This is the video recording of the March 17th Weekly Town Hall w/ Willie Delwiche

03/17/22 2:00 PM ET [Read more…]

Expert technical analysis of financial markets by JC Parets

This is the video recording of the March 17th Weekly Town Hall w/ Willie Delwiche

03/17/22 2:00 PM ET [Read more…]

To the surprise of no one, the Federal Reserve voted to raise its target fed funds rate at yesterday’s FOMC meeting. The 25 basis-point rate hike was fully priced into the futures market. There was only one dissenting vote – St. Louis Fed President Jim Bullard expressed a preference for a 50 basis point hike at this meeting.

I’ll admit I was surprised that neither Esther George (from the Kansas City Fed) or Loretta Mester (from the Cleveland Fed) joined Bullard in his dissent. At the end of the day, the Fed is now in tightening mode, and the pace of tightening is likely to pick up over the course of the year between the combined effects of interest rate hikes and balance sheet drawdowns.

I’m not going to parse the FOMC statement, dissect the dot plot, or break down the summary economic projections. Much of what needs to be said (and a lot of what didn’t need to be said) about the Fed’s decision has been offered in print, over the airwaves, and in our virtual communities.

From the desk of Willie Delwiche.

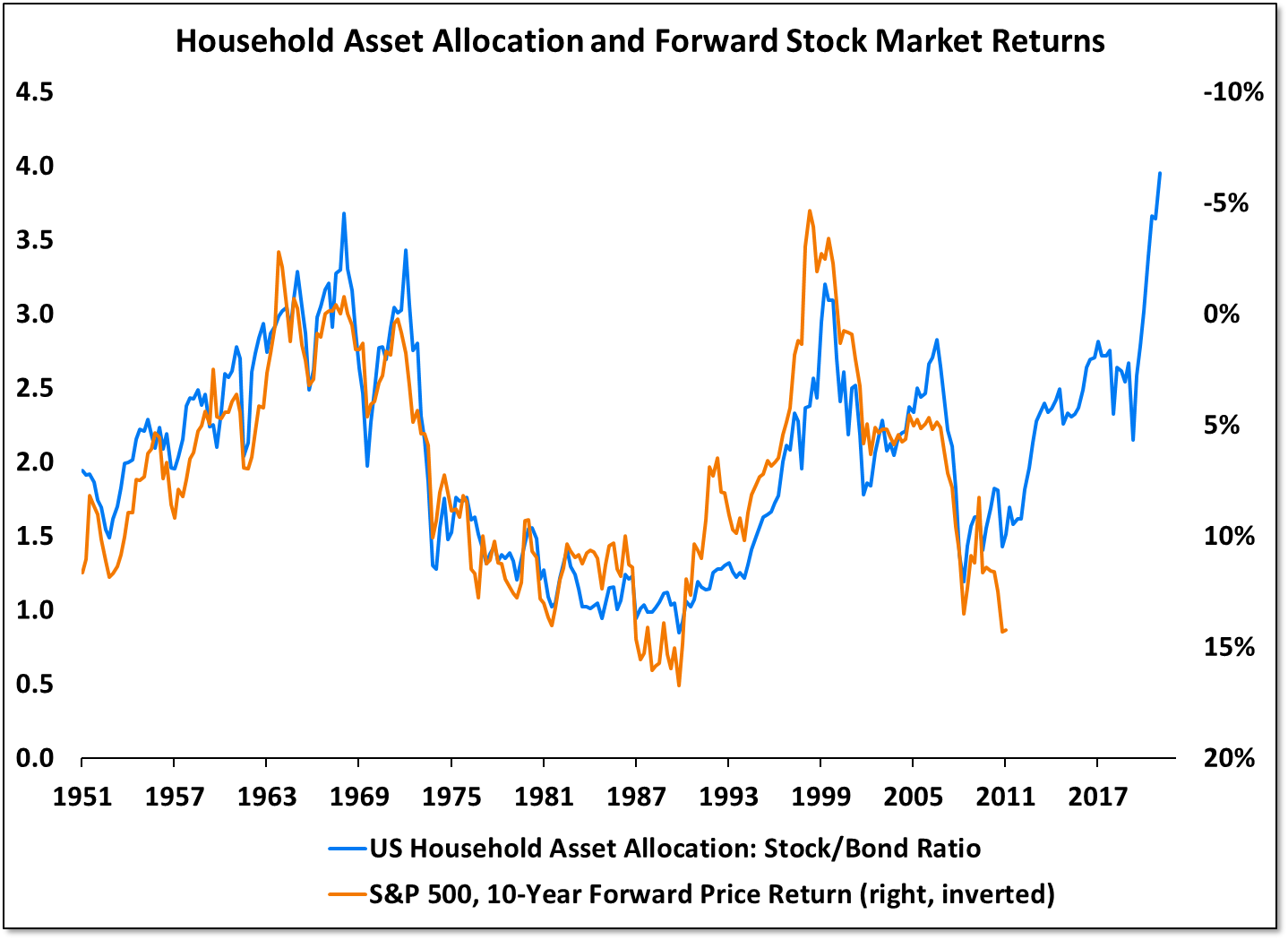

Key Takeaway: There is abundant focus on weekly and monthly surveys showing evidence of investor pessimism with regard to equities. This is at odds with the strategic positioning indicators showing that stocks are expensive and households are historically over-exposed to equities (relative to bonds, but also relative to bonds plus cash). The last two times that II bears exceeded bulls (in 2019 and 2020), household asset allocation data showed only 53% exposure to equities. As of the end of 2021, it was at 62%, an all-time high. So while investors may be identifying themselves as bearish, there is little evidence that investable cash is on the sidelines. With the Fed now raising rates and the market re-considering valuation levels, this lack of available firepower could weigh on equities. Whether today’s pessimism represents a cyclical extreme remains to be seen.

Sentiment Report Chart of the Week: Household Equity Exposure Hits New High

US households finished 2021 with their highest level of equity exposure on record. Households had 62% exposure to stocks, 16% exposure to bonds and 22% exposure to cash.This is quarterly data, meaning it doesn’t reflect changes in market value or fund flows that have occurred this year. Nonetheless, there is a strong inverse relationship between equity market exposure (relative to bonds) and forward returns for the S&P 500 that goes back to the 1950s. If this relationship holds going forward, stock market returns could be disappointing for an investing public that has gone all in for equities.

Key Takeaways:

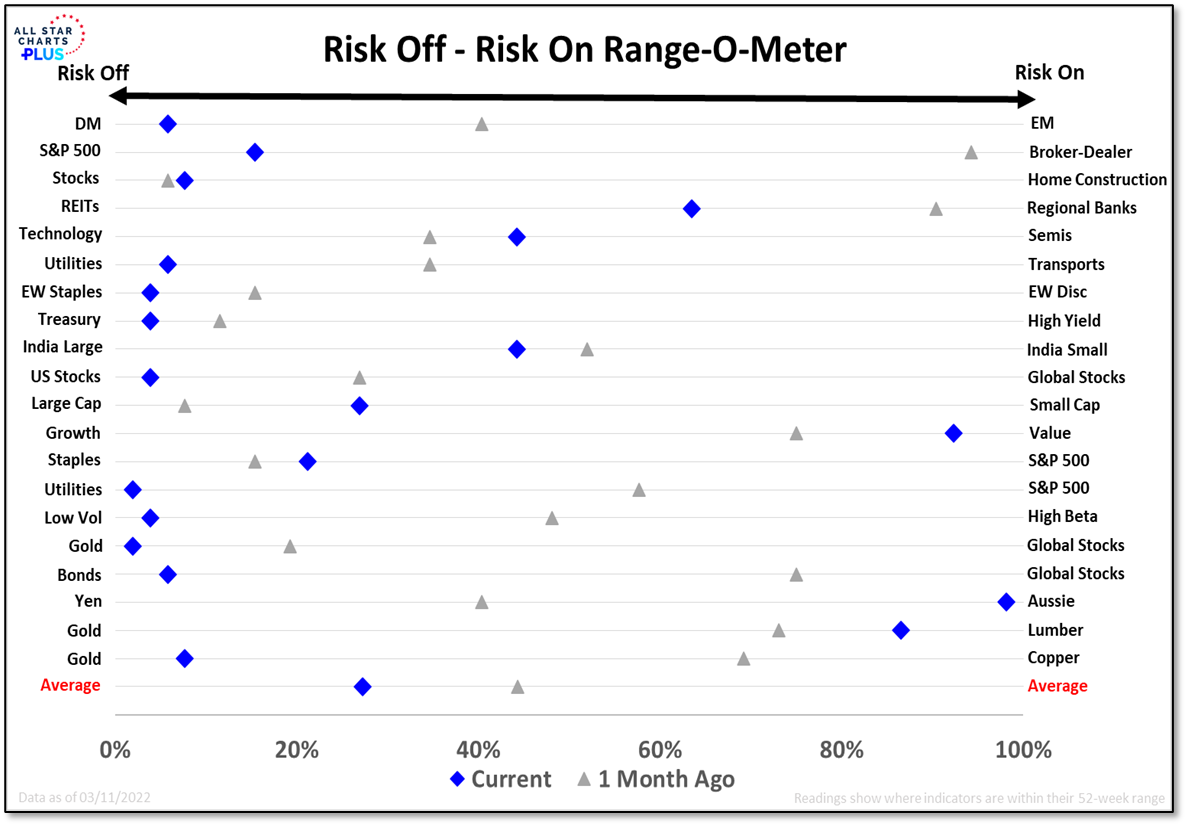

The headlines remain noisy, but the message of the market is one of risk off leadership. Our Risk Off – Risk On Range-O-Meter shows the risk off component in most of these asset pairs gaining strength. Of the 20 pairs displayed here, only three (Value vs Growth, Aussie Dollar vs Yen, Lumber vs Gold) have the risk on component anywhere near new relative highs. In more than half the cases, the risk off component is within 10% of its highest level in the past year. This pair-wise intermarket view confirms the message from our Weight of the Evidence dashboard that argues for caution as conditions have deteriorated. The rest of this piece puts the current readings from this range-o-meter into some historical context and takes a closer look at our ASC+Plus Risk On & Risk Off Indexes.

From the desk of Willie Delwiche.

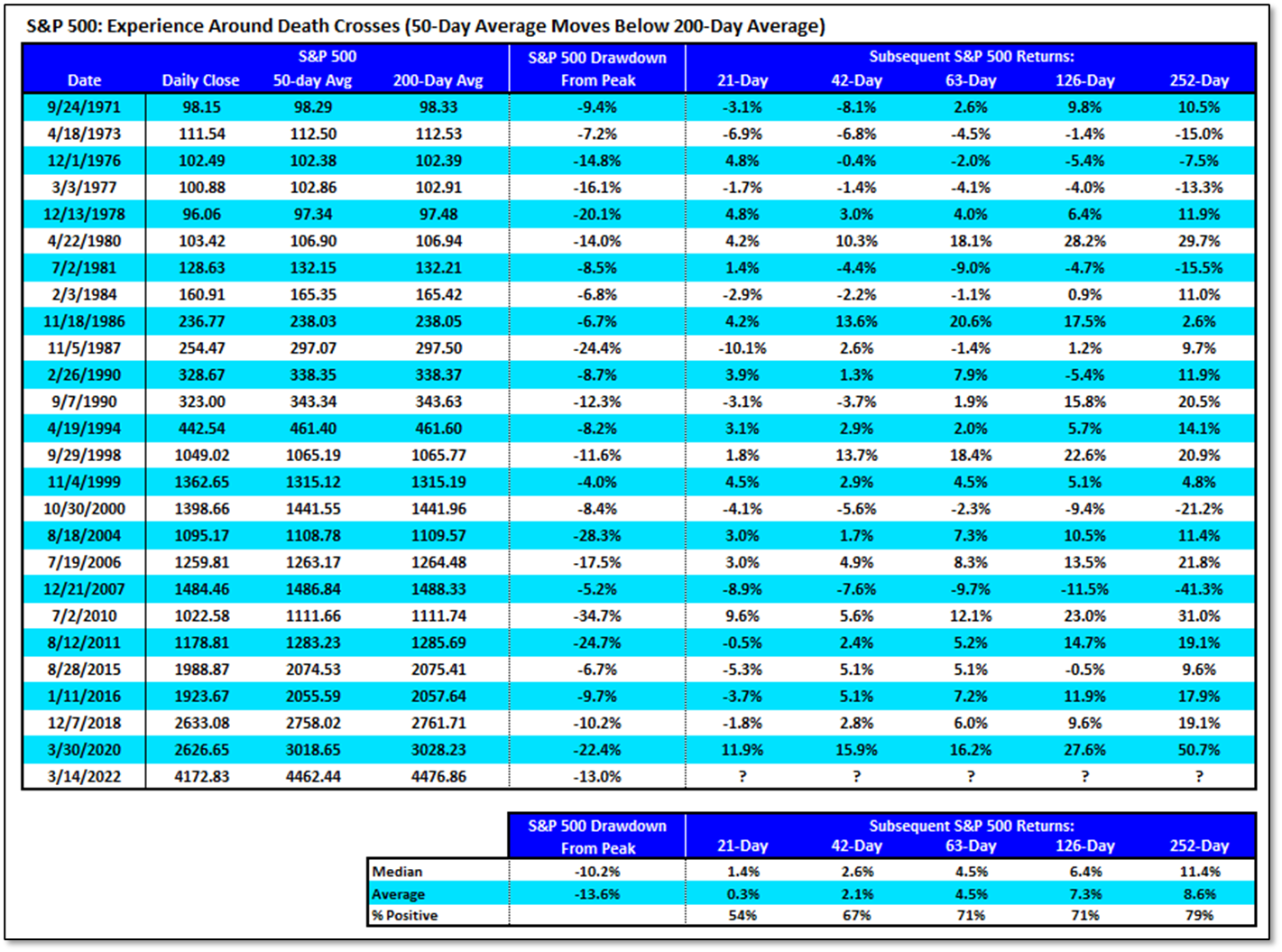

In aggregate, forward returns following Death Crosses are not meaningfully different from any random day in the market over the past 50 years. This is more noise than news and these crosses mostly reflect an index that has pulled back from its peak. The S&P 500 is currently 13% below its January peak, which puts the current Death Cross in line with the historical pattern. The relationship between the 50-day average and the 200-day average describes an environment but is not likely to shape the path going forward.

From the desk of Willie Delwiche.

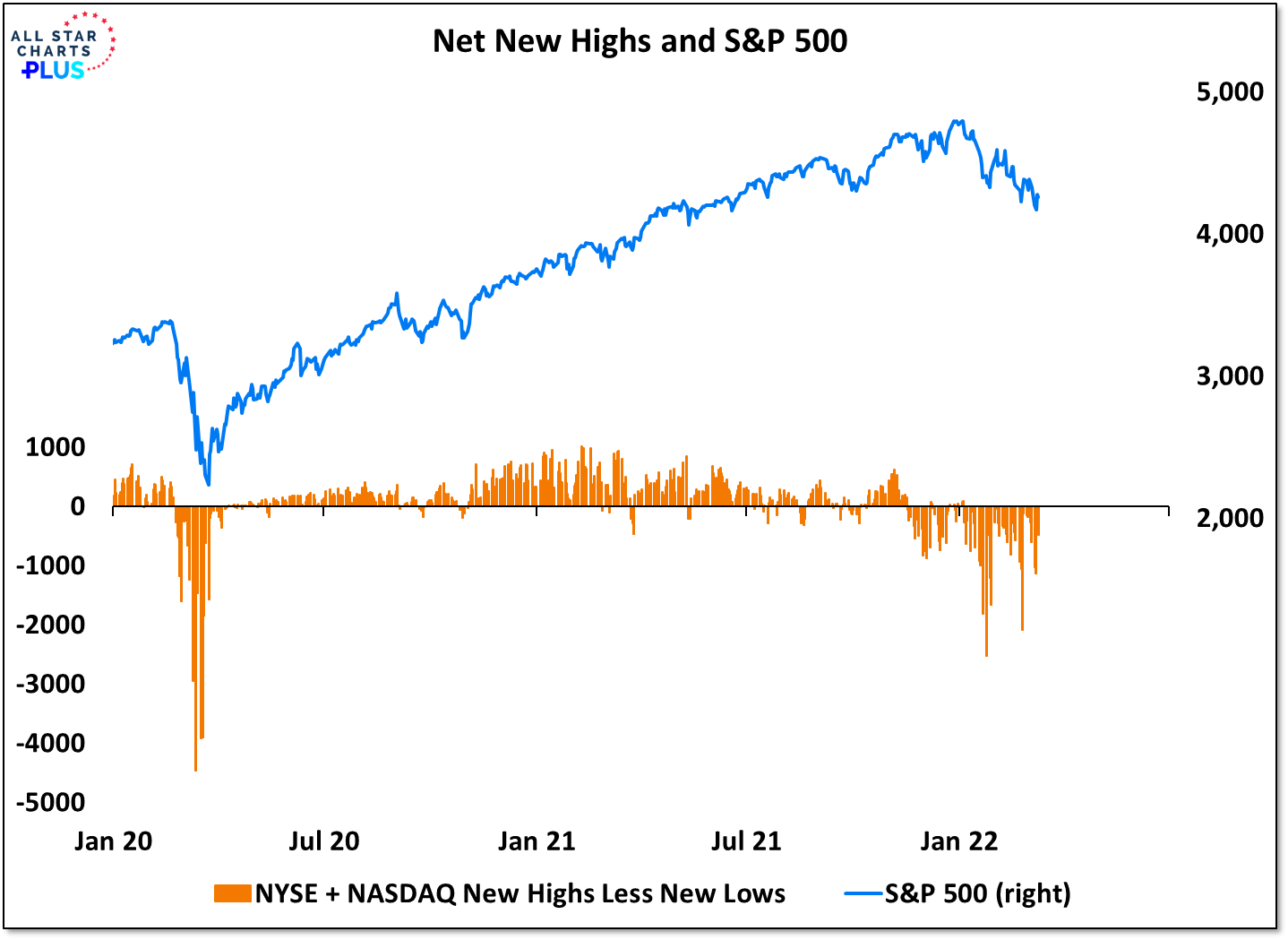

Stocks attempted to rally this week. Following Tuesday’s abortive attempt to regain the considerable ground lost on Monday, the S&P 500 posted its best daily gain since 2020 on Wednesday (+2.65). The S&P 500 is still down on the week as I write this, but if the right headlines cross the wire this afternoon, anything could happen. That’s the kind of environment we are in. One filled with plenty of day-to-day noise. Stepping back, the S&P 500 attempted to rally off the lows in both January and February as well. Then, lower highs were ultimately followed by lower lows. The consistent theme as the indexes have moved lower off of their early year highs has been weakness beneath the surface. The number of stocks making new lows has been persistently higher than the number of stocks making new highs. When that changes, and we see evidence of meaningful improvement in breadth, we can take a more constructive view of rally attempts. For they deserve skepticism. Let’s make it a mantra (or at least a T-shirt): “No Thrust? No Trust!”

This is the video recording of the March 10th Weekly Town Hall w/ Willie Delwiche

03/10/22 2:00 PM ET [Read more…]

From the desk of Willie Delwiche.

This isn’t a post about nuclear Armageddon or a survival guide for a post-apocalyptic world.

But it is about recognizing when something has ended.

In rare cases, we know when an end is coming and can try to prepare. This was the case with my son’s final grade school basketball game. The season-ending tournament was on the calendar months in advance. But even still, there were a few tears when the final buzzer sounded.

In other cases, we might not know in advance that an end is coming, but can quickly recognize that it has arrived. Think about going home from the office for the last time as the COVID crisis was intensifying in Spring 2020. Few knew when they shut their computers down for the day that it would be weeks or months (if ever at all, in my case) until they returned. Though unexpected, that reality became obvious in short-order. [Read more…]

{kind=link}