This is the video recording of the May 20th Town Hall Meeting w/ Willie Delwiche

05/20/21 2PM ET [Read more…]

Expert technical analysis of financial markets by JC Parets

This is the video recording of the May 20th Town Hall Meeting w/ Willie Delwiche

05/20/21 2PM ET [Read more…]

From the desk of Willie Delwiche.

A box of family photos showed up at my house this weekend.

Some are relatively recent, others stretch back nearly a century. Together, they tell a story of generation after generation experiencing life in its many stages. Each one captures a moment

One that really stuck out to me was an image of a camping trip from more than 90 years ago. You can see an old car with a canvas tent pitched against it. At a picnic table, we see a lady and two young boys. The younger of these two is my grandfather. Next to him is his brother. Behind him is their mother (my great-grandmother).

“Now that’s camping done right,” I thought as I inspected the picture.

While the Fed is musing about tapering, the market, as usual, is already in action. Upward momentum in bond yields and an economy that has soaked up liquidity have become headwinds for equities at a time when investors are already re-thinking risk appetites.

The S&P 500 is a week and a half removed from its highest weekly close on record, but many of the areas of the market that saw the biggest run-ups over the past 2+ years are in the midst of tumultuous pullbacks. After gaudy returns on the way up, investors should expect equally gaudy reversals on the way down. By way of example, the ARK Innovation ETF is more than 30% off its peak but is still up 180% since Jan 2019. Bitcoin too is 30% from its high but is still up 1000% since Jan 2019. These moves make the action in small-cap growth (15% below where it was in Jan 2021 peak but still 70% above where it was in Jan 2019) staid by comparison.

From the desk of Willie Delwiche.

Key takeaway: Amid the economic optimism that is seen in surveys and magazine covers, the stock market is experiencing an unwinding in speculative excesses that has just begun. This shift in risk appetite makes a healthy sentiment reset like we saw in March a less likely outcome this time around. More probably is that we are moving from excessive optimism to some meaningful degree of pessimism. This is the area of the sentiment curve when price is most vulnerable to correction. With upside economic surprises waning and near-term breadth trends more mixed, the choppy environment of the past few weeks could not only persist, but even intensify.

Sentiment Report Chart of the Week: Magazine Covers

Like headlines, magazine covers can be more anecdote than an indicator. But they do give a sense of the public mood and the contrast between what appeared on the cover of The New Yorker in March 2020 (an empty Grand Central Station) and this week (New Yorkers emerging from the darkness and into the city bathed in blue skies and sunshine) could not be starker. As investors, we don’t want to overlook this shift from pessimism and despair to ebullient optimism.

From the desk of Willie Delwiche.

This morning I had the opportunity to catch up with my colleague Chuck Jaffe on the the Money Life Show.

This was a lot of fun as we briefly discussed the trends we continue to see play out in this very different 2021. Click here to give it a listen.

From the desk of Willie Delwiche.

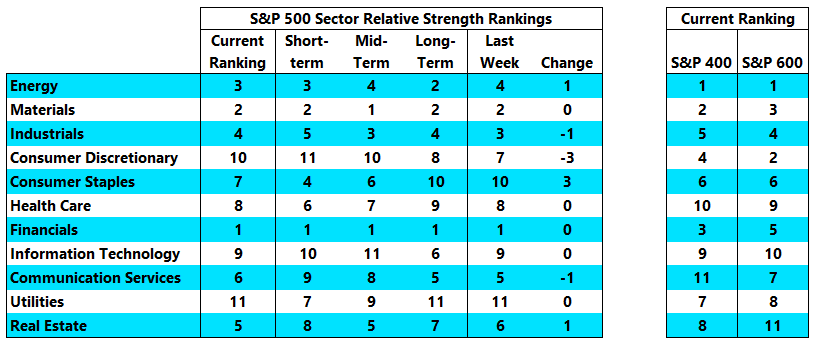

Key Takeaway: Investors finding themselves with too much Technology exposure. Speculative unwind occurring as neglected areas of the market make new highs. Inflation concerns are overdone in the near term but represent a new reality for the coming decade.

Cyclical value sectors remain atop the relative strength rankings, with Financials and Materials (both of which made new highs last week even as the S&P 500 overall lost ground) holding on to the top two spots. The big gainer in this week’s rankings is Consumer Staples, which climbed three spots in the relative strength rankings. Staples also finished the week at a new high. The industry group heat map shows improving conditions widespread among large-cap groups and deteriorating conditions widespread among small-cap groups. Actual leadership is pretty consistent across sizes and is consistent with the sector rankings.

From the desk of Willie Delwiche.

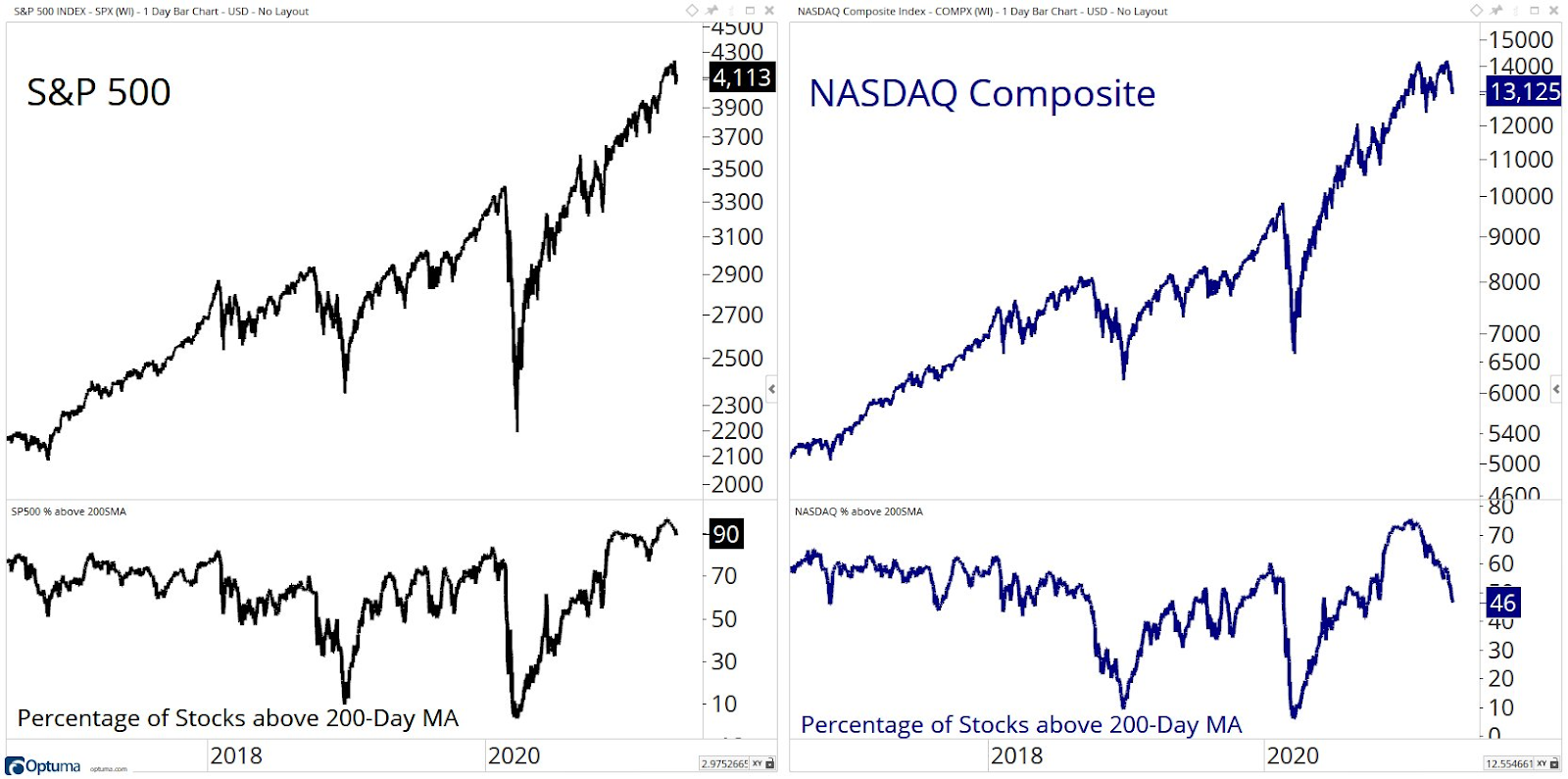

The one chart is actually two charts this week. On the left is the S&P 500 and the percentage of stocks in that index that are above their 200-day average (90%). On the right is the NASDAQ Composite and the percentage of stocks in that index that are above their 200-day average (50%). The contrast could hardly be more stark. Even as weakness has been seen in some of the largest sectors (like Technology), the S&P 500 is being supported by ongoing strength in cyclical values areas. The NASDAQ has little to no exposure to those sectors that are doing the best right now and is bearing the brunt of speculative excesses being unwound (the collapse in equity call options is evidence of this shift).

From the desk of Willie Delwiche.

I planted most of the vegetables for the garden over the past couple of weeks. Seeds and seedlings. Neat rows and clustered groups. Into the raised beds they went.

I don’t know what the day to day (or week to week) fluctuations in the weather will be. But I do know that it is (finally) Spring. Planting as the air temperature rises and our daylight hours expand increases the likelihood of a bountiful garden later this summer. Leafy greens (kale, arugula, chard) were the first into the soil. They can withstand cooler temperatures than the cucumbers, peppers and tomatoes.

As a gardener, I have some understanding of the underlying trends and conditions that guide the seasons. Plant too soon and a late frost will kill off tender seedlings. Plant too late and the summer heat will sap the strength of plants without well-developed root systems.

It’s about knowing the growing environment, managing temperature risks and finding opportunities to increase vegetable production.

Some might dismiss this as a farmer’s market timing. I call it prudent.