From the desk of Willie Delwiche.

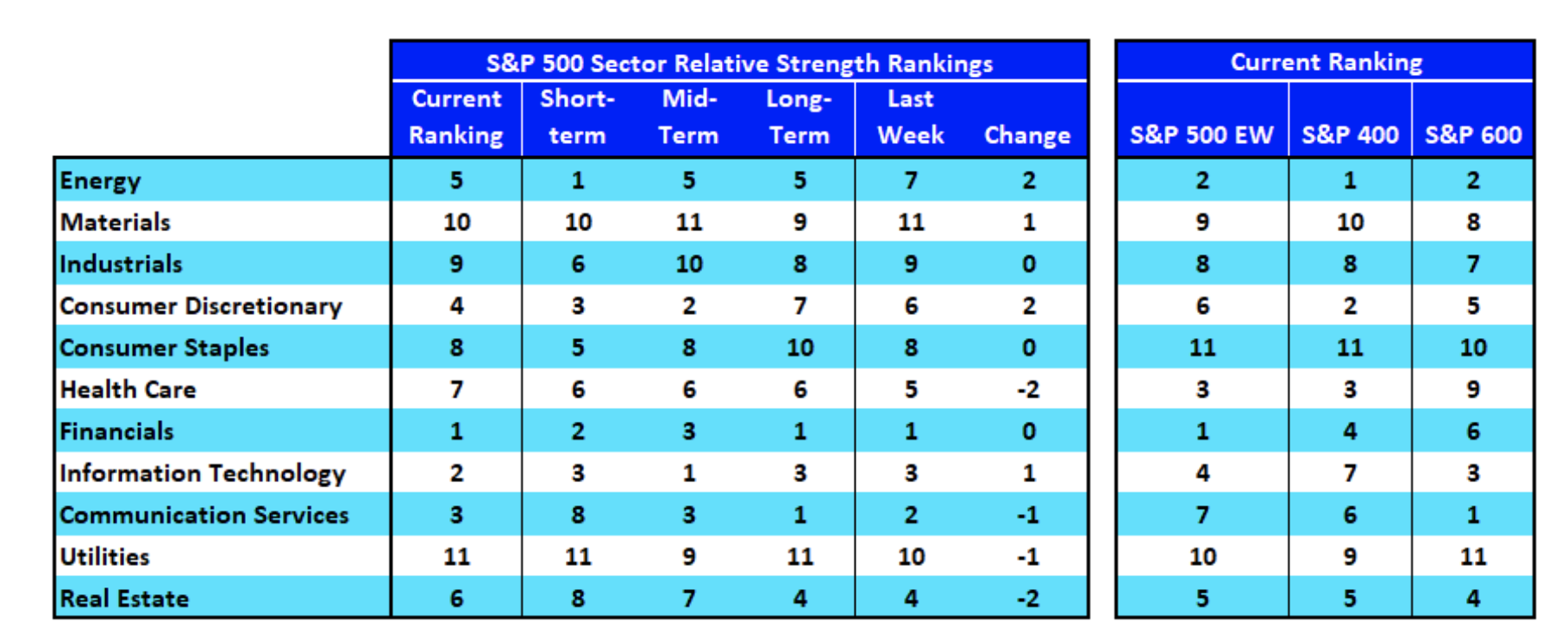

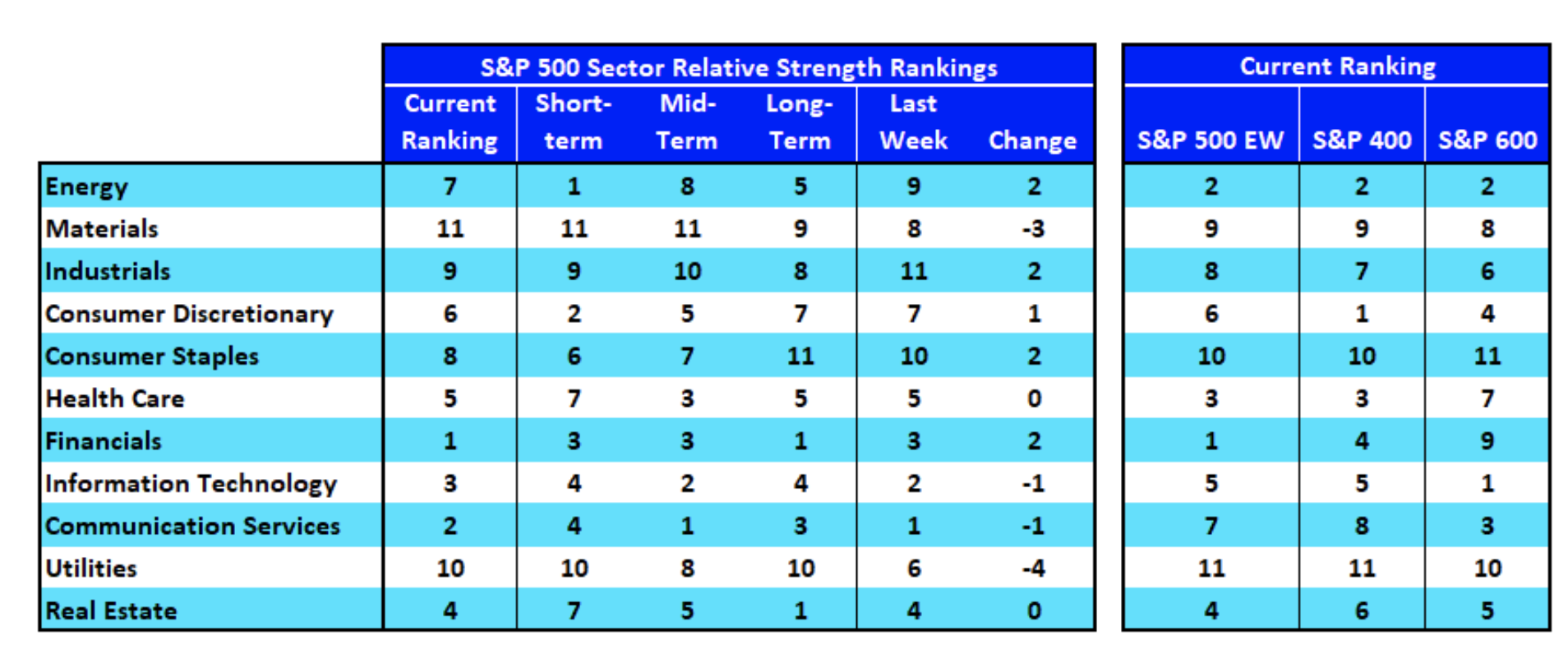

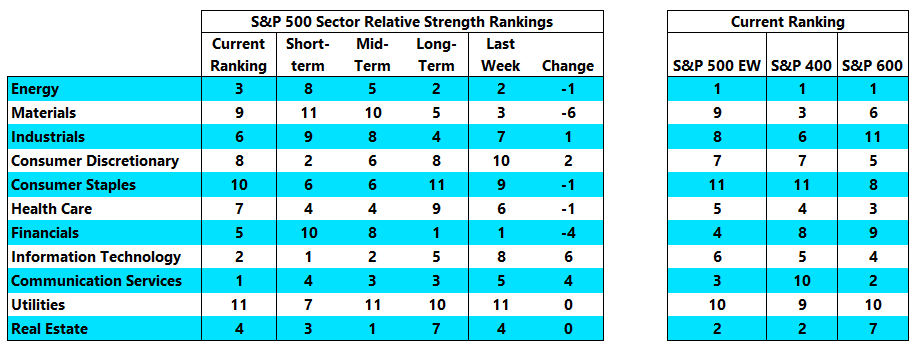

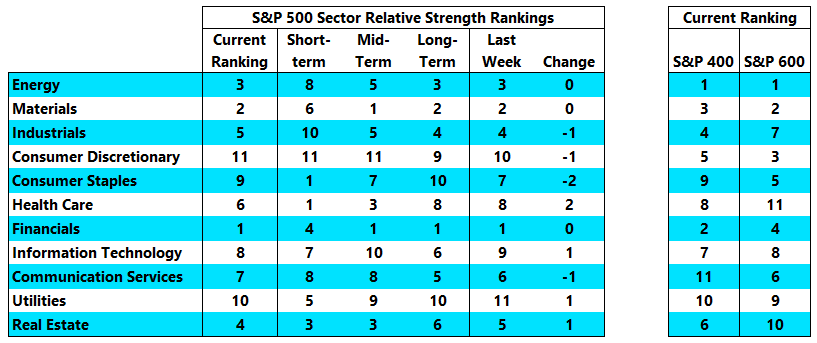

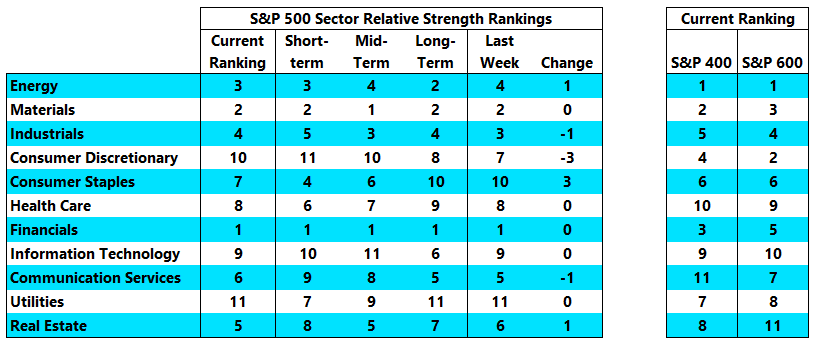

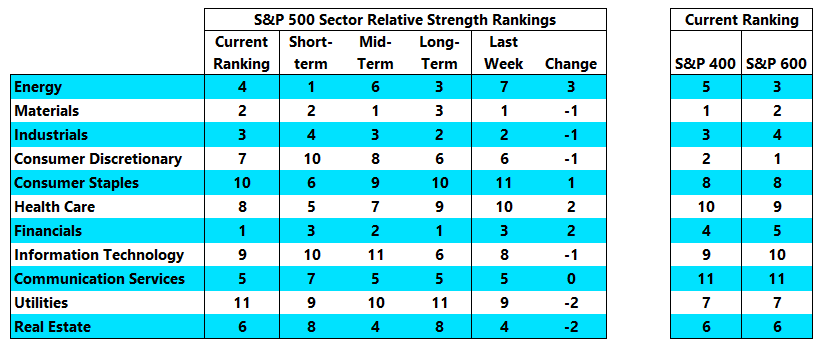

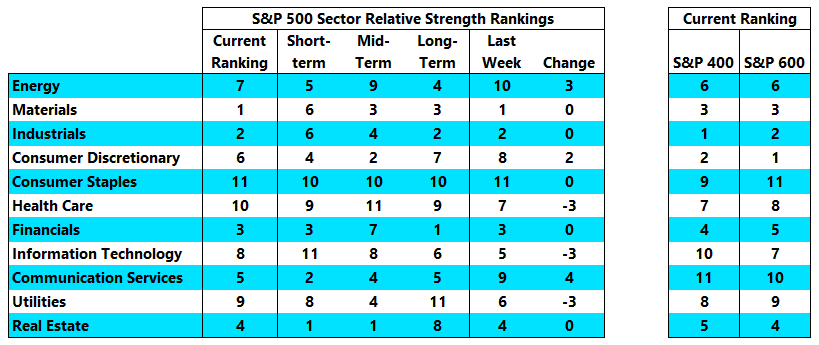

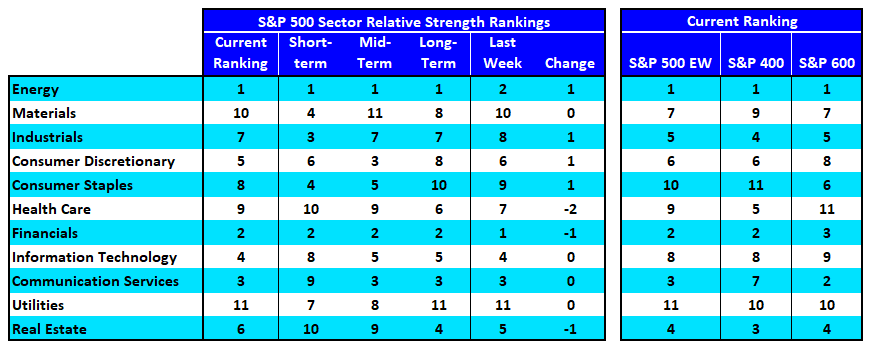

- Energy and Financials switched spots this week but remain at the top of the relative strength rankings, with leadership evident across time frames and market cap levels. Over the past three months, no other sector is up more than 1%. The Financials sector is up 6% and Energy is up 8%.

- Our industry group heat map shows notable strength in Energy and Banks. Health Care, Technology and Telecom groups are coming under pressure.