From the desk of Willie Delwiche.

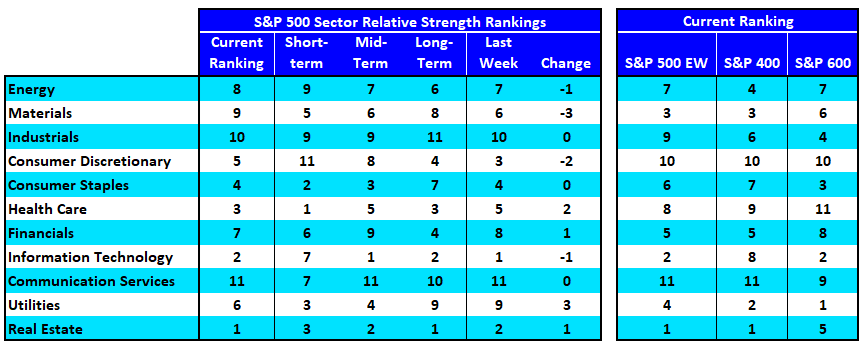

- Entering 2022, Real Estate, Technology, Health Care and Consumer Staples hold down the top spots in our S&P 500 sector relative strength rankings.

- Our industry group-based heat map shows deteriorating conditions across Energy and Financials and improving conditions in Staples and Utilities. Leadership from defensive groups is not usually consistent with risk-on behavior.