From the desk of Willie Delwiche.

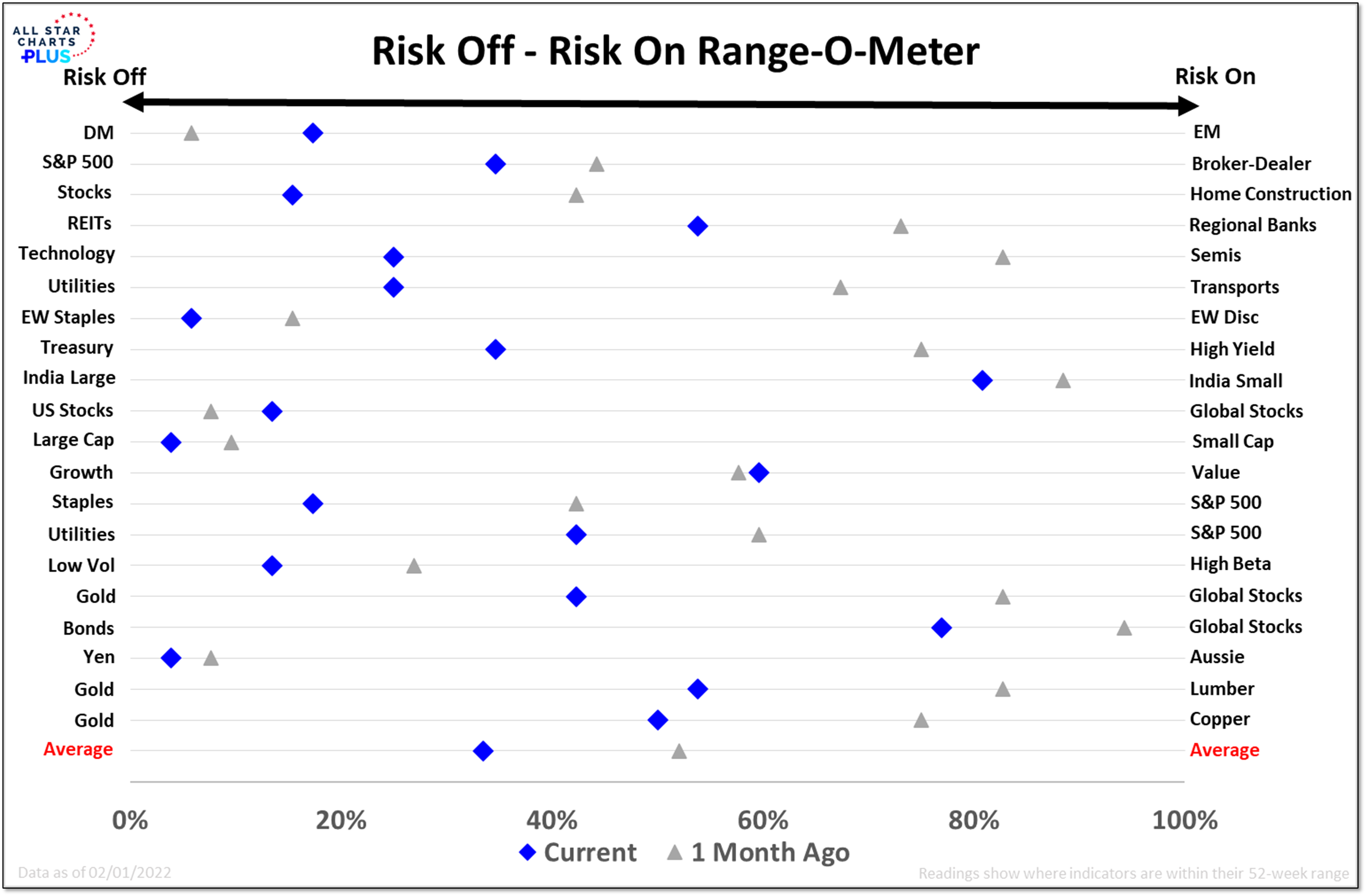

By looking at various ratios relative to where they have been over the past year, we get a sense of investor risk appetite from an intermarket perspective. The pairwise comparisons in our risk off – risk on Range-O-Meter show a decisive tilt toward risk off assets over the past month. A few (Staples vs Discretionary, Large-Cap vs Small-Cap, Yen vs Aussie Dollar) are nearing new 52-week extremes favoring the risk-off side of the ratio. We could get some near-term relief from the intense selling of January, some of that has been seen this week already. But if we are seeing broad and sustainable strength, I expect it will be evident by a decisive move toward the risk-on side of our range-o-meter.

To read the rest of this report, you must be a member of All Star Charts PLUS. Please login below or start your risk-free 30 day trial today.

Lost Password?