This is the video recording of the September 30th Weekly Town Hall w/ Willie Delwiche & JC Parets

09/30/21 2PM ET [Read more…]

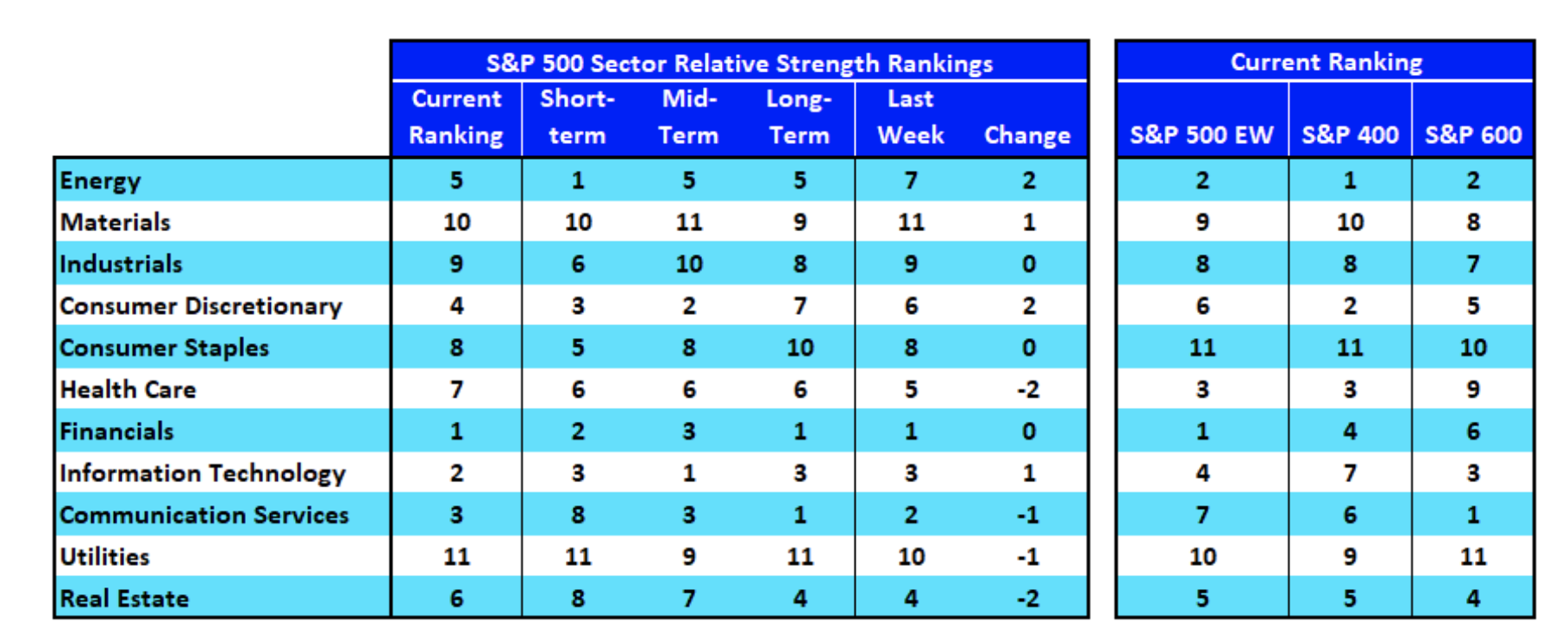

Expert technical analysis of financial markets by JC Parets

This is the video recording of the September 30th Weekly Town Hall w/ Willie Delwiche & JC Parets

09/30/21 2PM ET [Read more…]

From the desk of Willie Delwiche.

We see what we are thinking about. The first time I really became aware of this was a few years ago after we bought our Subaru. I had gone from not thinking at all about Subarus to driving one and now I was surprised to see how many other Subarus were on the road. I realized quickly that I was not an automotive trend-setter, but just being impacted by the way our brains work.

It happened again recently, though this time with a more exciting car.

I flew into Reagan National airport in Washington, DC, on a recent trip to visit family in Maryland.

I met up with my sister when I arrived and headed over to the rental car counter. I had reserved a four-door mid-sized model but what I got instead was a two-door sports car. A convertible Ford Mustang, to be exact. To be clear, they didn’t force the car on me. The agent asked if it would be okay and I quickly agreed.

From the desk of Willie Delwiche.

Key Takeaway: Bulls continue to retreat while bears remain relatively unchanged. The current imbalance in sentiment speaks to cooling optimism and an increasing degree of caution. In recent weeks bears have been on the rise, but so far that has been a short term event. It does not mean that all has been repaired from a sentiment perspective. On the contrary, risks remain elevated. If history is any lesson, the fear and pessimism associated with a complete unwind in optimism will not materialize without instigation from downside volatility. It’s often falling prices that lead the way and fan the flames.

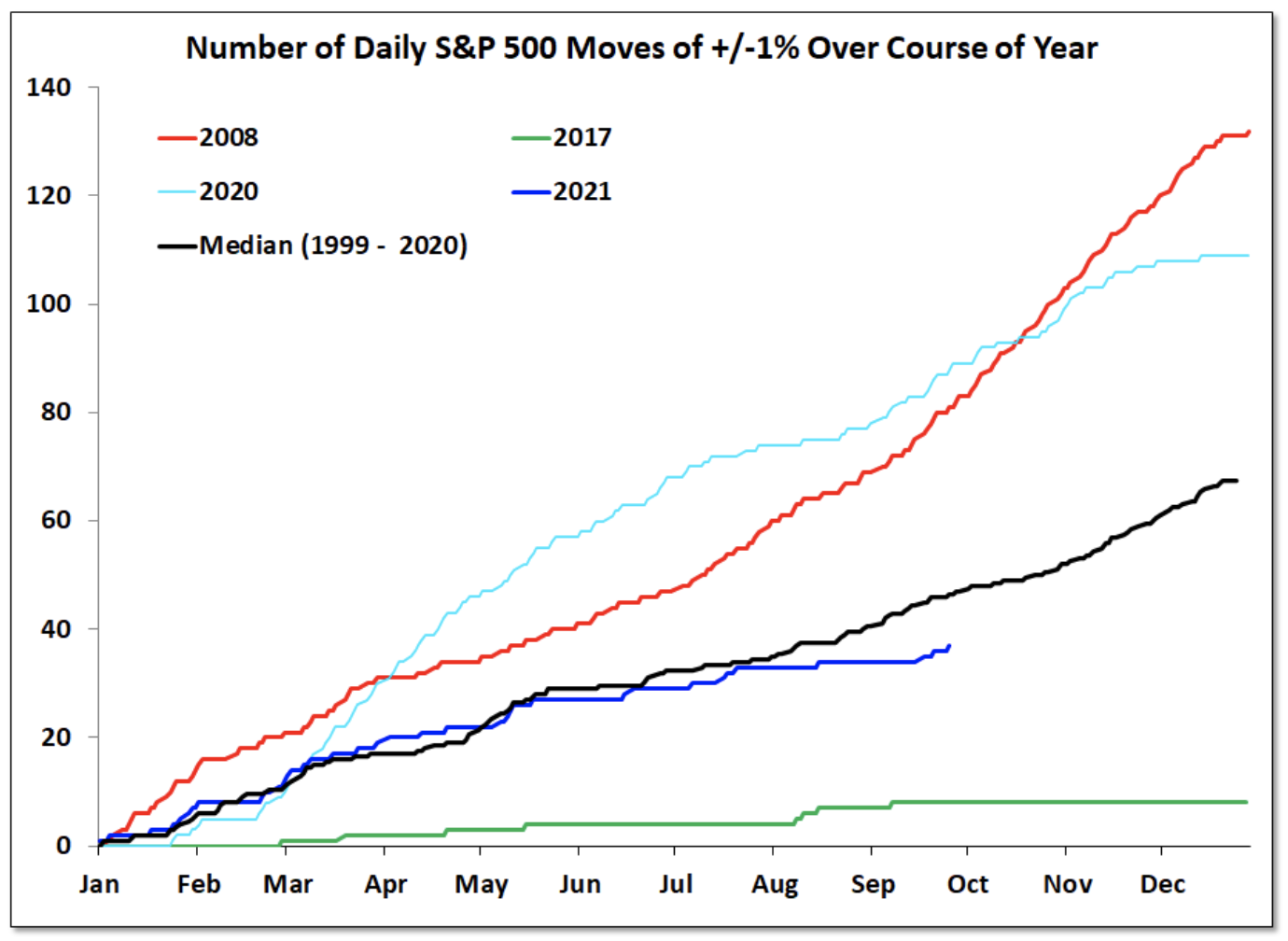

Sentiment Report Chart of the Week: Lack of volatility keeps investors calm

Volatility has picked up over the last few weeks, but it is not leading to much in terms of increased fear and pessimism on the part of investors. Why? Because even with the latest uptick, the number of 1% moves this year is not only well-shy of what was seen last year, but has actually slipped away from the trend of the past two decades. It may take more volatility to bring out fear and concern that last more than just a session or two. Whether or not that is forthcoming remains to be seen.

Key Takeaways:

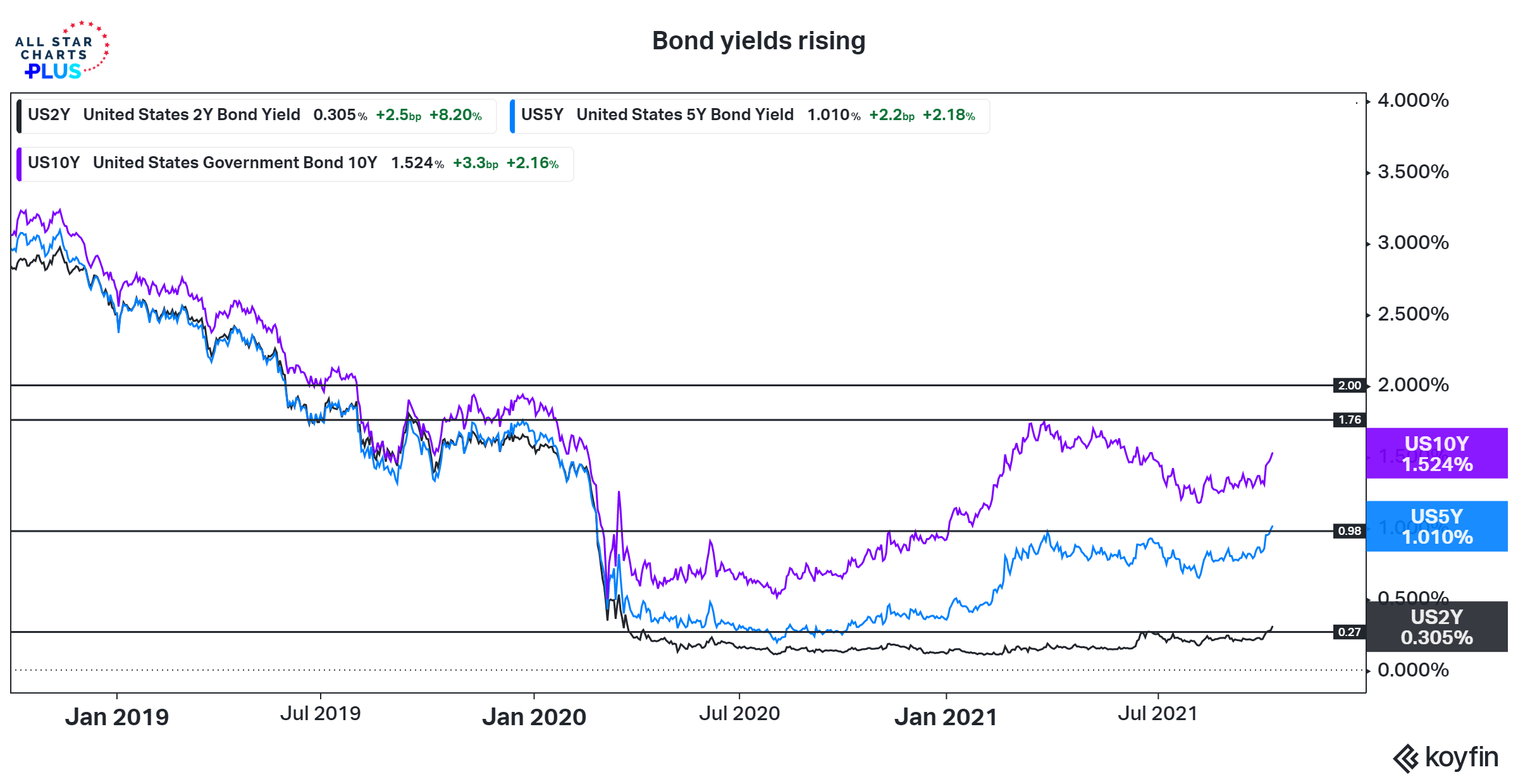

Make no mistake about it, bond yields are rising. Yields on 2-year and 5-year T-Notes have surpassed their 2021 highs and are at levels not seen since their Q1 2020 COVID-related breakdown. The yield on the benchmark 10-year T-Note is above 1.50% and appears headed toward a test of the early 2021 high near 1.75% sooner rather than later.

How high yields could rise in Q4 remains an open question. A two-handle by the end of the year does not seem far-fetched. As recently as 2019, 2’s, 5’s and 10’s all had yields above 2%. With inflation pressures showing little evidence of meaningfully subsiding the path of least resistance for bond yields appears higher.

As we get ready for the final quarter of the year, we need to remember that while guesses are great, we don’t want to get ahead of what is actually happening. Evidence > Assumptions.

From the desk of Willie Delwiche.

From the desk of Willie Delwiche.

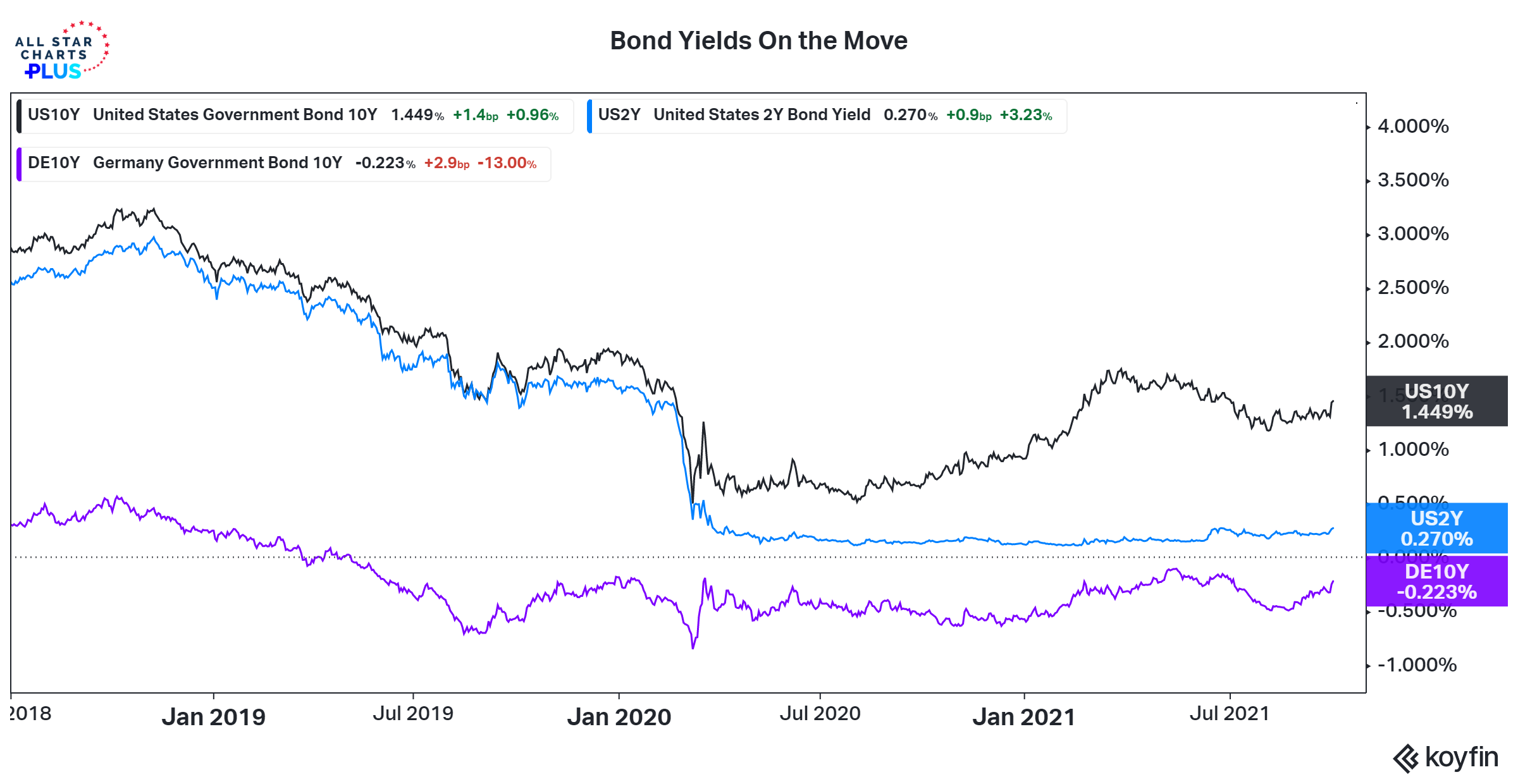

The story this week was bond yields and the mounting evidence that they are ready to move higher. 10-year yields in the US and Germany have climbed to their highest levels since July. The US 10-year T-Note yield has broken above 1.40% and could soon have 1.75% again in its sights. A 2-handle by the end of the year would not be surprising. Except for the May/June time period, German yields are the least negative they have been since crossing the zero threshold in mid-2019. These moves may reflect inflation expectations, but with the rise in the 2-year T-Note yield this week (highest level since March 2020) it is also the bond market taking seriously the possibility that the Fed will soon be joining the 30% of global central banks that have already begun to raise interest rates. For investors, this could be an opportunity to rotate back into cyclical sectors that do well in rising rate environments.

This is the video recording of the September 23rd Weekly Town Hall w/ Willie Delwiche.

09/23/21 2PM ET [Read more…]

From the desk of Willie Delwiche.

I’ll admit it. I’m a Fed-watcher from way back. I enjoy it as much as anyone, and probably more than most (especially those within the All Star Charts community).

While I never had to analyze the weekly money supply numbers to figure out what the Fed was doing, I’ve remained attentive as the Fed has revamped its mode of communication with the market time and again.

The latest iteration — a written statement and press conference after every FOMC meeting coupled with summary economic projections released four times a year — reflects the Fed’s desire for transparency. It also supports the belief that forward guidance is a powerful tool at a time when interest rates are stuck near zero.

Market participants listen, absorb the message and the forecasts, and react. We did this dance again this week.

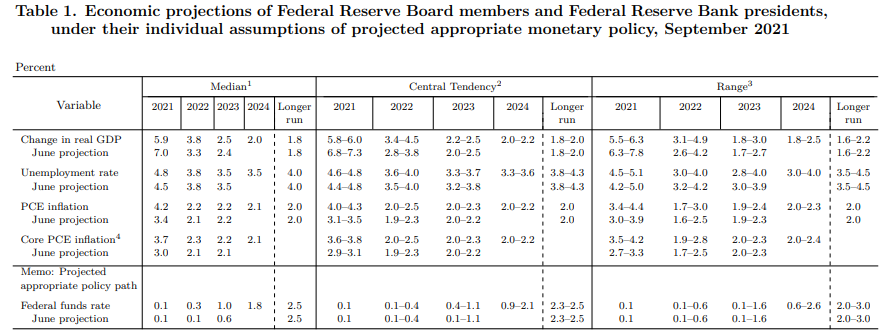

Here’s the latest batch of forecasts from the Fed: