From the desk of Willie Delwiche.

Expert technical analysis of financial markets by JC Parets

This is the video recording of the June 2nd Weekly Town Hall w/ Willie Delwiche.

06/02/22 2:00 PM ET [Read more…]

From the desk of Willie Delwiche.

Key Takeaway: Investor moods will change as prices fluctuate but they seemed to follow word with deed in May. The AAII asset allocation survey showed them lightening up (perhaps only briefly and modestly) on their equity exposure. By month-end, we had evidence that the $4.5 trillion in money market funds (more of a molehill than a mountain when adjusted for total market value) was being put to work in both stocks and bonds. Bearish investors are not so much disgruntled with stocks, but disgusted by the price action they have experienced this year. It didn’t take much of a move off the lows for optimism to start building again. Rallies that are initially despised (or at least viewed skeptically) are more likely to have staying power than those that are quickly embraced. Sentiment is at levels from which rallies tend to emerge – positioning, however, is not.

Sentiment Report Chart of the Week: Investors Take Some Action

AAII asset allocation data shows that investors trimmed their equity exposure last month. pulling back from 70% in April to 67% in May. Bond exposure moved up from 13% to 14% and cash increased to 19%. Two things are worth pointing out here:

Key Takeaway:

From the desk of Willie Delwiche.

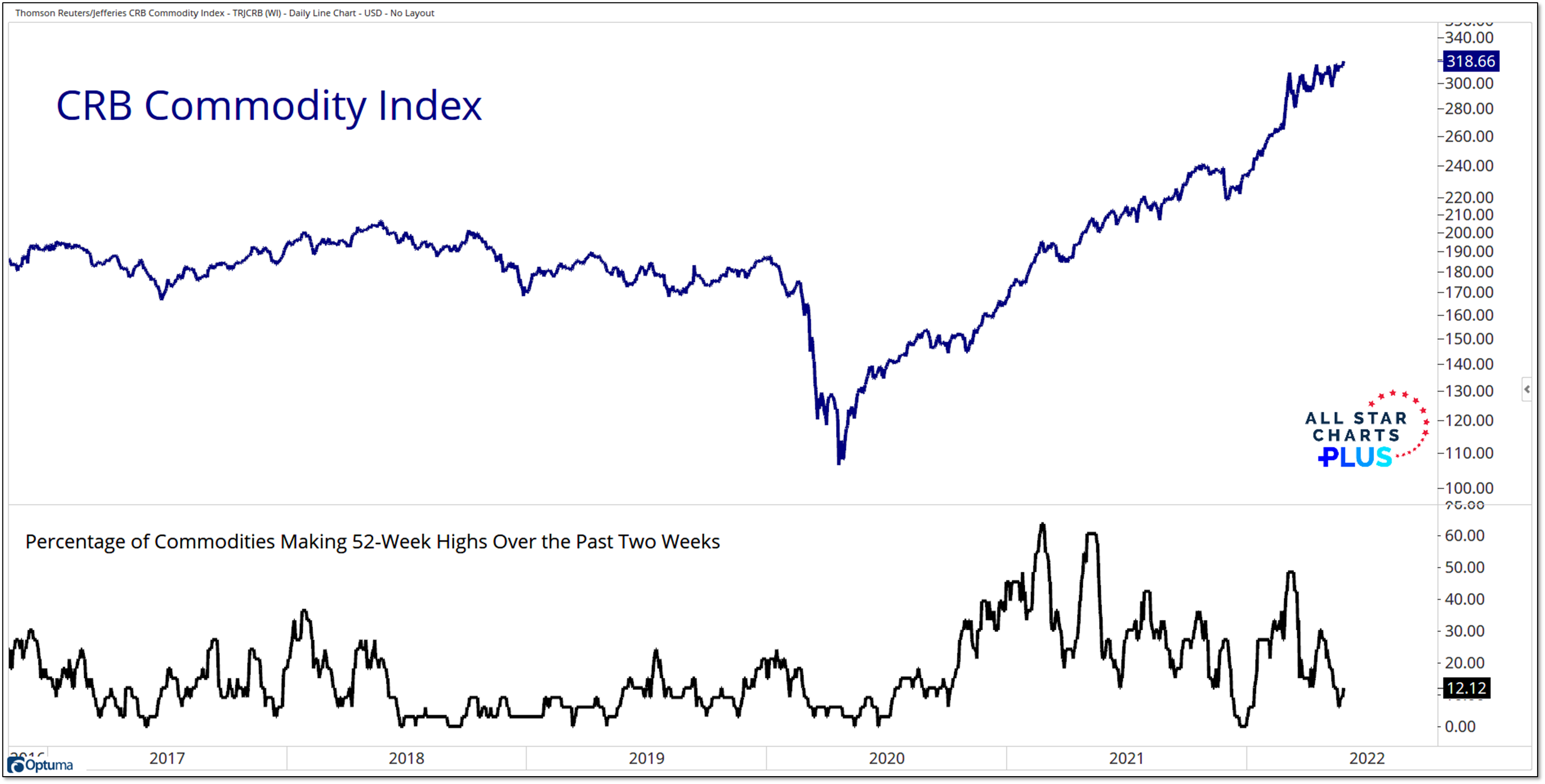

In a year marked by broad weakness in both stocks and bonds, commodity strength has provided some portfolio ballast for those who have been willing and able to expand their asset allocation opportunity set. After several weeks of consolidation, the CRB commodity index is again making new highs. But rally participation looks to be narrowing. Only 12% of the commodities in our ASC Commodities universe have made new 52-week highs in the past two weeks. This was as high as 50% earlier this year. Perhaps not surprisingly, our equal-weight commodity index has not confirmed the strength in the CRB index (which has heavy tilting toward energy-related commodities). I think Bob Farrell’s Rule 7 applies here: “Markets are strongest when they are broad and weakest when they narrow.” Strength in the CRB index is more likely to persist if it’s not just energy fueling the advance.

This is the video recording of the May 26th Weekly Town Hall w/ Willie Delwiche.

05/26/22 2:00 PM ET [Read more…]

From the desk of Willie Delwiche.

The minutes from the May FOMC meeting were released this week, leading to renewed “will they or won’t they” discussions about potential rate hikes later this year.

I’m old enough to remember when FOMC minutes weren’t really a thing. I liked it better then. I also preferred when Fed officials (both Board Governors and Regional Bank Presidents) were rarely seen, and even more scarcely heard. But I digress…

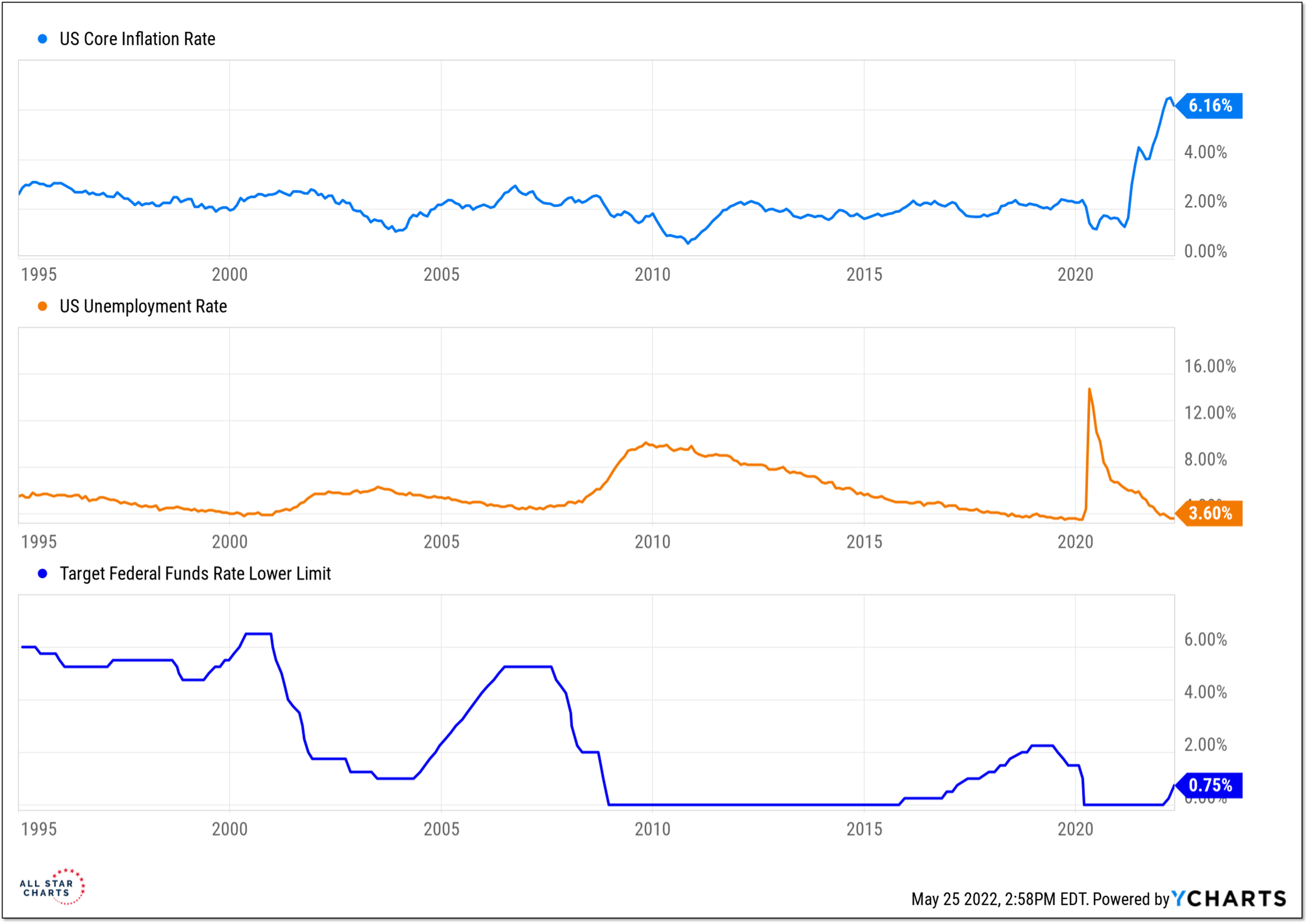

When thinking about where rates have gone in the past and where they could go in the future, it’s helpful to remember the context of the Fed’s dual mandate (stable prices and full employment). The last three tightening cycles all began with lower inflation & higher unemployment rates than we have now.

From the desk of Willie Delwiche.

Key Takeaway: Fear and concern are at the tip of every investor’s tongue, yet their eyes remain on the market. For all the pessimism suggested by sentiment surveys, there’s still a great deal of hope as the desperate search for the bottom continues. Yes, put call ratios are on the rise but that’s mostly driven by falling call activity as last year’s speculative exuberance evaporates. Also, investors continue to favor equities over more defensive assets such as bonds and cash despite what they say. Caution remains warranted until attitudes change or market participants are forced to avert their gaze out of disgust. After we see evidence of improved price action (and likely a series of breadth thrusts), accumulated pessimism becomes fuel for a rally, but the timing of that turn is anybody’s guess at this point.

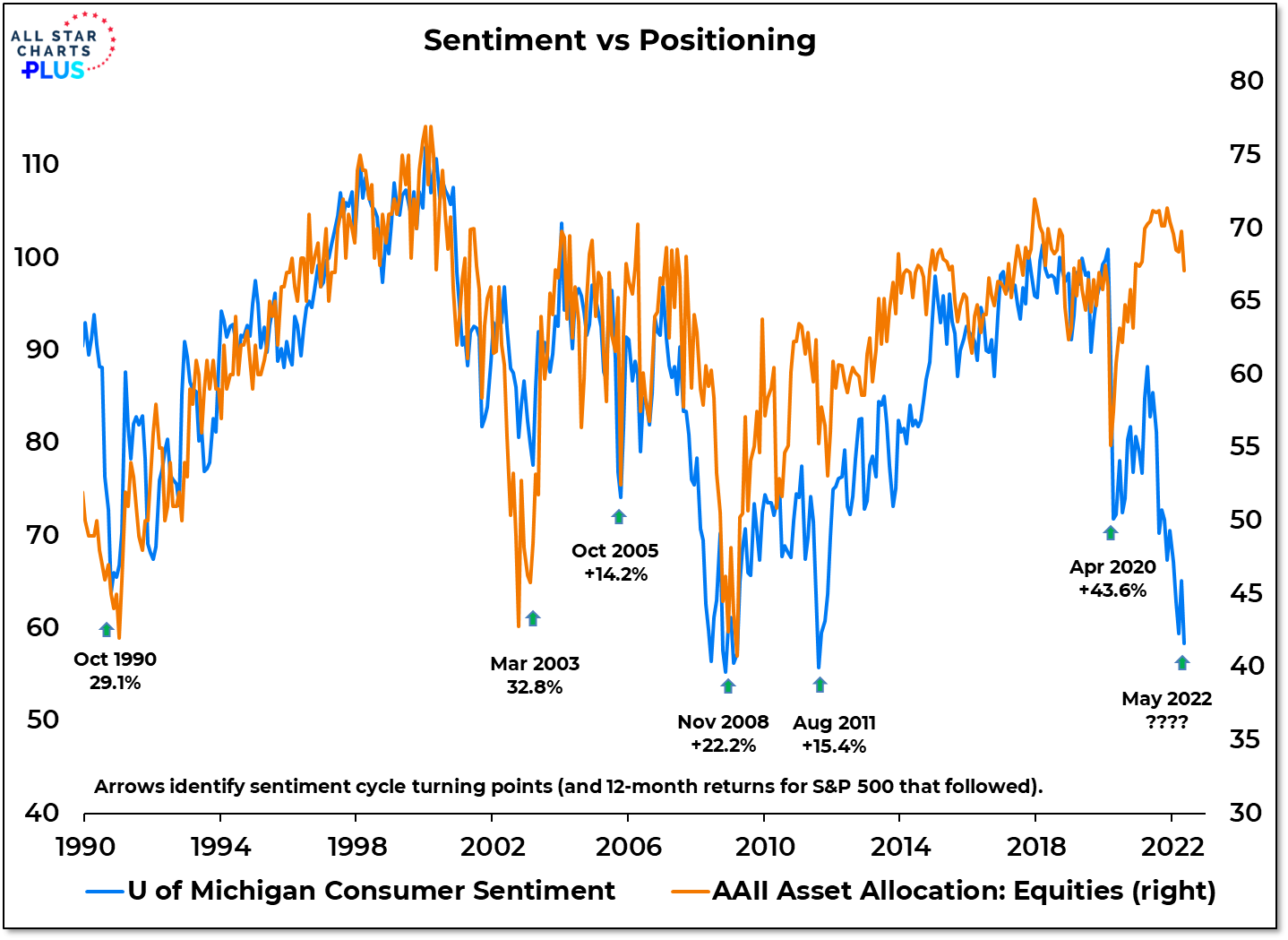

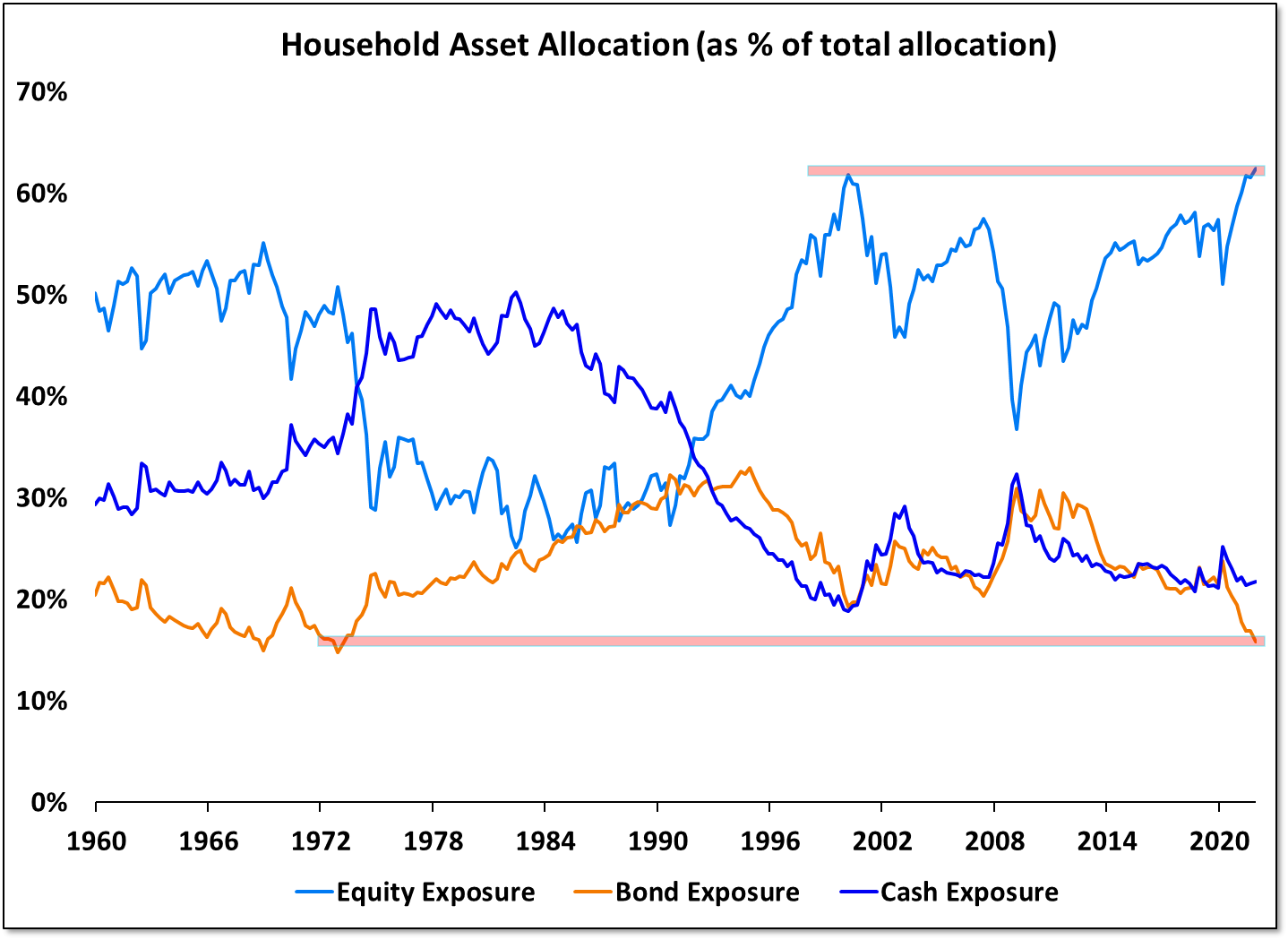

Sentiment Report Chart of the Week: Contrarian Positioning Is To Go Long Bonds

With all the focus on sentiment indicators, it seems like being a contrarian right now is all the rage. The problem with this approach is that while investors say they are pessimistic about stocks (and the economy), their positioning tells a different story. Household equity exposure was at an all-time high coming into 2021 and despite weakness in stocks this year, equity ETF’s have continued to see inflows. Even target date funds (a popular choice for passive investors) have been increasing equity exposure in recent years. It’s a different story for bonds. As dark as the mood has been on equities, it’s been even worse for fixed income and this sentiment is actually reflected in positioning. Coming into this year, household exposure to bonds was its lowest since the early 1970’s. With yields having risen to and now pulling back from well-tested resistance as concerns about economic deterioration rise, the contrarian call might not have anything to do with stocks. It might be to go long bonds.