This is the video recording of the October 27th, 2022, Weekly Town Hall w/ Willie Delwiche.

10/27/22 2:00 PM ET [Read more…]

Expert technical analysis of financial markets by JC Parets

This is the video recording of the October 27th, 2022, Weekly Town Hall w/ Willie Delwiche.

10/27/22 2:00 PM ET [Read more…]

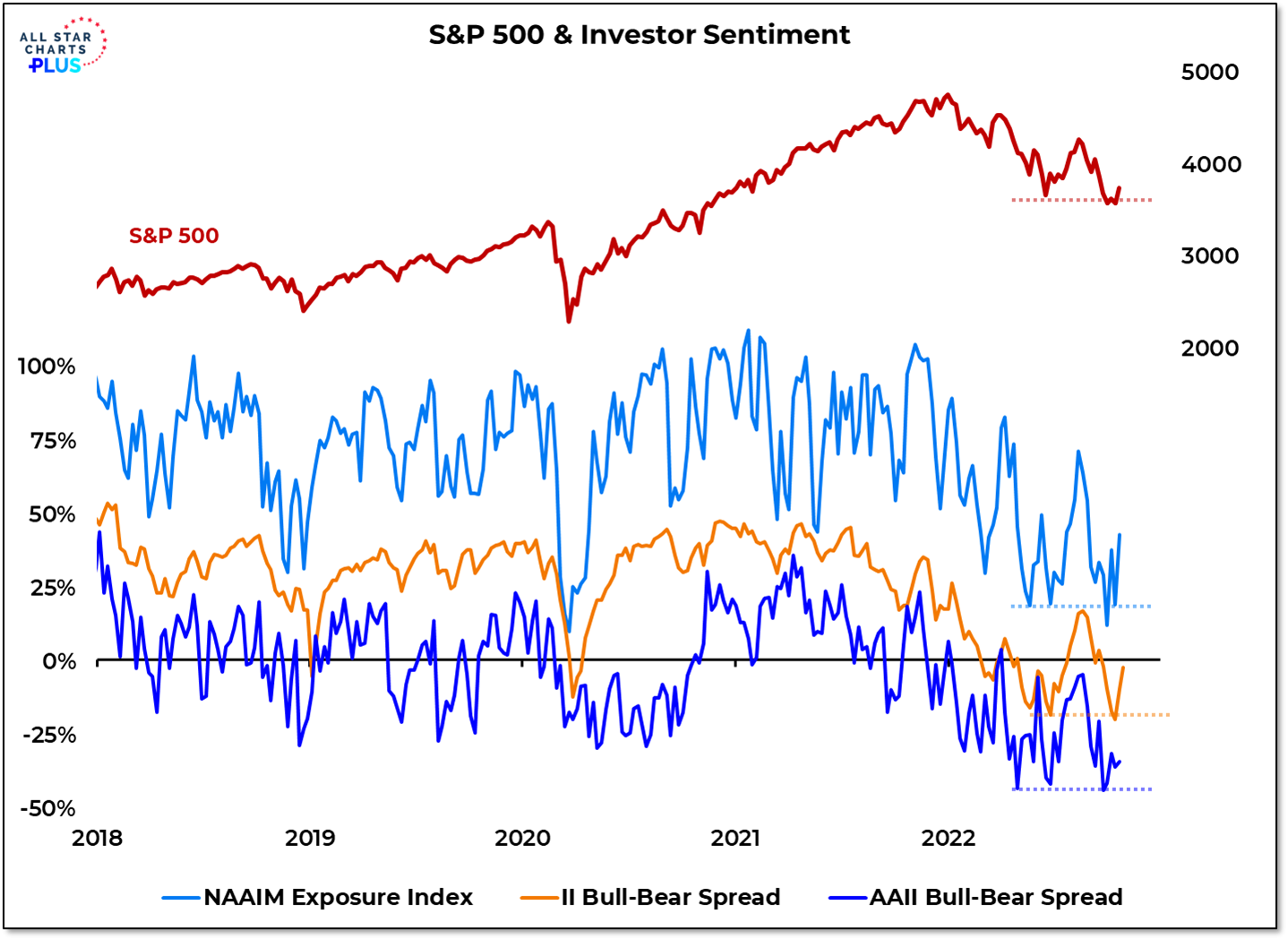

From the desk of Willie Delwiche.

“This Is A Test. This Is Only A Test.”

The S&P 500 this month and last undercut its June low but it is now back above that key level. The same can be said from a sentiment perspective. The NAAIM Exposure index and the Bull-Bear spreads for Investors Intelligence and AAII in recent weeks dipped below their Q2 lows but have since recovered.

Why It Matters: Important lows often get re-visited one last time before trends turn and rallies become sustainable. It will be a lot easier for stocks to build on recent strength if optimism is increasing. It does indeed take bulls to have a bull market. Confirmation that this was just a test is twofold: staying above the Q2 lows and continued improvement beneath the surface (including seeing more stocks make new highs than new lows).

In this week’s Sentiment Report we take a closer look at how investors are feeling and how (if at all) we can take advantage of it.

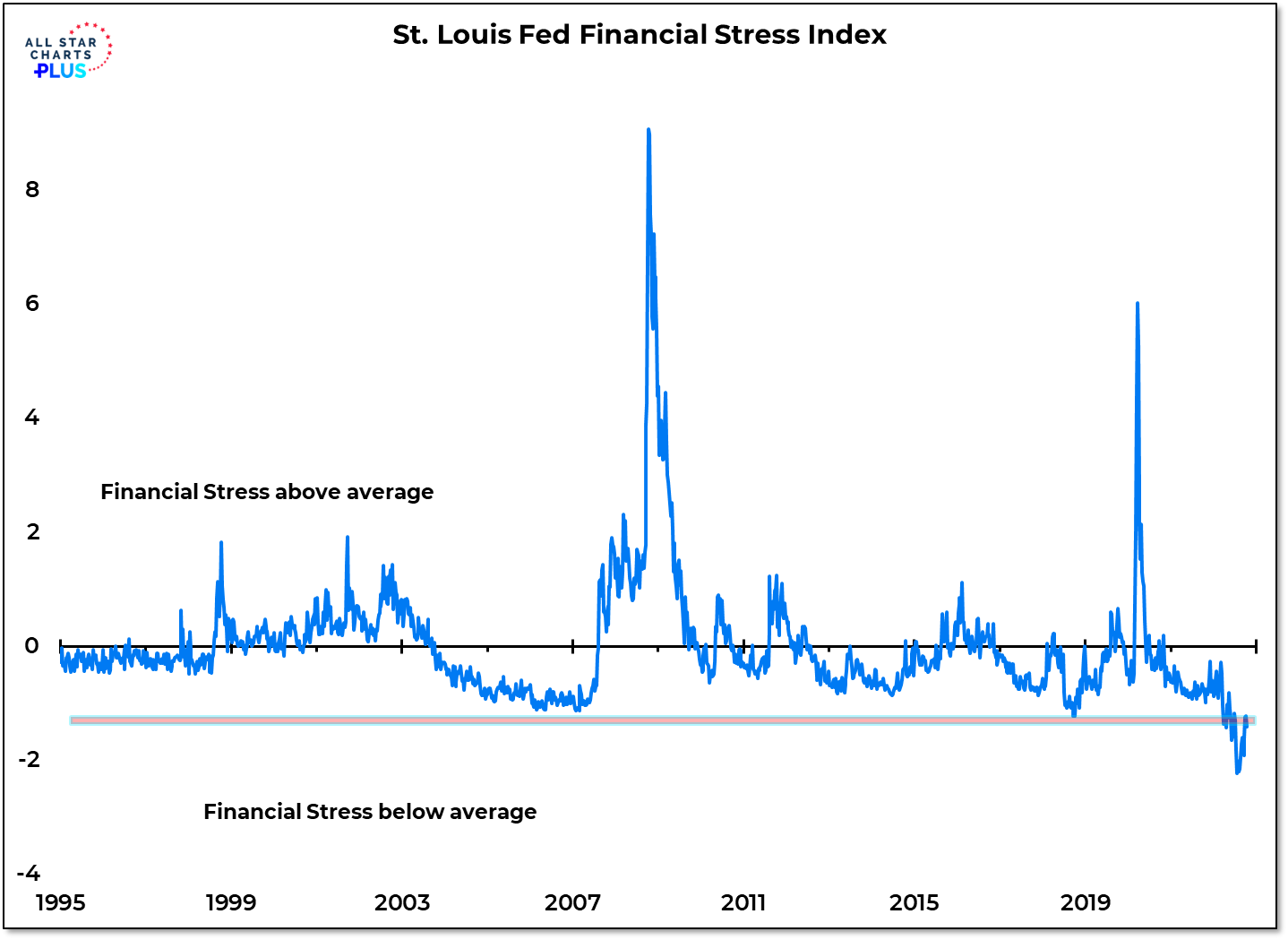

Stocks and bonds are enduring one of their worst years on record. Yet the St. Louis Fed’s Financial Stress Index dropped to never before seen levels. It’s off its lows but still indicates less stress in the financial system than at any previous point in the past quarter century.

Why It Matters: Aggressive tightening by central banks around the world has pushed sovereign yields higher and kept interest rate spreads subdued. That has made financial stress less apparent. Until this changes, there is little impetus for the Fed to pivot away from its intense focus on bringing down inflation.

In taking a Deeper Look we see how the specific characteristics of this cycle may be masking signs of stress that are present just beyond the headlines.

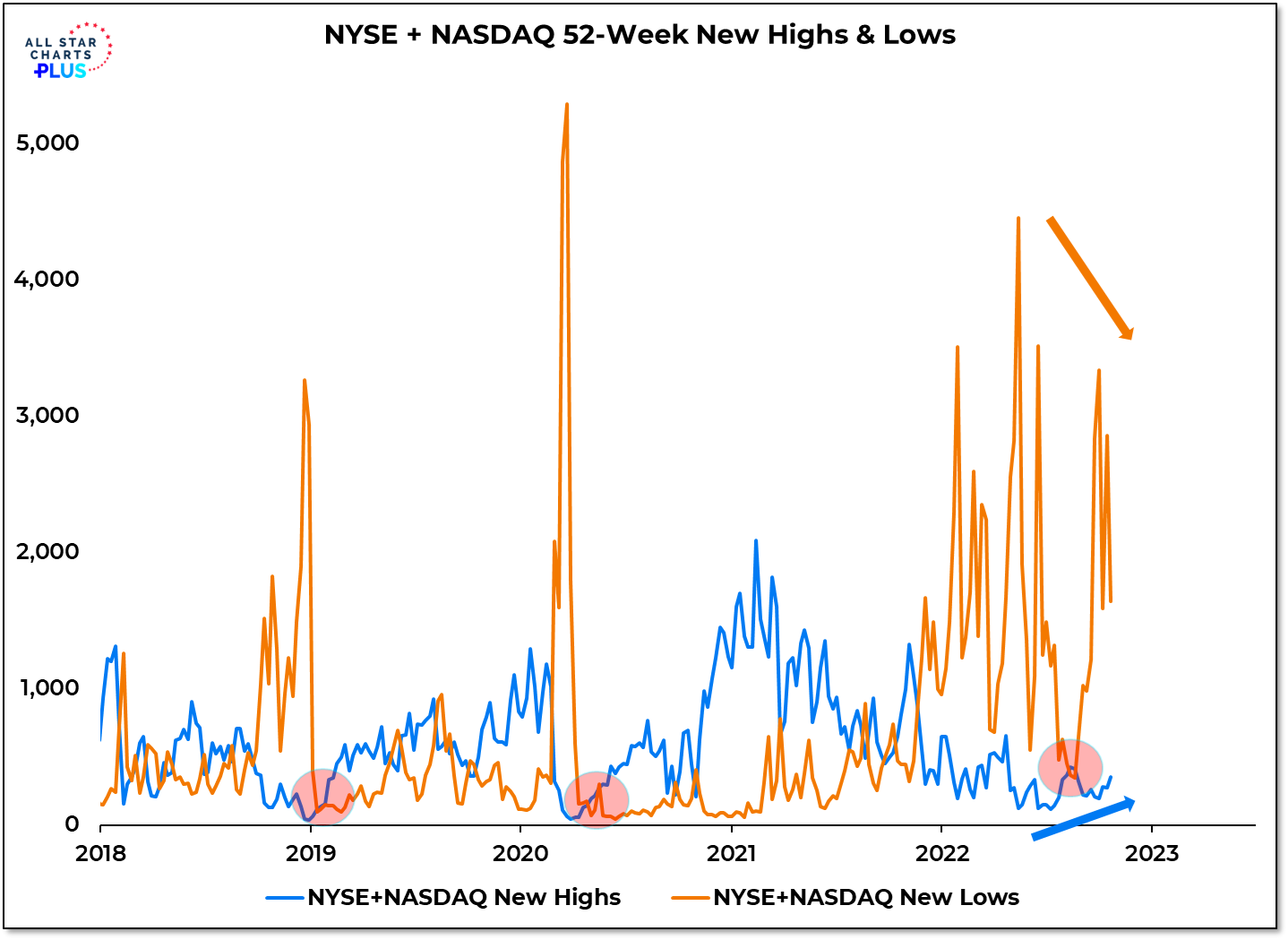

Reversal – Or Just a Respite?

The new low list peaked in May and the new high list bottomed in July. Despite this, we’ve had more new lows than new highs in 44 of the past 46 weeks.

The Details: More than 4400 stocks (48% of the total on the NYSE + NASDAQ) made new lows in May. That was the most since March 2020. The new low list has ebbed and flowed since then but has not surpassed that peak. The 116 stocks (just 1% of NYSE + NASDAQ total) that made new highs in the first week of July was the fewest since April 2020. Last week 357 stocks (4%) made new highs and 1645 (18%) made new lows.

More Context: When downtrends ready to turn higher and new bull markets are being born, we usually see a sharp collapse in new lows accompanied by a gradual expansion in new highs. The combined effect is that new highs begin to consistently outnumber new lows. We saw this in early 2019 and again after the COVID lows. There were two weeks in August in which the new high list was longer than the new low list, but that turned out to be more respite than reversal.

We take a Deeper Look at other areas where we have seen more respite than reversal and what that means for adding risk ahead of the November elections.

From the Desk of Willie Delwiche.

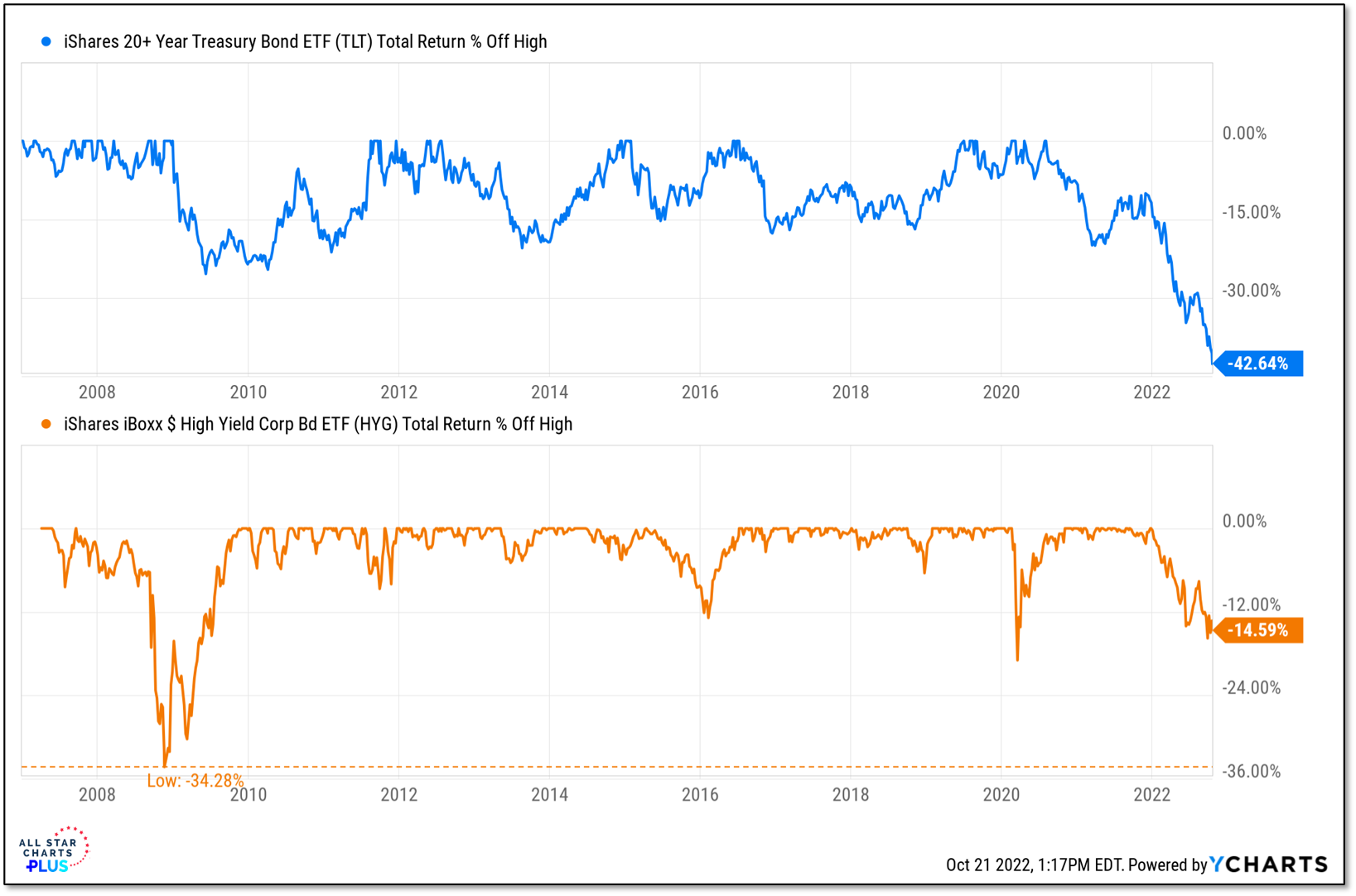

2022 Sovereign Stress > 2008 Corporate Stress

The Chart:

The long-term Treasury Bond ETF (TLT) is currently in a drawdown of more than 40%. This exceeds the 35% drawdown that high yield bonds (HYG) experienced in 2008 during the financial crisis.

Why It Matters:

High yield bond yields are rising but spreads are not widening. That’s because sovereign yields are rising just as fast. That is a big difference between 2022 and 2008. It’s not just peripheral countries. We are seeing stress in the UK and we are seeing stress in Japan. We are also seeing it in the US, where yields are rising at their fastest pace in 40 years, yield curves are inverting and some Treasuries are trading at 50 cents on the dollar. It’s a risk off environment, but one in which risk off assets are leading the way lower.

This is the video recording of the October 20th, 2022, Weekly Town Hall w/ Willie Delwiche.

10/20/22 2:00 PM ET [Read more…]

From the desk of Willie Delwiche.

Feeling More Like The Financial Crisis

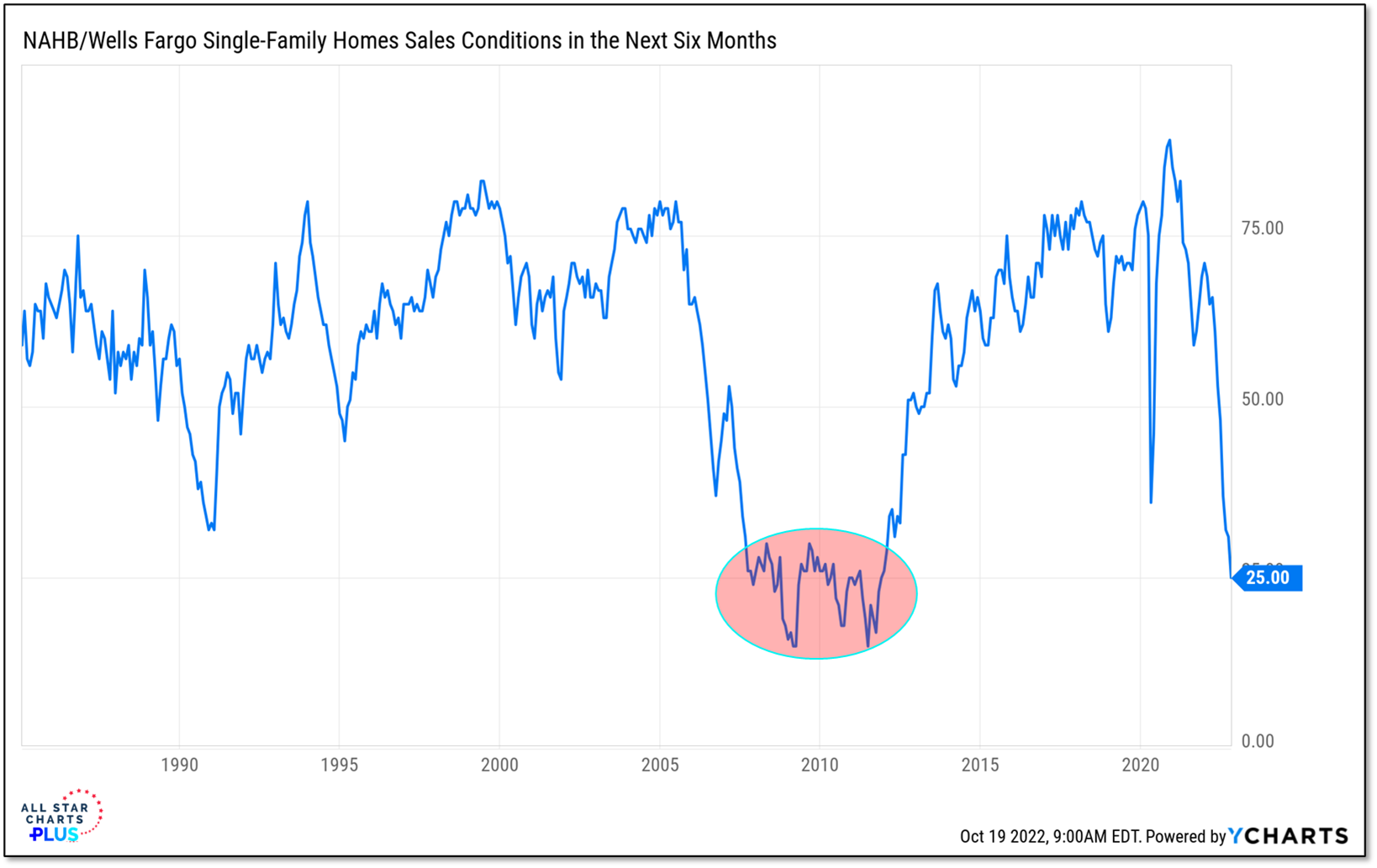

Mortgage rates are soaring and housing market conditions are deteriorating. Sentiment is sour in both the financial markets and the economy.

The Numbers: Expectations for home selling conditions are at a level that have been seen leading up to, through, and in the wake of the financial crisis. This isn’t an isolated report and its both sides of the market. Data from the University of Michigan shows that the fewest survey respondents since the early 1980’s see this as a good time to buy a house (and that was prior to the most recent spike in mortgage rates).

Why It Matters: Economic sentiment, whether on buying houses or CEO confidence, is usually self-fulfilling. This may seem to be at odds with the idea of using sentiment as a contrarian indicator, but it isn’t all that different. We can look at past sentiment extremes to gauge the possibility that moods have moved too far, but it takes bulls to have a bull market in the same way it takes optimism to have an economic expansion.

In this week’s Sentiment Report we take a closer look at the persistent pessimism that can be seen across the market. While the conditions might be ripe for a rally, the longer the bears have the upper hand, the more risk there is to stocks.

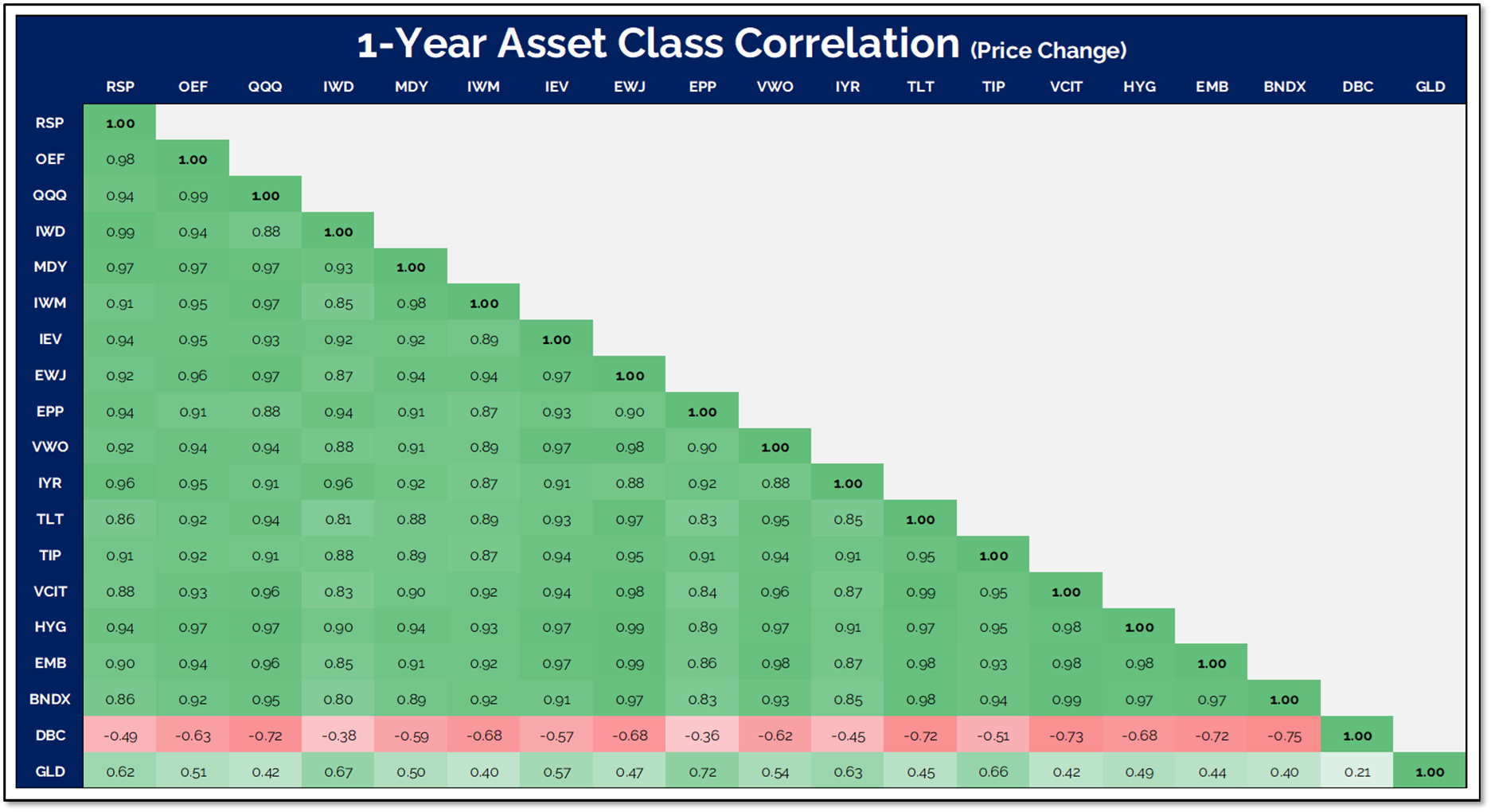

Over the past year, this old Wall Street saying has been more than an adage. It’s been a reality. Correlations across the ETFs that we use as proxies for various asset classes are overwhelmingly positive and on the rise. The exception has been Commodities (DBC), though many asset allocation conversations don’t even include commodities.

Why It Matters: Elevated correlations have left investors with no places to hide as stocks enduring historic levels of volatility and weakness. 2022 has been a risk off environment where risk off assets have been as weak as risk on assets. Trying to navigate this backdrop has led to frayed nerves and impatience for the arrival of better times. Unfortunately this year has done little to show it deserves the benefit of the doubt so far.

In taking a Deeper Look we put 2022 into context, review our indicators of risk behavior and highlight some areas where risk appetite may be improving.