From the desk of Willie Delwiche.

Expert technical analysis of financial markets by JC Parets

From the desk of Willie Delwiche.

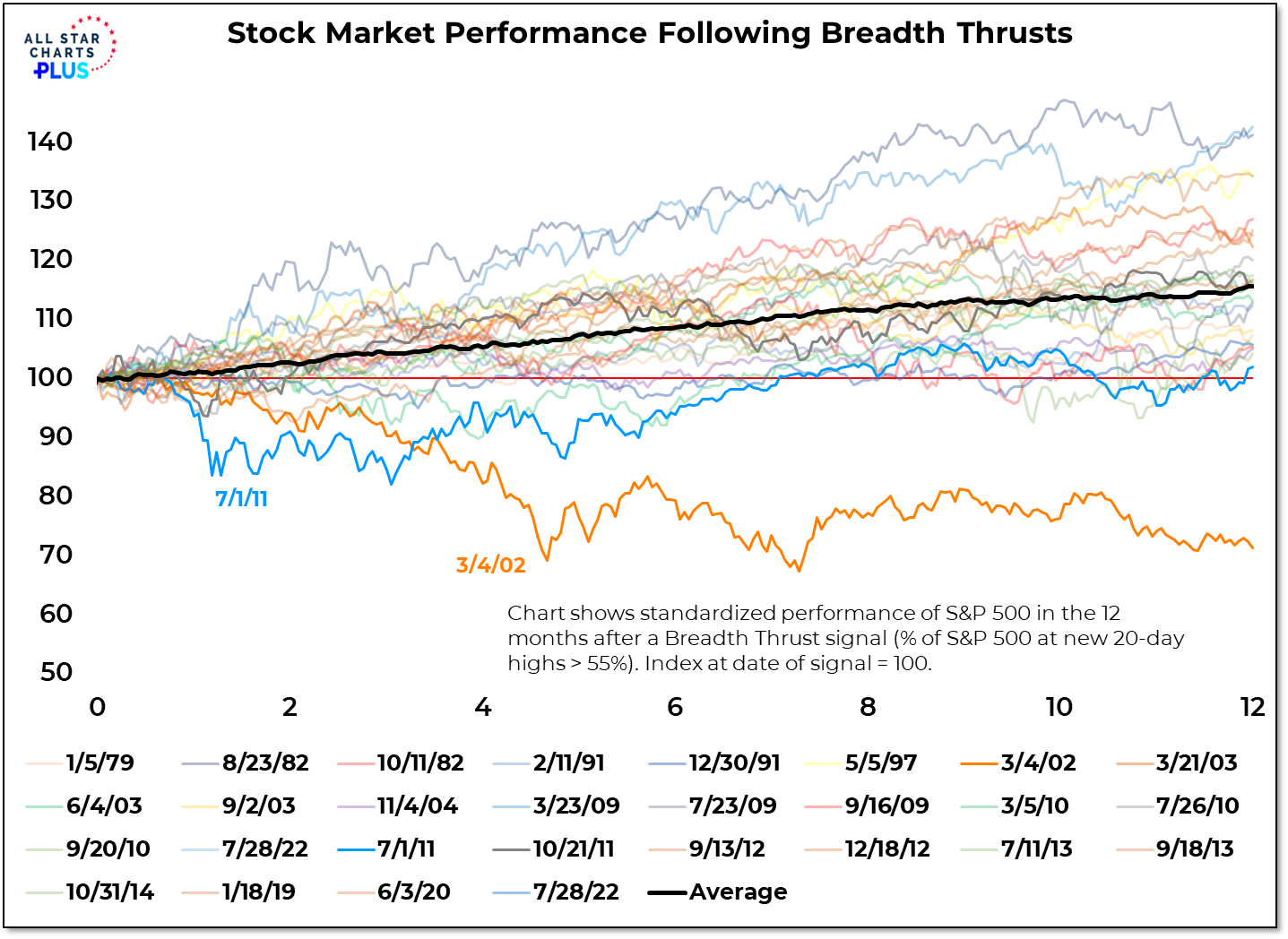

We got a breadth thrust this week as the percentage of S&P 500 stocks making new 20-day highs edged above 55% on Thursday. This might not be the most well-known of the various breadth thrusts, but it’s the one I lean on most heavily. It’s part of our bull market re-birth checklist and watched by market pros. It’s not an all clear signal or a guarantee that the market will not go down. The market stumbled after the July 2011 signal and the performance in the wake of the March 2002 signal was ugly. But overall, this tended to point to improving conditions and indicate that the market may more easily move up and to the right. I have reservations right now (we continue to see more new lows than new highs) and I believe much of the rally off the June lows has been built on a premise that will prove false. But the data are what they are. To quote Walter Deemer, “Ours is not to reason why, ours is just to sell and buy.” Breadth thrusts signal strength and I don’t like to argue with strength.

This is the video recording of the July 28, 2022, Weekly Town Hall w/ Willie Delwiche.

07/28/22 2:00 PM ET [Read more…]

From the desk of Willie Delwiche.

It’s not the first thing I do in the morning (a cup of coffee and some devotional time take precedence) but early each day, I am out in the garden. Hose in hand, I water what needs to be watered. I’m also observing – noticing weeds, identifying what needs to be propped up or redirected, and making a mental note of what is ripe and ready to be picked.

Right now, it’s cucumbers – a lot of them. I’m giving them away as fast as I can. But I still had to pickle a bunch this past weekend (Capital Preservation in investing parlance). They are almost hydra-like this time of year. Eat one and there are three more ready to be picked.

From the desk of Willie Delwiche.

Key Takeaway: In recent weeks, the bulls have made their presence known after hiding in the shadows for most of the year. But as they inch their way forward, they will need assurance from the market that they’re moving in the right direction. So far, any signs of positive feedback have been lacking. New lows remain greater than new highs (for 35 weeks and counting). And there is an absence of strength among global markets, although they have stopped going down. The market needs to turn it up in regards to price and participation if the bulls are to prove more than a bunch of wallflowers.

Sentiment Report Chart of the Week: How Do We Keep The Bulls On Dance Floor?

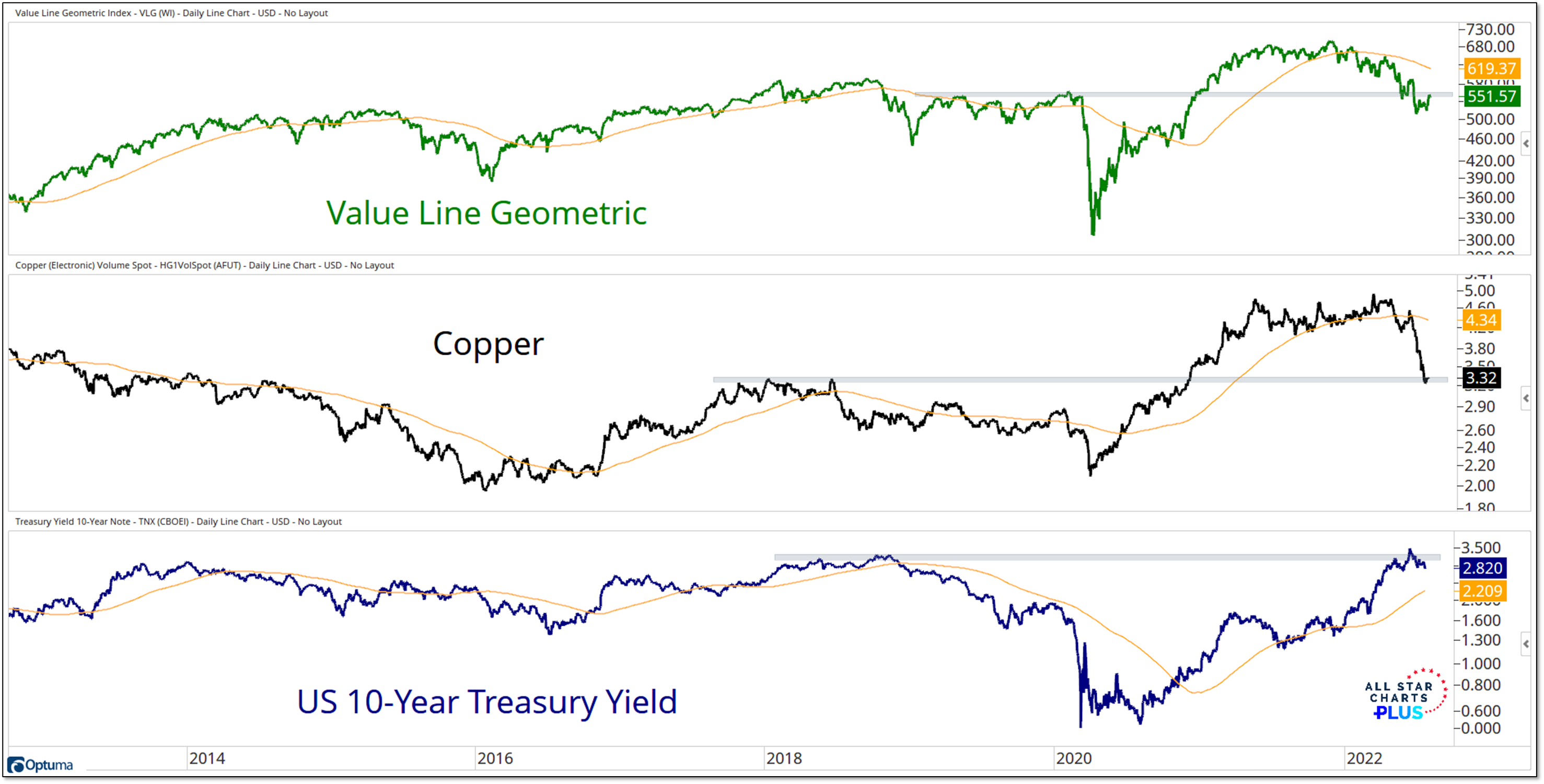

If we are going to have a party, we need to keep bulls on the dance floor. One way to do that is through improved price action. We know that it takes bulls to have a bull market, but it also takes a bull market to keep the bulls involved. When we look across various assets, we keep coming back to key levels from 2018. The Value Line Geometric Index is struggling to get back above its pre-COVID highs, copper is finding support at its 2018 highs and Treasury yields briefly poked above their 2018 highs before reversing lower. Not sure whether it will be above or below, but I expect all three of these to end up on the same side of those key thresholds. If it’s above, equity bulls are being rewarded and they are likely to keep dancing. If it’s below, then it’s back to enduring taunts from bears and wondering why they bothered showing up in the first place.

It’s been over a month since the S&P 500 made a new year-to-date low and market volatility has cooled somewhat. After averaging a 1% move (in either direction) every other day in the first half of the year, the S&P 500 has only had 5 such moves so far in July (16 trading days). The last one was over a week ago.

A couple 9-to-1 up volume days on the NYSE and an uptick in bulls on the sentiment surveys is providing some hope that the bear market environment may be fading. Our Risk Indicators (as well as the continued presence of more stocks making new lows than new highs) argue that it is premature to jump to that conclusion.

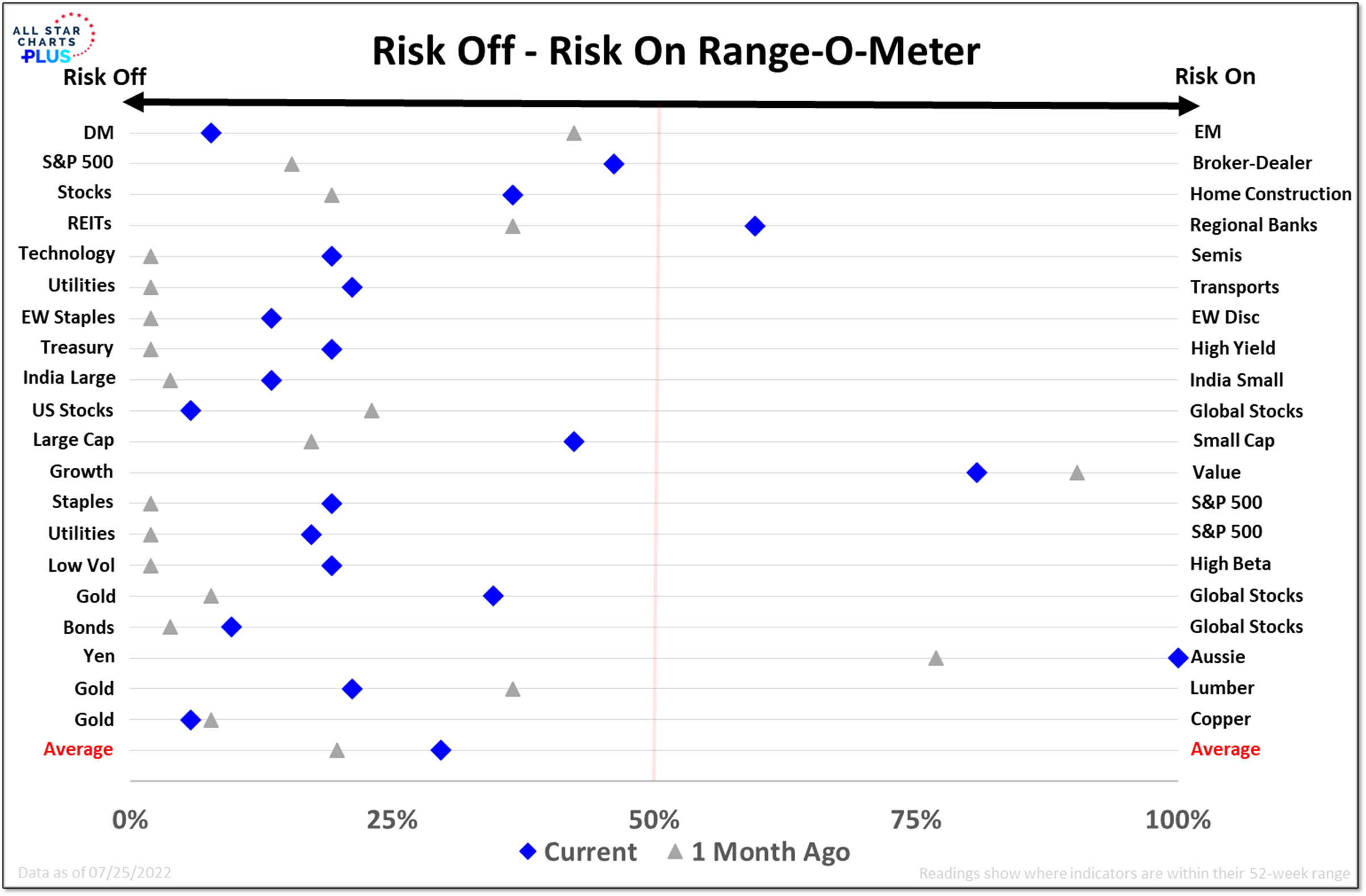

We have seen some improvement over the past month, and of the 20 risk off – risk on asset pairs, 14 are closer to their risk-on extreme than they were a month ago. But even with that improvement, only 3 of the pairs are closer to the risk-extreme than the risk-off extreme. In this fight over field position team “Risk Off” is winning. As we get into the details, this story is more about a lack of risk appetite and risk on weakness rather than broad strength out of risk off components.

Key Takeaway:

While high relative to the previous decade, the Fed could in 2019 at least make the argument that inflation and wage growth were low from a historical perspective. Additionally there was evidence that financial stresses were starting to build. Now, the wage and price pressures that were still incubating in 2019 have erupted to their highest levels in decades while at the same time the financial stress has never been lower (according to the St. Louis Fed’s index).

The market has currently priced in another 100 basis points of tightening over the final three FOMC meetings this year (September, November, December). There is some expectation that Powell will use his post-FOMC press conference this week to tamp down those expectations. The Fed may want to preserve as much flexibility as possible to adapt to incoming information, which many hope will show decelerating inflation and which many fear will show outright contraction in growth. That remains to be seen. But with inflation pressure more related to labor market imbalances than supply chain disruptions, a sustained move lower in inflation is unlikely without considerable easing in labor market conditions.

The Fed may not want a recession, but in this environment it will likely tolerate one. A dovish pivot at this point is unlikely.

From the desk of Willie Delwiche.

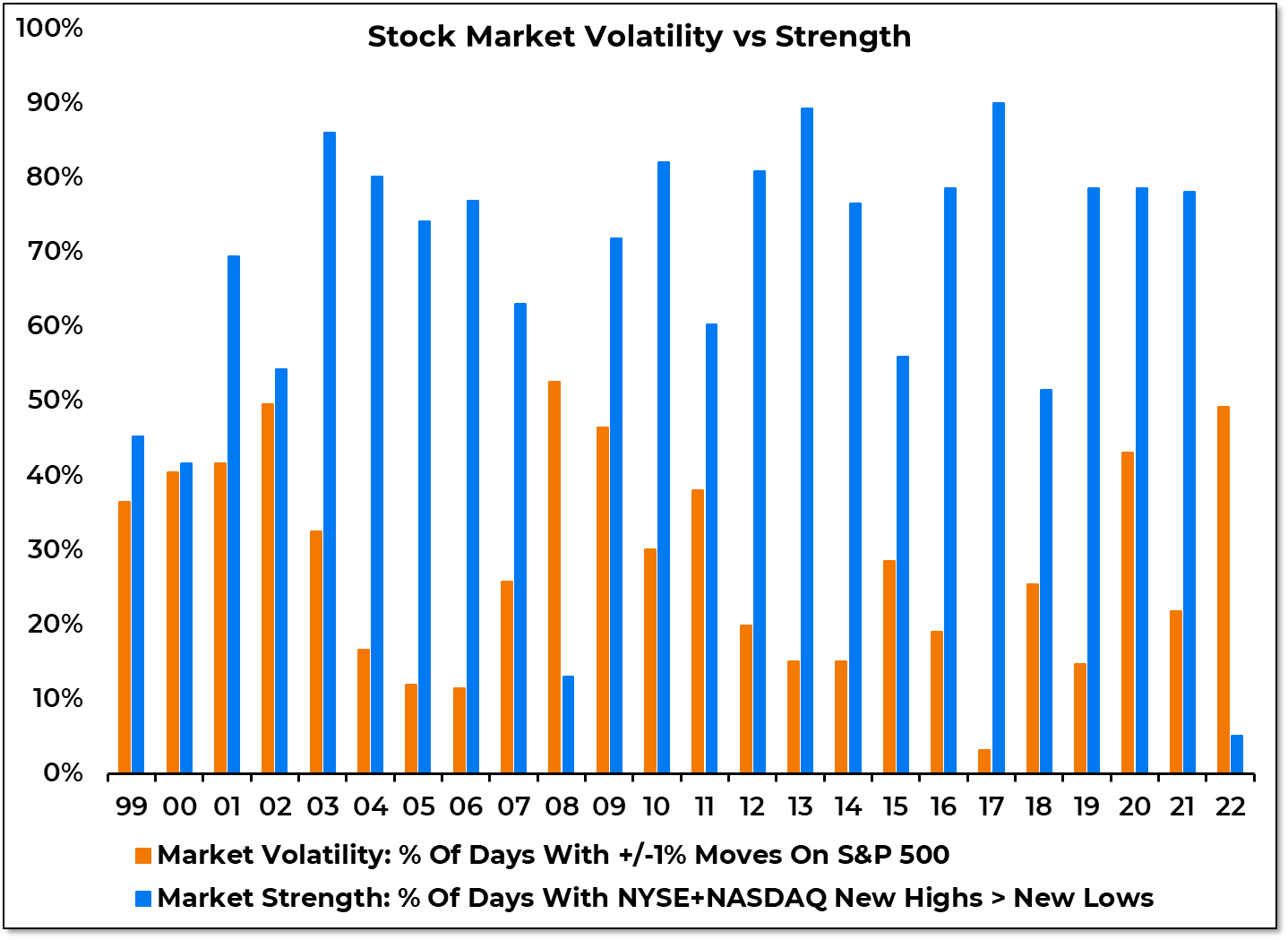

Stocks have rallied off of their mid-June lows, but it goes without saying that 2022 has still been a year marked by volatility and an absence of strength. In fact it has been historic (or nearly so) on both accounts. In terms of volatility, only two years (2008 and 2002) finished with a higher percentage of days on which the S&P 500 closed up or down by 1% or more than we have seen so far in 2022 (just shy of 50%). No year has come close to as low a percentage of days with more new highs than new lows. So far we have had seven in 2022: two in January, three in March and one each in April and May. That is just 5% of the trading days so far this year. The next closest year was 2008, which had new highs > new lows on just 13% of the days. At the opposite extreme is 2017, regarded by many as one of the best years in stock market history. That year, 90% of the days saw more stocks making new highs than new lows, only 3% of the days had the S&P 500 moving by more than 1%, and the S&P 500 booked a nearly 20% gain.