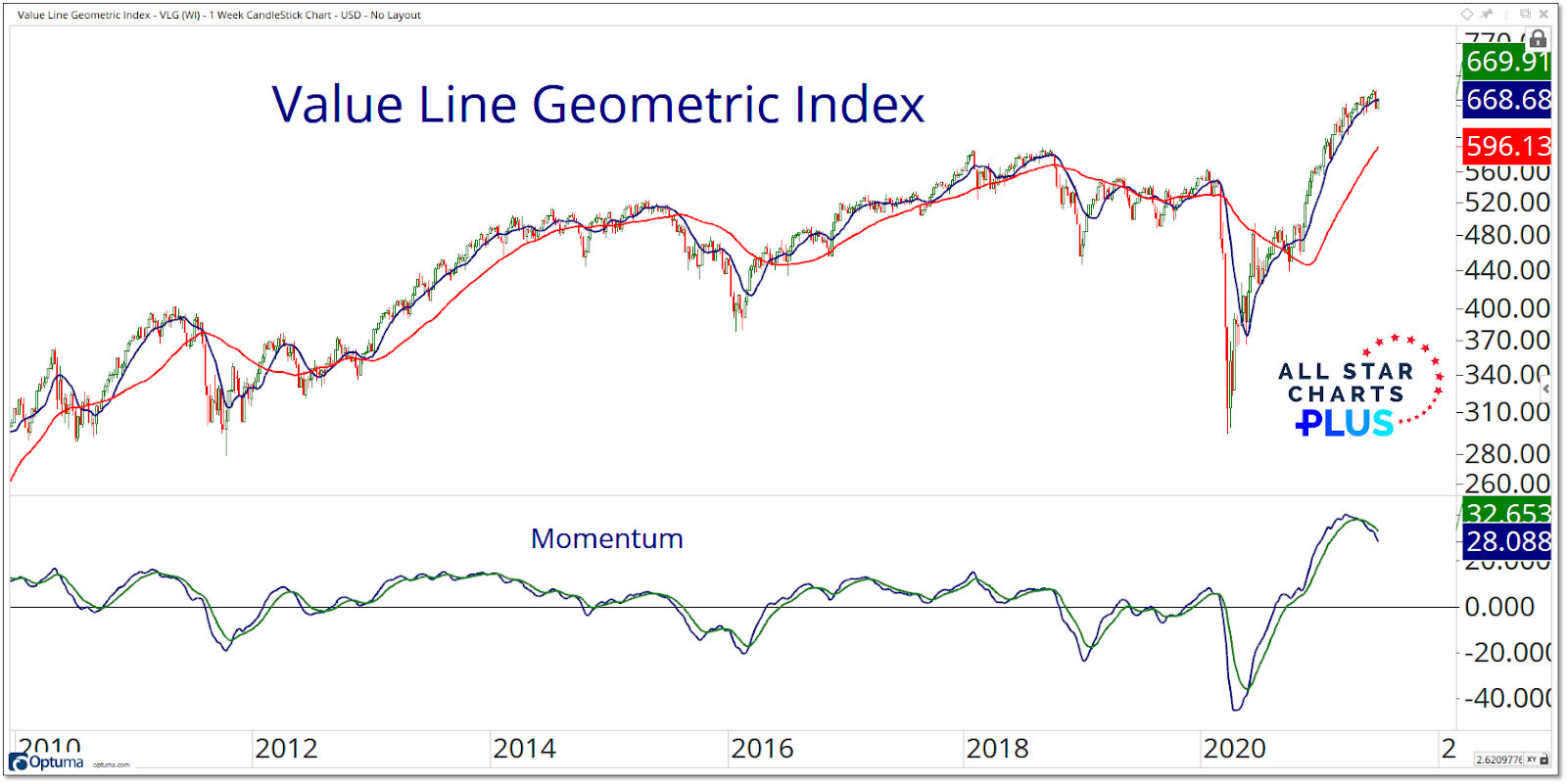

The Value Line Geometric Index has moved from new high to below its 10-week average in the space of a week. Momentum has peaked and is moving lower. [Read more…]

Expert technical analysis of financial markets by JC Parets

The Value Line Geometric Index has moved from new high to below its 10-week average in the space of a week. Momentum has peaked and is moving lower. [Read more…]

2020 was a remarkable year in many ways. The rally that emerged off of the early year lows was broad-based and historically strong. It was fueled by numerous momentum surges, overwhelming amounts of fiscal and monetary liquidity, an unprecedented string of better than expected economic data, and a persistent trend in earnings estimates being revised higher. While 2021 began with some of those tailwinds intact, as we move toward the second half of the year, we want to avoid the assumption that nothing has changed as we have entered year two of the cyclical rally.

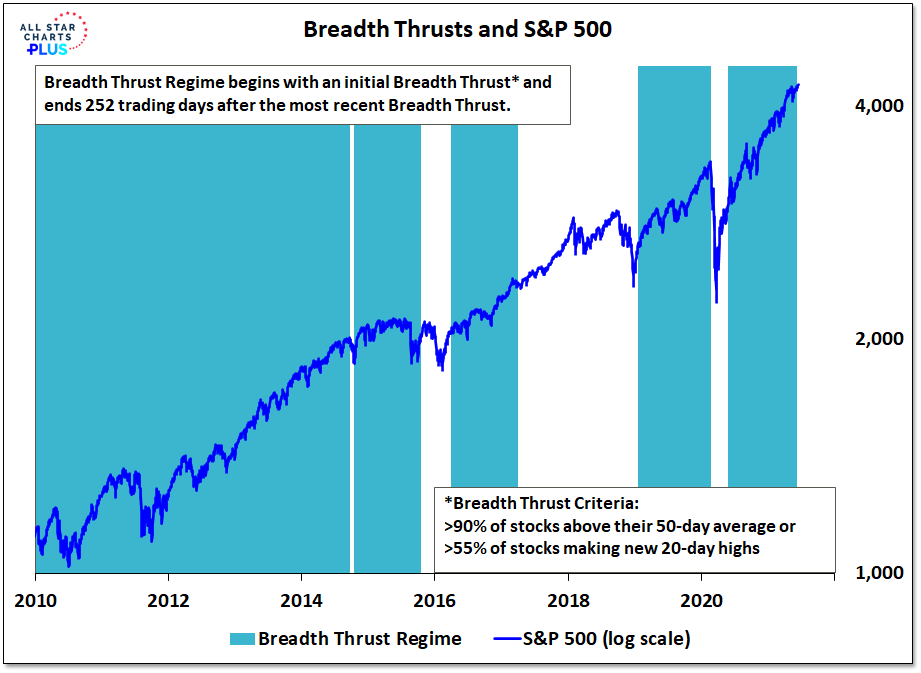

Breadth thrusts can signal strong and sustainable upward momentum for stocks that can last for up to a year. Our two favorite indicators are having 90% of stocks above their 50-day averages and/or 55% of stocks at new 20-day highs. These indicators last sent signals in late May and early June last year, and the breadth thrust regime from those signals has now expired. All of the net gains for the S&P 500 since 2010 have come during breadth thrust regimes. The path forward could remain rocky without another round of breadth thrusts.

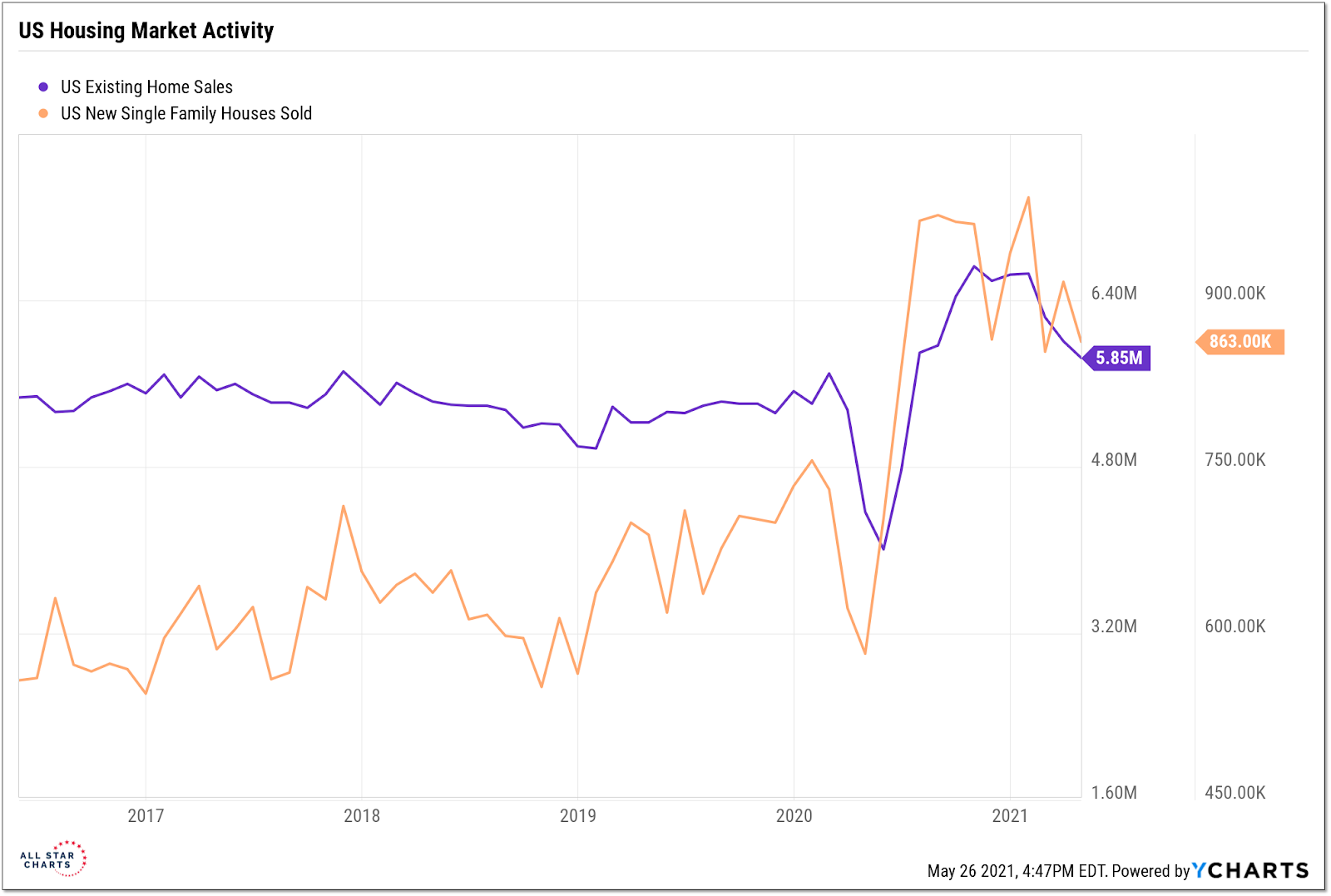

I’ll start by acknowledging more questions than answers on this subject. But that itself is part of the point. The housing market was one of the earliest parts of the economy to bounce back last year, but activity in recent months has been more uneven. Existing home sales in April unexpectedly fell (and are at their lowest level since June) and new home sales fell more than expected last month and data for the preceding month was revised lower. There is evidence that supply constraints (in terms of both current housing stock as well as workers and supplies necessary to build additional units) are weighing on activity. But when something as diverse and complex as the national housing market gets wrapped up in a narrative that is almost universally endorsed, I get more than a little skeptical.

While the Fed is musing about tapering, the market, as usual, is already in action. Upward momentum in bond yields and an economy that has soaked up liquidity have become headwinds for equities at a time when investors are already re-thinking risk appetites.

The S&P 500 is a week and a half removed from its highest weekly close on record, but many of the areas of the market that saw the biggest run-ups over the past 2+ years are in the midst of tumultuous pullbacks. After gaudy returns on the way up, investors should expect equally gaudy reversals on the way down. By way of example, the ARK Innovation ETF is more than 30% off its peak but is still up 180% since Jan 2019. Bitcoin too is 30% from its high but is still up 1000% since Jan 2019. These moves make the action in small-cap growth (15% below where it was in Jan 2021 peak but still 70% above where it was in Jan 2019) staid by comparison.

From the desk of Willie Delwiche.

Key Takeaways:

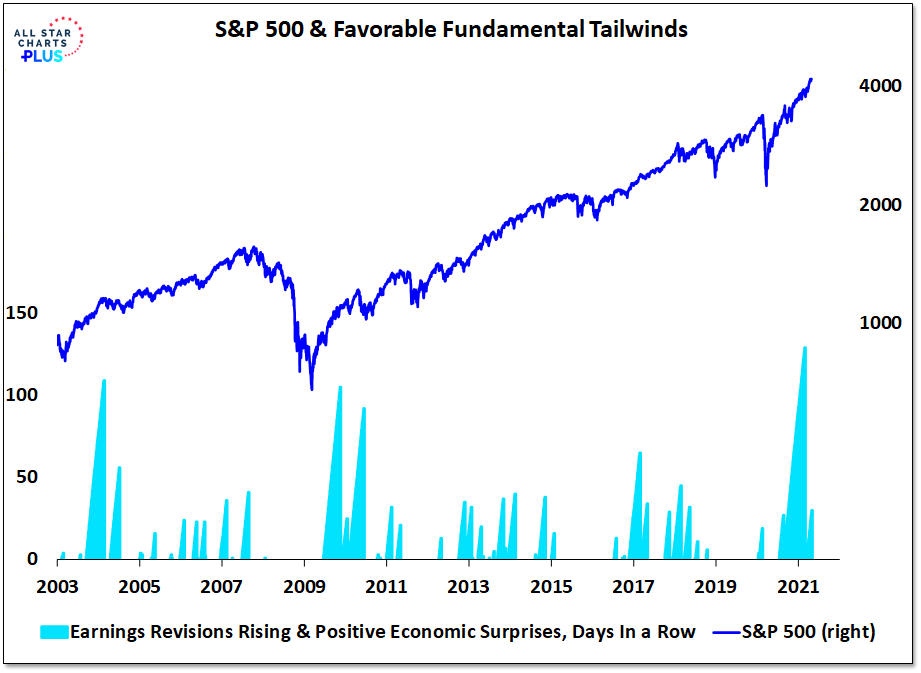

The S&P 500 has benefitted from an unprecedented string of good news. The economic surprise index has been positive since June (the longest continuous streak on record) and for most of that time has been accompanied by a rising earnings revision trend. Since 2003, this combination of positive economic surprises and rising earnings revisions have occurred less than 30% of the time. But in that environment, the S&P 500 has risen at a 20% annual rate, versus an overall annualized gain of 8.7% since January 2003.

From the desk of Willie Delwiche.

Key Takeaways:

The word perspective has multiple definitions. The dictionary we have at our house lists eight. For me, the most relevant of those have to do with seeing the interrelationships of relevant facts and ideas as well as those that deal with distant time frames & horizons.

When it comes to investing, keeping perspective is the difference between success and failure. A successful approach to portfolio management can be built on a sturdy three-legged stool of perspective focusing on:

We need to keep in mind how we are making sense of incoming information, how our preferences are changing in light of that information, and how far out in the future we are looking when it comes to how we are positioning our portfolios. When we lose track of any of these, the stool topples and the noise of the market can crescendo to a deafening din. This seems especially to be the case in the current environment, which offers many compelling arguments that reach starkly different conclusions.