When Junk Bond traders jump ship, I’m out of stocks.

With all the talk about credit spreads “blowing out” since early August, this is an important discussion to have right now.

We always trust the bond market. Throughout history, bonds have done an impeccable job at alerting investors about problems in risk asset markets.

When there is stress in other markets, it shows up in fixed income first.

However, as technical analysts, we are mindful of the math that is behind some of the relationships we study and give weight to.

What if I told you that industrials have been massive underperformers during this bull market?

The absolute price chart looks incredible. How could that be?

We call it the denominator fallacy.

Benchmarked against the S&P 500 or Nasdaq 100, of course they are underperforming.

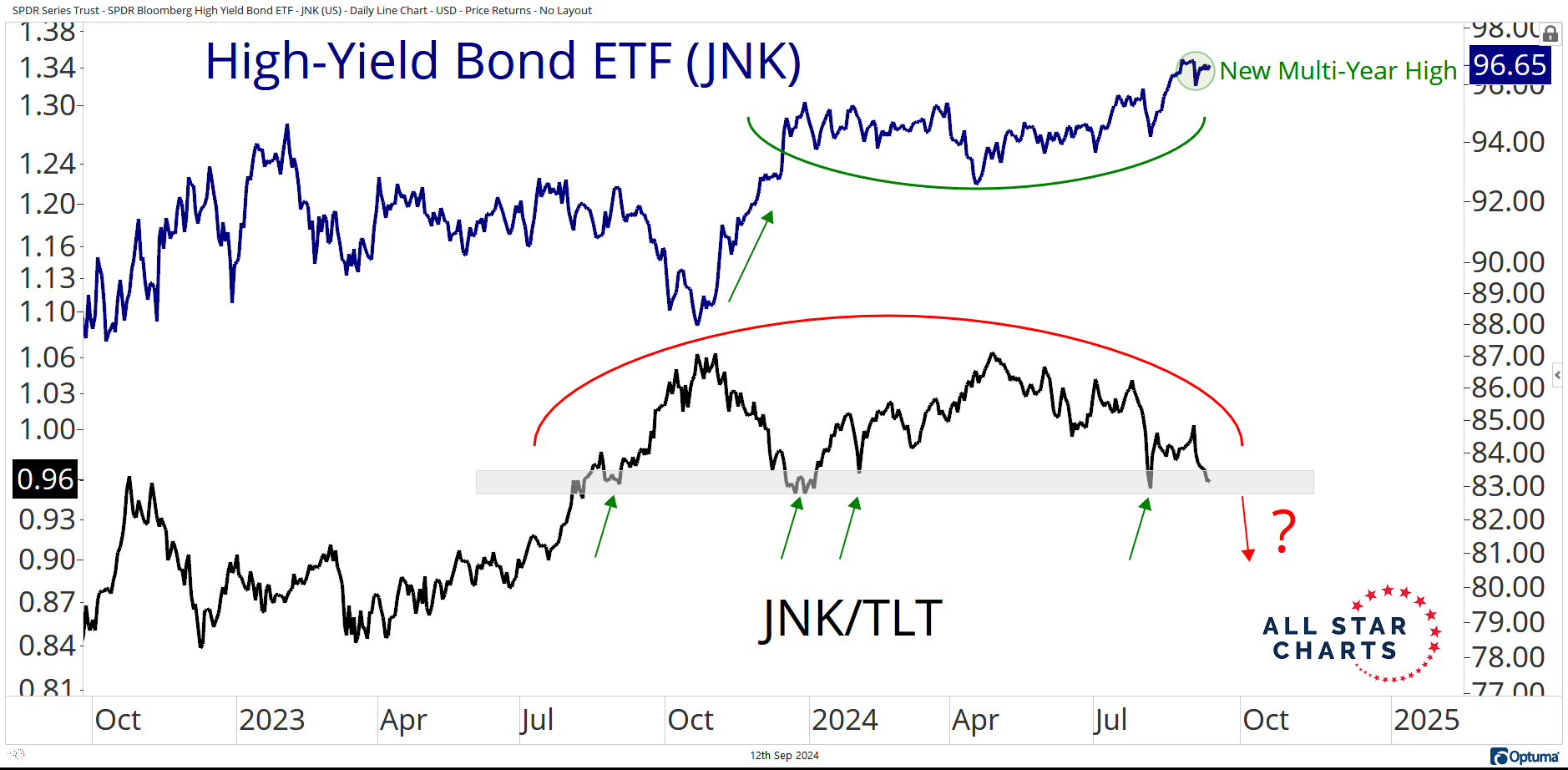

We think there is a similar situation playing out for our bond market ratios right now.

The absolute chart up top looks great. The relative trend, down below, not so much.

So, it’s not weakness in high yield that is driving the bearish action in credit spreads. It’s the strength in treasuries, the denominator in the above ratio.

What really matters is how the riskiest bonds in the world are doing on absolute terms.

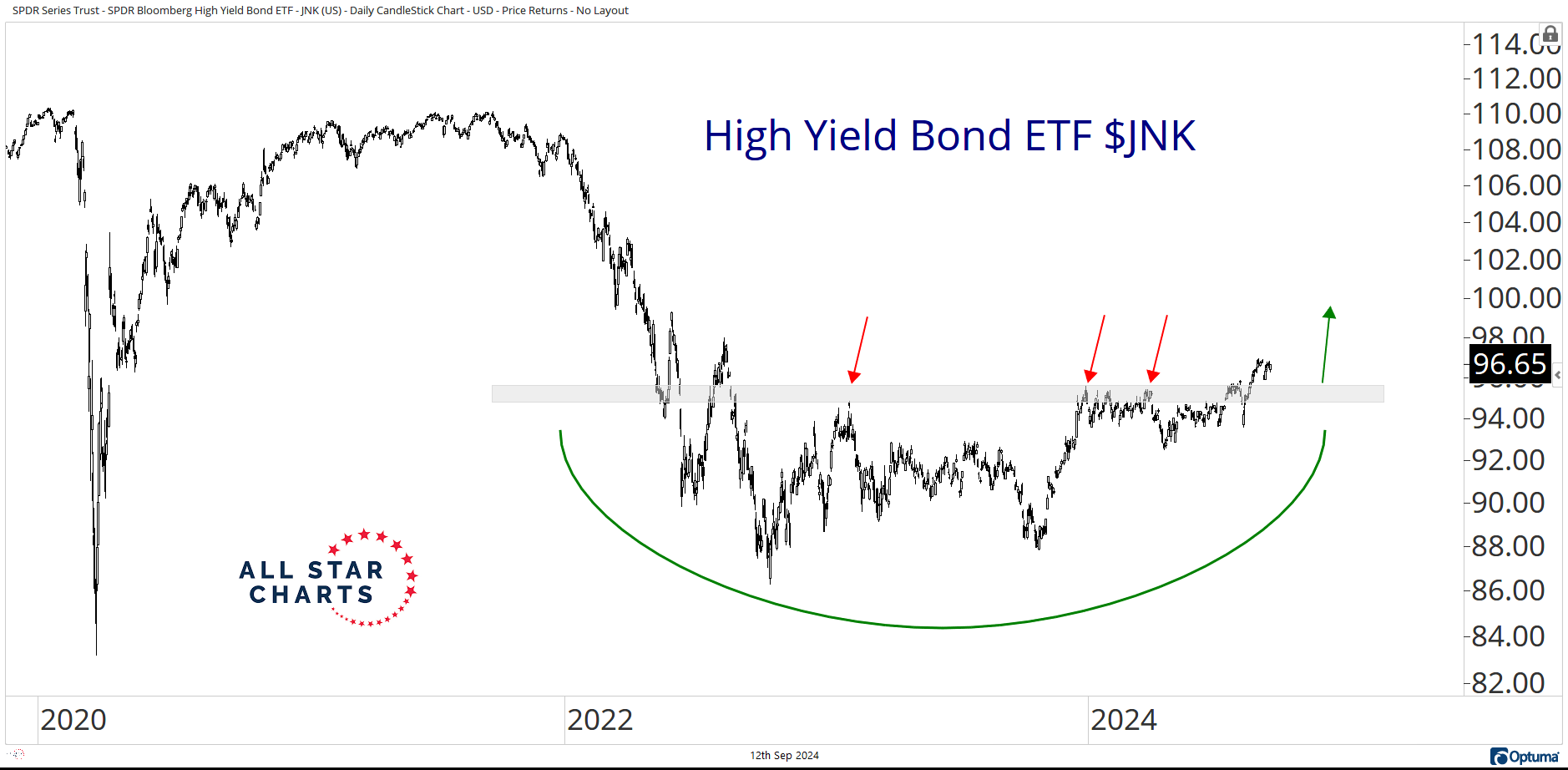

Here is a better look at the SPDR High Yield Bond ETF $JNK completing a trend reversal and making new highs…

Junk Bonds are a powerful 'risk-on' indicator.

This next chart illustrates it:

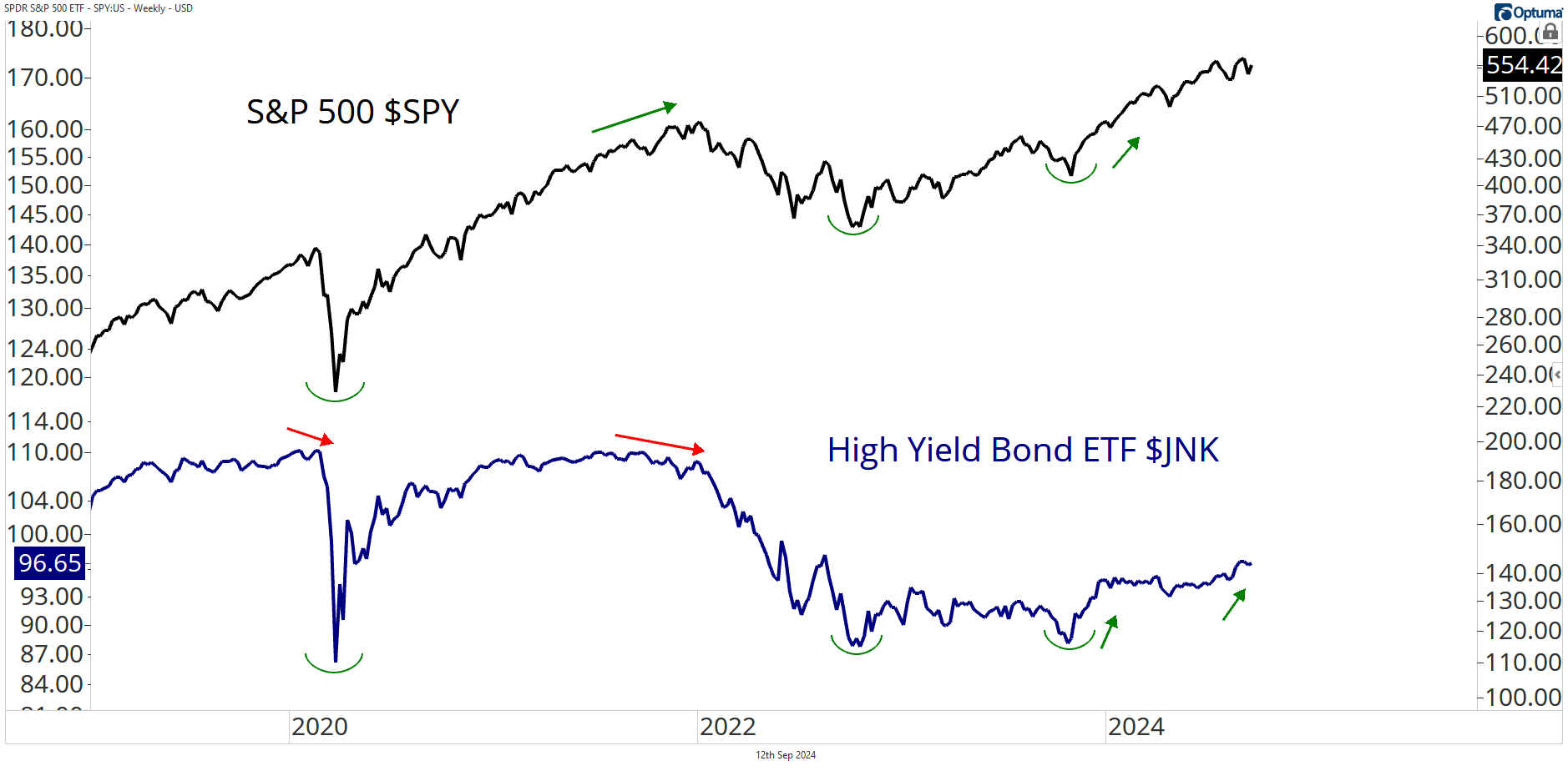

Just look at JNK, moving in the same direction as the stock market over the past 5 years. If we zoomed out further, it would be the same story.

As traders, we can’t look at things in a vacuum and think one thing is terrible because another thing is outperforming. It is information, but it does not tell the whole story.

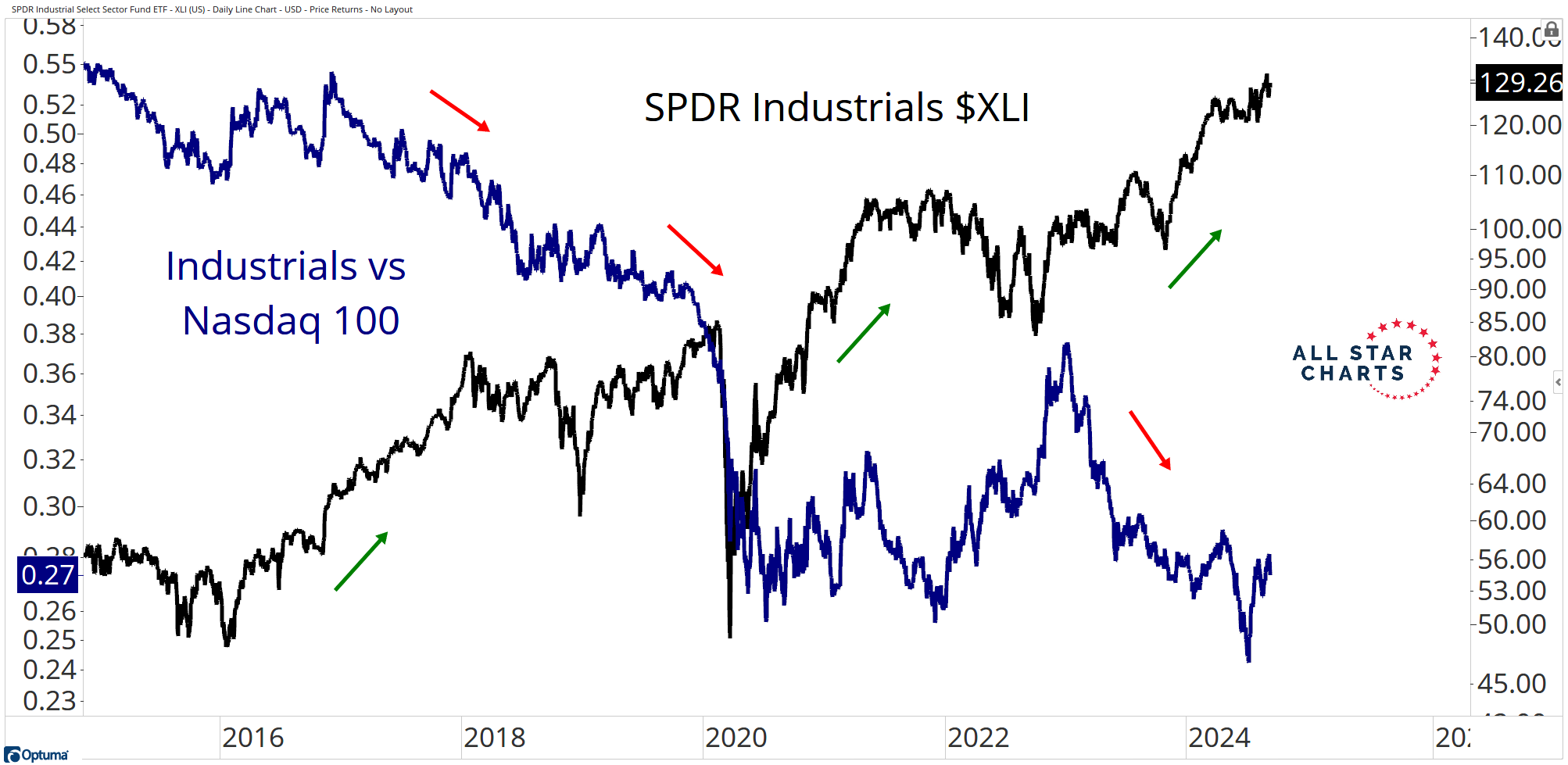

Take Industrials, for example. XLI has been a great investment, steadily moving higher for much of the past decade. The SPDR Industrials $XLI is shown in black below.

However, if we benchmark it against something even stronger, like the Nasdaq 100, it’s been making new relative lows the entire way.

This isn’t about weakness in industrial stocks. It’s about strength in growth stocks.

The same is true for high-yield bonds right now. They are trending well. Just not as well as treasury bonds. And we think that’s just fine.

At the moment, treasuries are like the Nasdaq. Interest rates have peaked and rolled over, and government bonds are resolving primary trend reversals with serious momentum.

Junk bonds are like industrials, and just as industrials are important to the broad market, high yield also gives us some really good information.

Right now, these risky bonds are telling us not to overthink credit spreads… and to stay the course with stocks.

-Allstarcharts Team

Thanks for reading.

As always, be sure to download this week’s Bond Report!

You need to have a subscription to access this content in full.

Log in or subscribe today to unlock new features and receive Member Benefits.