From the desk of Willie Delwiche.

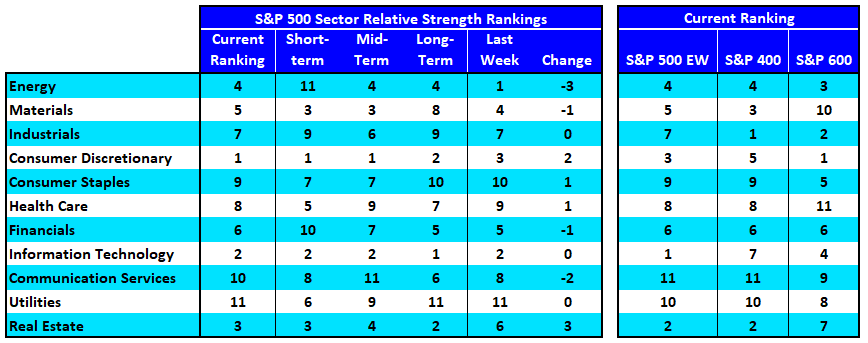

- Financials sector has continued to slip in our relative strength rankings, falling to its lowest level in over a year and dropping out of the leadership group.

- Consumer Staples remain toward the bottom of the overall rankings, but have been the top-ranked sector on a short-term basis and we are seeing evidence of improving trends at the industry group level across market capitalization levels.

- Large-cap health care is rising in the rankings, but this strength is not echoed at the mid-cap or small-cap level (or even on an equal-weight basis at the large-cap level)