From the desk of Willie Delwiche.

Expert technical analysis of financial markets by JC Parets

From the desk of Willie Delwiche.

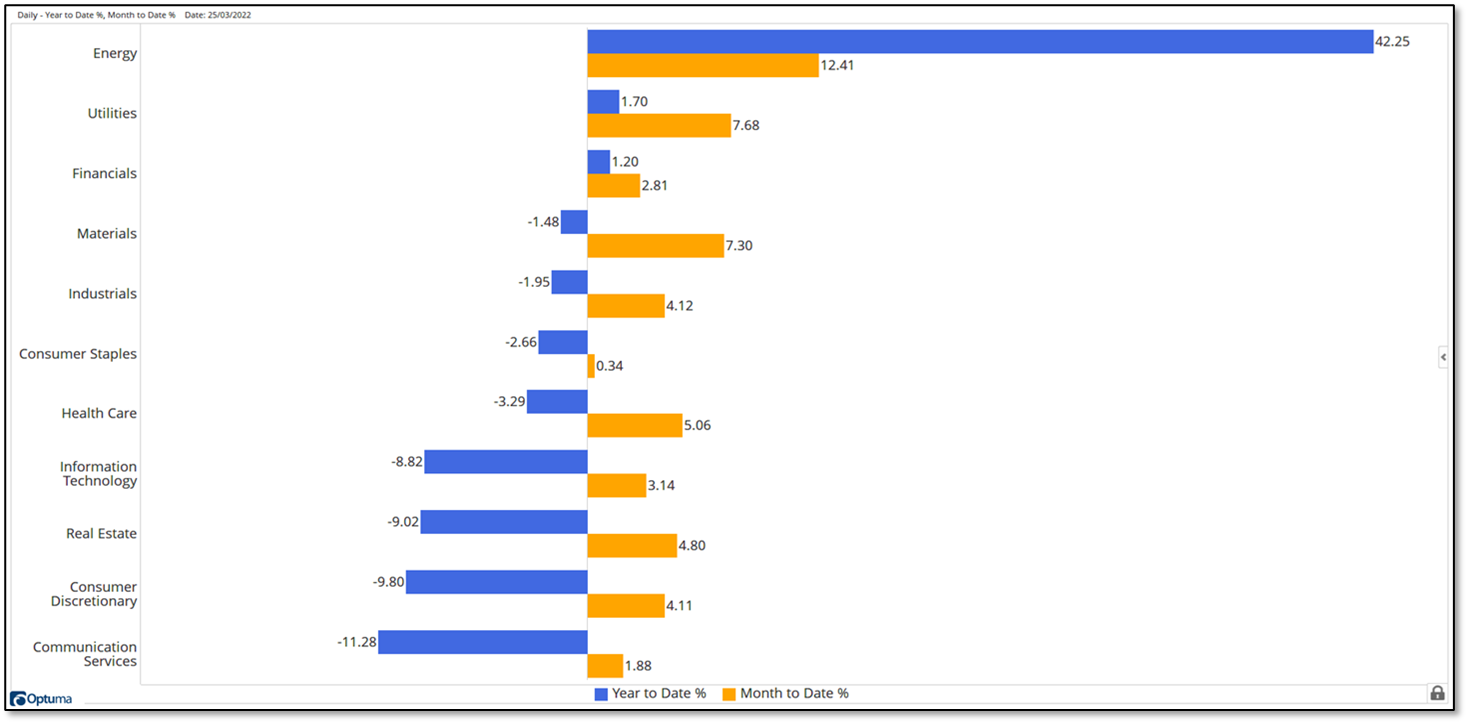

Key Takeaway: Q1 returns reflect a bifurcated market. Weekly data shows breadth struggling for traction. Inflation-fighting proposals are political palliatives, not economic solutions.

From the desk of Willie Delwiche.

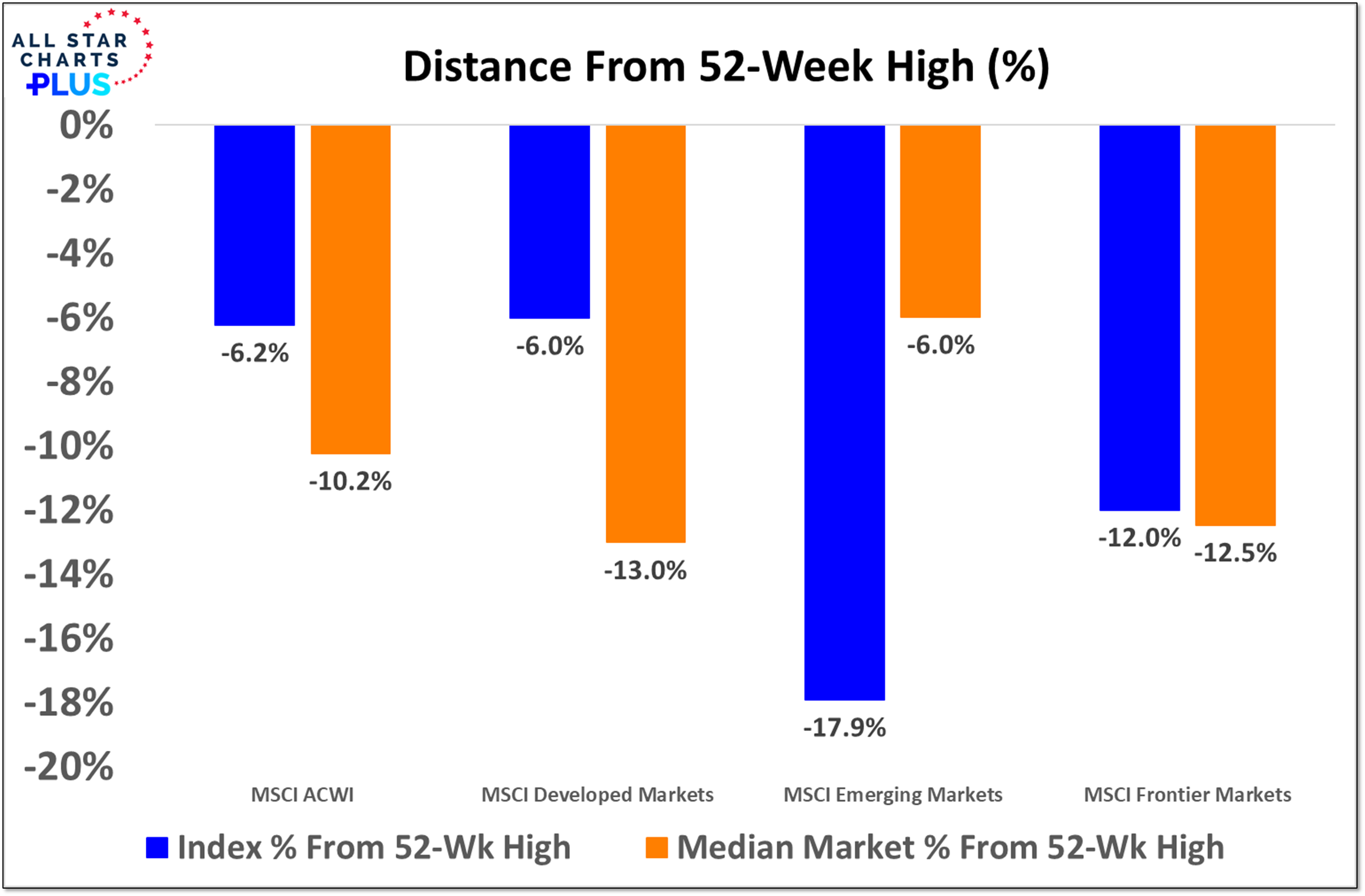

We discussed the need to look beneath the surface of the market in our Weekly Townhall and I mentioned it again on the Townhall Takeaway Livestream. This chart for the weekend hits that point one more time. When we look across the global market composites, Emerging Markets have experienced the largest drawdown from their 52-week high. When we look beneath the surface of the indexes, the median emerging market has had a smaller drawdown than the median Developed Market or the median Frontier Market. When we look at it from a country-level perspective, trends in Emerging Markets vs Developed Markets are stronger than they’ve been at any point in the past decade. That isn’t reflected in the indexes yet, but it may just be a matter of time until we see that transition. Speaking of transitions, while this chart is still looking at the distance below 52-week highs, we are starting to find ourselves thinking more about where things are relative to their 52-week lows.

From the desk of Willie Delwiche.

This year’s March Madness has been maddening indeed. Brackets were busted early and often. Three of the #1 seeds lost before they even had a chance to play for a trip to the Final Four. As challenging (and exciting) as that was, I’ve got a deeper frustration with it: It’s a passive participant’s paradise.

Let me explain.

Before the field of 64 is even set, we get deep dives on the various teams and their prospects. Stats are analyzed, stories are told. When the brackets are set, the picking begins. Though no games have yet been played, participants reason through potential matchups, from the first round all the way through to the finals. Bragging rights (and often more than that) are at stake for having properly allocated all your resources before the first whistle is blown. It’s about setting and forgetting. No feedback loops, no opportunities to adjust exposure based on changing tournament conditions.

This is the video recording of the March 31st Weekly Town Hall w/ Willie Delwiche & JC Parets

03/31/22 2:00 PM ET [Read more…]

From the desk of Willie Delwiche.

Key Takeaway: Price action has a way of changing sentiment, and the recent bout of strength has brought signs of hope. Optimism is on the rise with an uptick in bulls, a rebound in both the II and AAII bull-bear spreads, and an increase in exposure by active equity managers. Yet, bears linger and the drop in put/call ratios is driven by decreasing put activity. This speaks to less of a risk-off tone rather than a definitive sign of risk-on behavior. Though optimism is in the air, it’s going to take further improvements in trend, momentum, and breadth for bears to change their tune in support of a sustained rally.

Sentiment Report Chart of the Week: Breadth Backdrop Improving

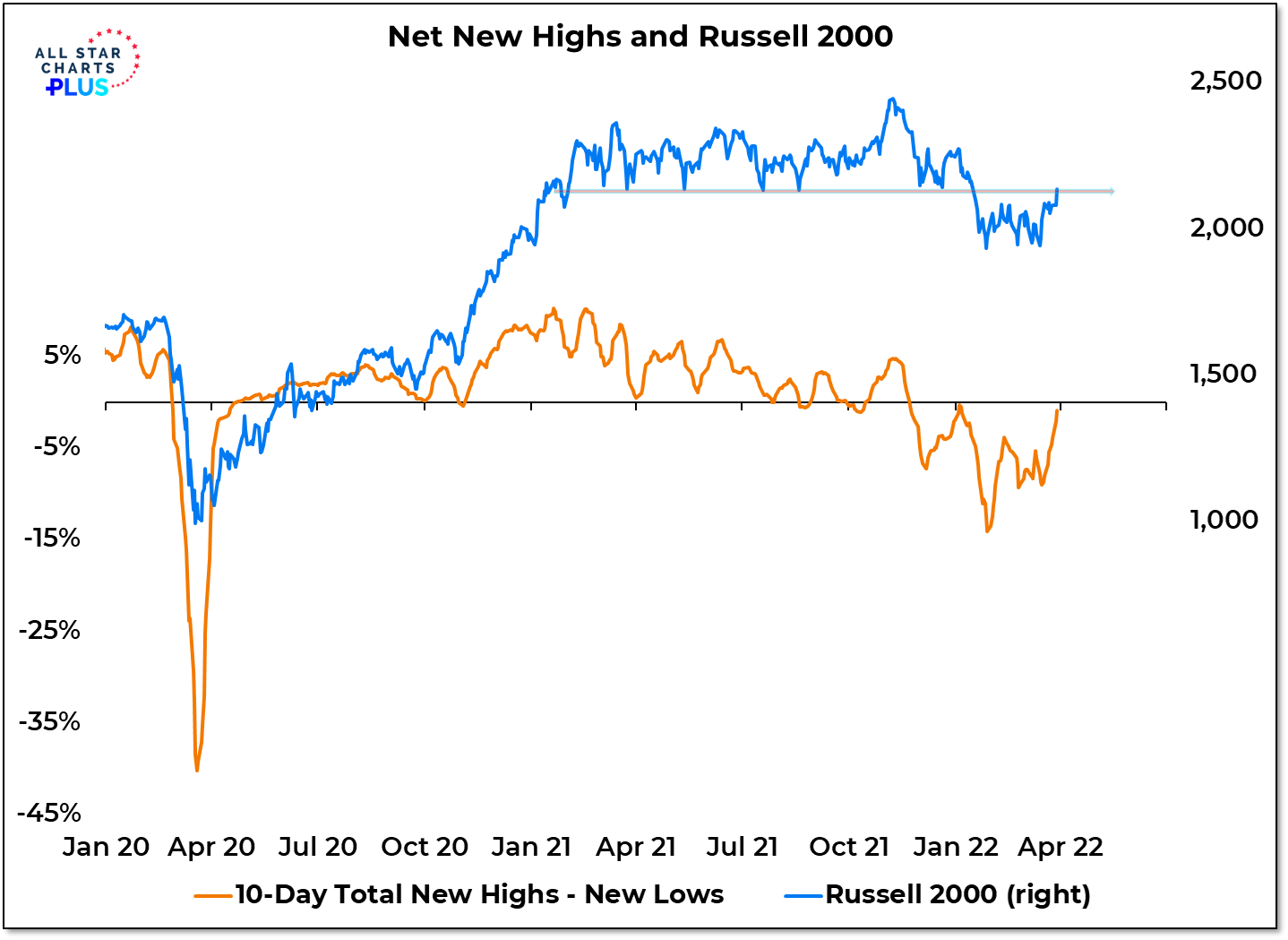

The rally off of the mid-March stock market lows has investors feeling better (or at least less bad). This improved mood (and the rebound in price that helped fuel it) will likely have more staying power if it’s accompanied by a better breadth backdrop. We are heading in that direction, but there is still work to be done. This week we finally had a day with more new highs than new lows (for the first time since the second trading session of the year). Building on that and getting the 10-day net new high number back in positive territory could help small-caps get back in gear. We’ve also had nearly 50% of S&P 500 stocks close at new 20-day highs. Getting above 55% would fire the first breadth thrust in our work since June 2020 and move the market into a bullish breadth thrust regime. The caveat: close but no cigar works in horseshoes and hand grenades but not breadth thrusts. A failure to build on recent strength could be met with disappointment from a price (and then sentiment) perspective.

Key Takeaways:

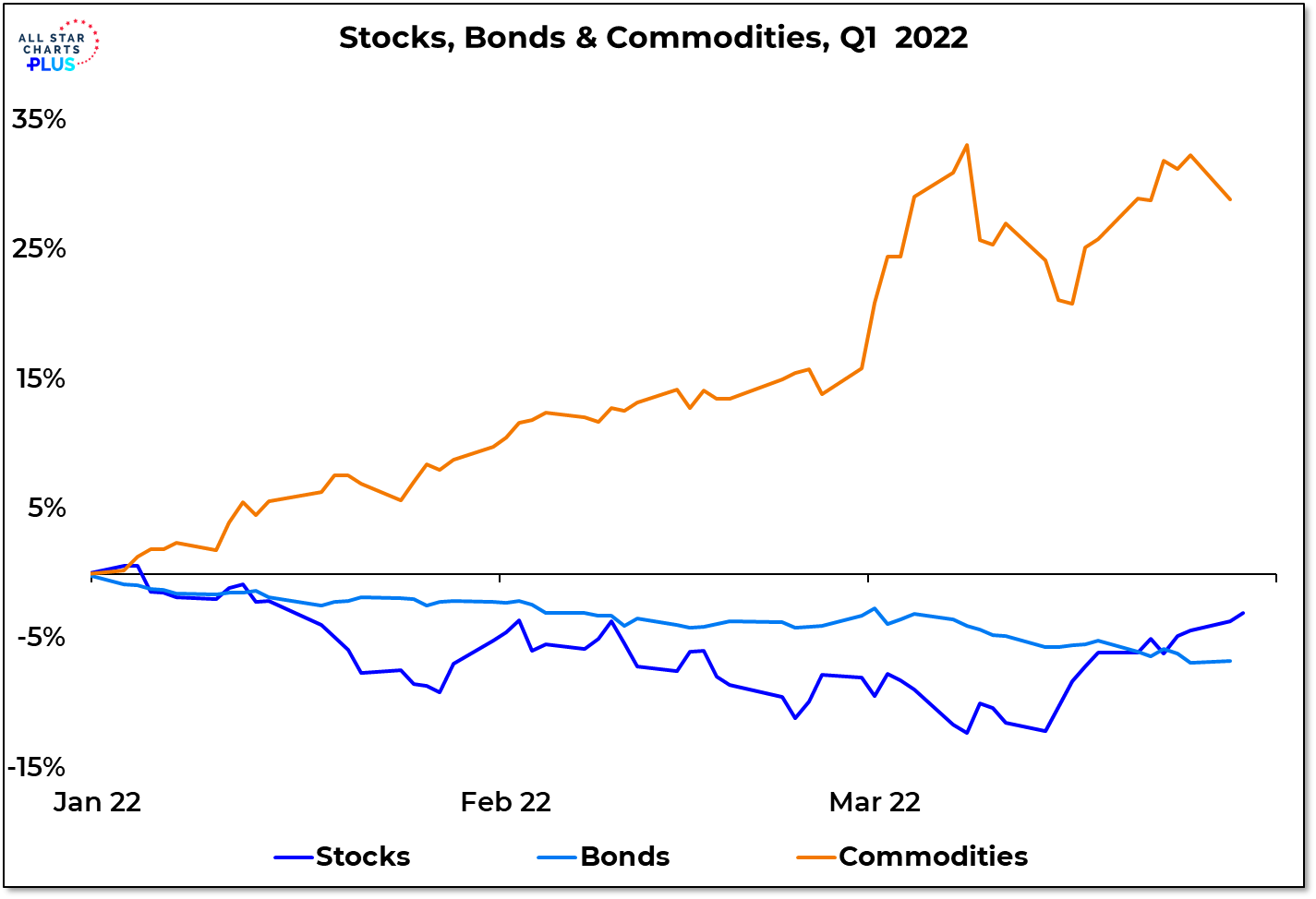

The first quarter still has two days of life left in it, though for many investors its end cannot come soon enough. The S&P 500 made a new high on the first day of the year, but has been underwater ever since. Bonds have been in the red all year, suffering their worst decline in decades. Commodities (and the minority of investors that have exposure there) enjoyed their best quarter in decades.

Each of these asset classes has its own story and dominant theme from Q1. For stocks, it’s the longest stretch of more new lows than new highs since the financial crisis. For bonds, it’s that yields around the world are moving to their highest levels in years (US & German yields get a lot of attention, but don’t overlook the Japanese 10-year yield breaking out after six years of moving sideways). For commodities, the story is about an asset class that has been overlooked by a generation of investors and financial planners making the case that it deserves to be part of the conversation. As investors we are well-served by allowing dynamic weighting to be part of the asset allocation process. Having all options on the table is an important first step before settling on specific exposures.

From the desk of Willie Delwiche.

{kind=link}