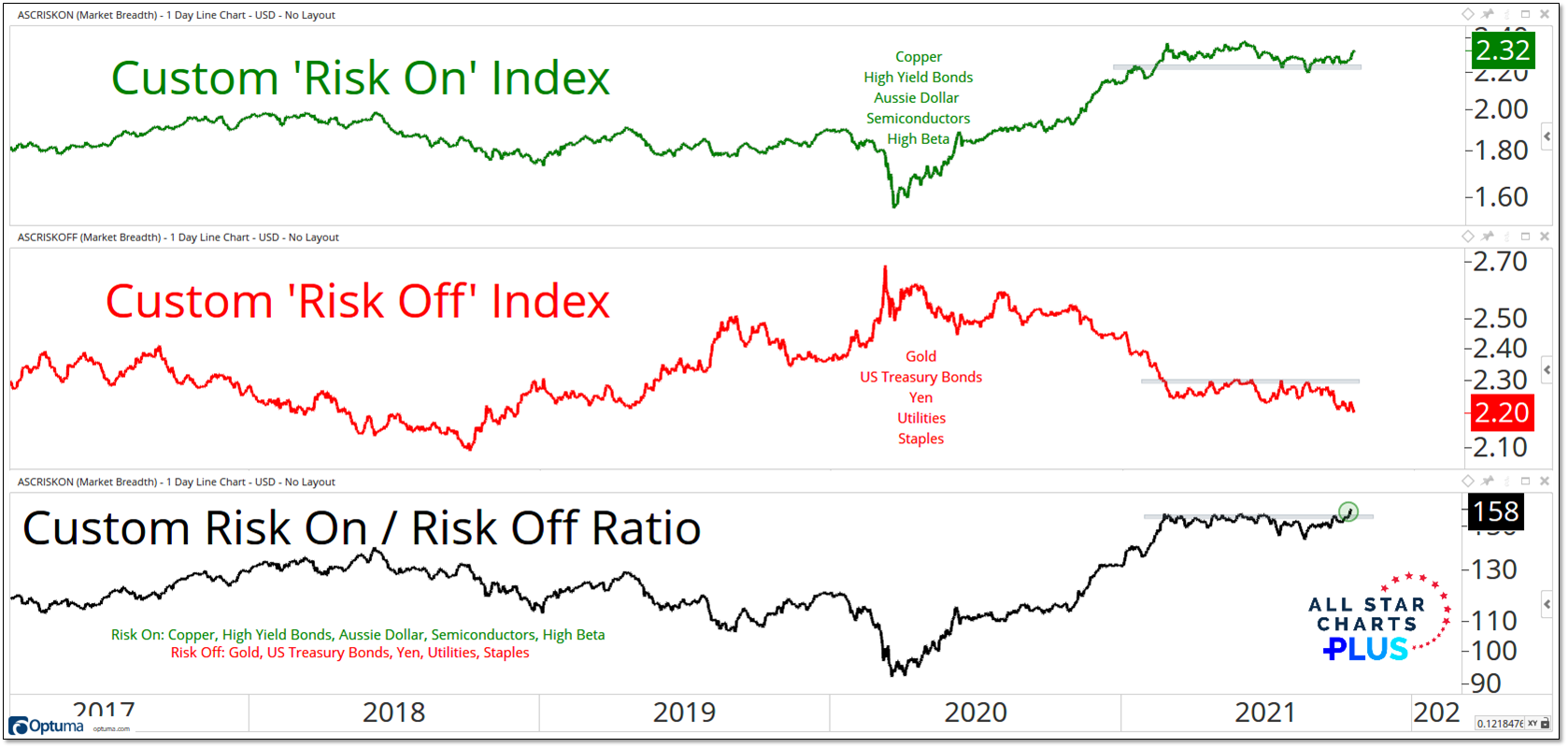

- Custom Risk On / Risk Off Ratio breaking out of an 8-month consolidation

- Risk On environment favors Emerging Market strength and leadership from Financials

- Intermarket analysis shows higher risk assets outperforming across multiple timeframes

Our ‘Risk On’ / ‘Risk Off’ Ratio is getting back in gear after spending most of 2021 going sideways. The ratio first peaked in February and while it visited and revisited that level multiple times as Spring became Summer, which then became Fall, it had not been able to break out until last week. The improvement in the ratio has been fueled by both an up-turn in the ‘Risk On’ index and a more pronounced down-turn in the ‘Risk Off’ index. On the following pages we will take a closer look at what is driving improvement in one and deterioration in the other.

The break-out in our ‘Risk On’ / ‘Risk Off’ ratio is consistent with the improving momentum backdrop being seen at the sector level and would be consistent with a more favorable seasonal backdrop as we move toward year-end. This ratio getting back in gear would be consistent with Emerging Markets continuing to show strength and Financials remaining in a leadership position.

[PLUS] Weekly Macro Perspectives – Can Earnings Surprises Stay Stellar?

Key Takeaways:

- Analysts and economists no longer chasing reality higher

- Downward earnings revisions coming with stocks priced for perfection

- Persistent inflation and higher bond yields would be a new experience for many investors

The past year has been one of widespread earnings surprises and large upward revisions. Whether those trends can remain intact as Q3 earnings season gets underway is one of the more important questions the market has to wrestle with right now. Expectations are elevated going into the quarter, but a number of the factors that fueled the earnings strength of the past year are starting to ebb. I have my suspicions that Q3 earnings season will be a repeat of the recent past.

At the end of the day, price is what pays. We don’t want to forget that, but we also want to keep an eye on whether (and how) investors’ expectations are being met or not. In each of the first two quarters of 2021, the earnings growth rate at the end of earnings season was nearly 30 percentage points higher than what was expected when the quarter ended. That is a clear case of expectations being exceeded – and to a historically high degree.

- « Previous Page

- 1

- …

- 4

- 5

- 6

- 7

- 8

- 9

- Next Page »