Rates and the US dollar are both catching higher – the opposite of what would likely ignite a precious metals rally.

Yet gold continues to hold above its former 2011 highs!

Despite these setbacks, my bias remains bullish for gold.

But my desire to own the strongest assets is shifting actionable trade setups toward more profitable opportunities…

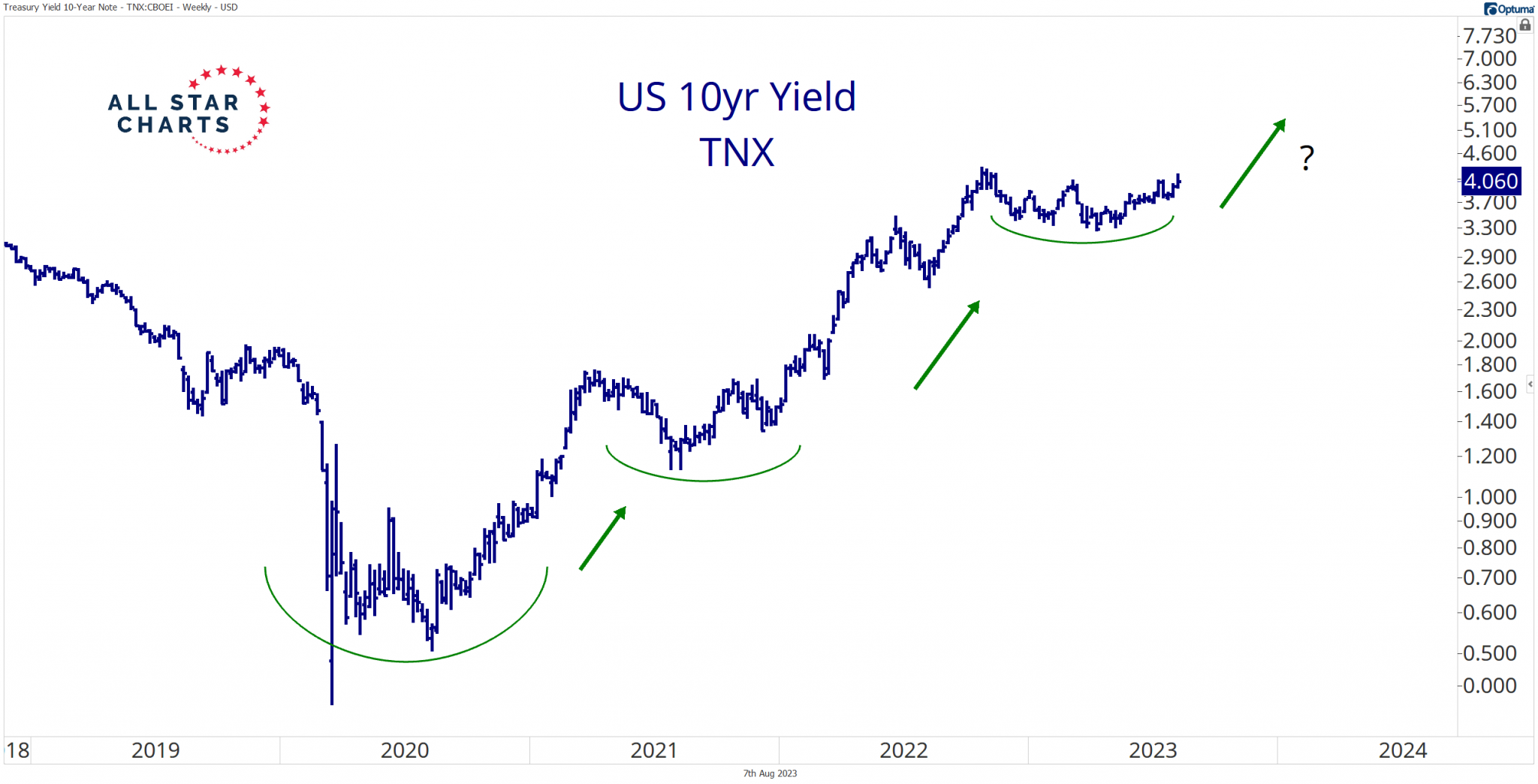

Let’s start at the top: the underlying uptrend in interest rates.

Check out the US 10-year yield:

The 10-year has yet to resolve higher from this basing formation. Nevertheless, the uptrend remains intact as the market has not given investors any reason to bet on lower yields.

As long as yields continue to rise, procyclical areas of the market will offer better returns.

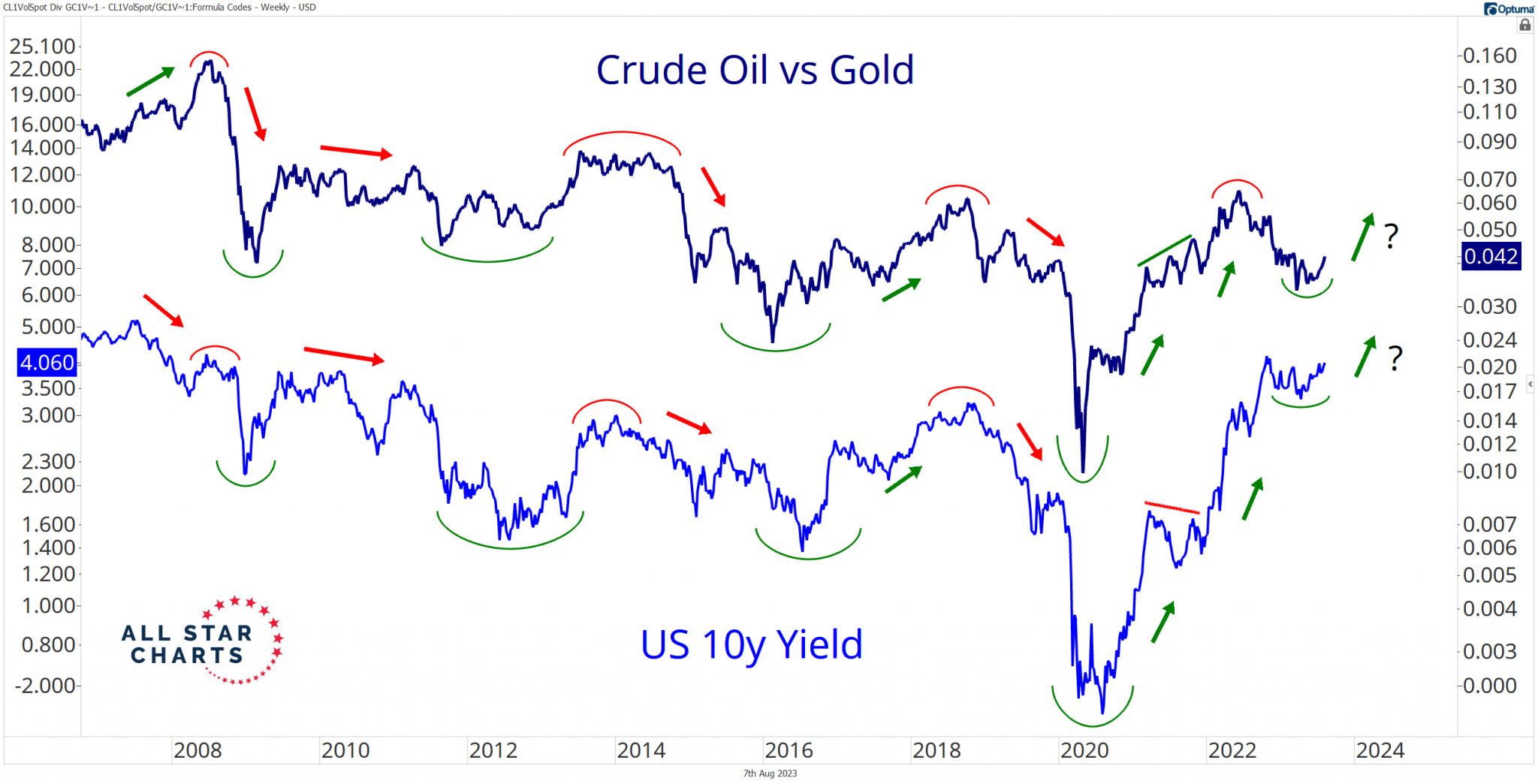

The overlay chart of the 10-year yield and crude oil versus gold tells the story:

Crude oil outperforms gold as rates rise (no wonder I keep finding quality long setups in energy names), while gold shines as rates fall.

Gold can catch higher along with yields. But buy signals in crude oil offer a higher probability of success as rates rise.

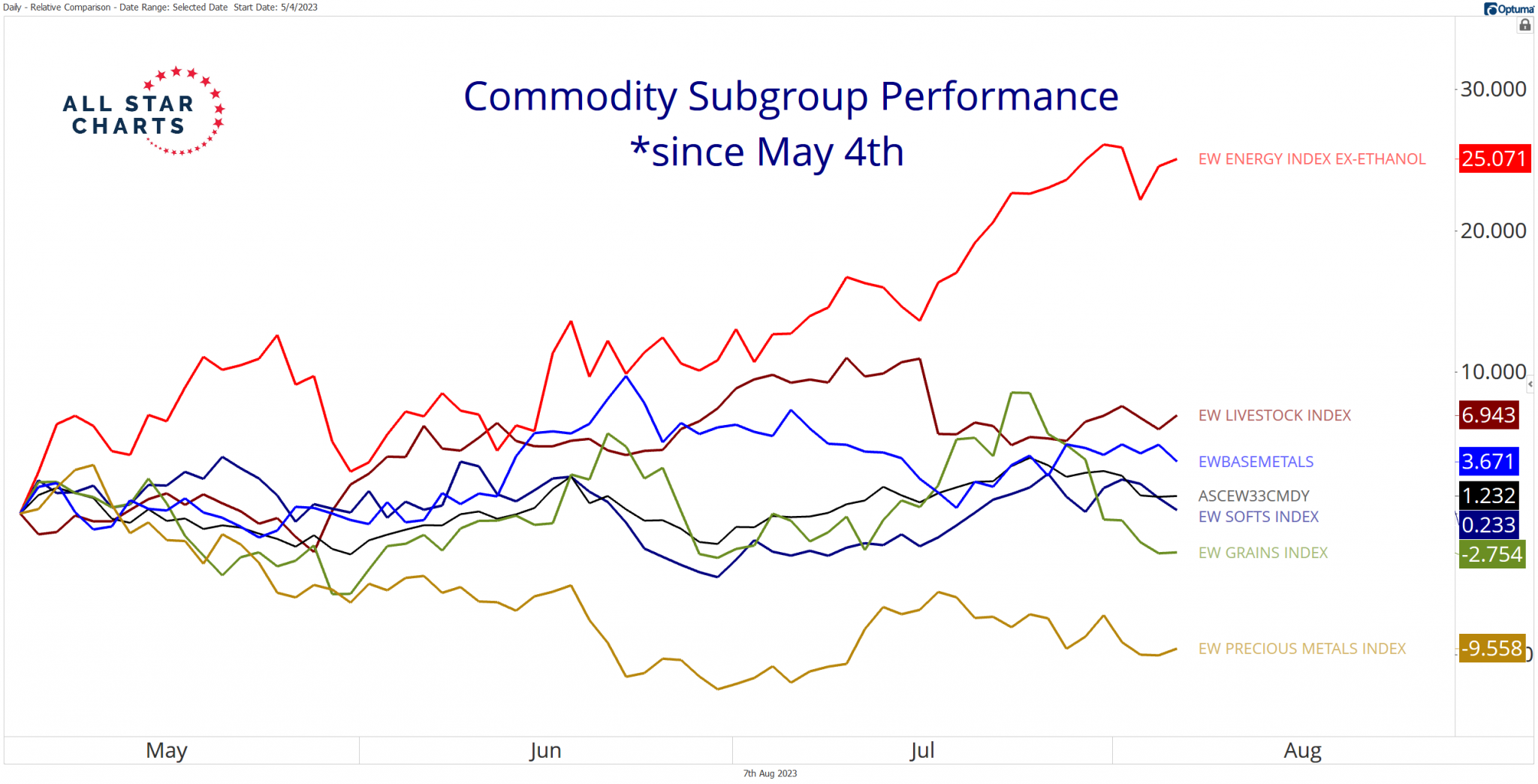

Notice how the commodity group performance has shifted since May 4, when the 10-year yield put in a significant pivot low:

Energy has performed the best, climbing 25% since interest rates marked a local bottom last spring, while precious metals have been the weakest – down almost 10%.

A lackluster summer for gold isn’t enough to flip my structural outlook. But I think it’s safe to say gold has plenty of work to do.

A break below the former 2011 highs places gold futures on high alert. It’s a similar situation for the Gold Miners ETF $GDX as it nears my protective stop.

I still hold a bullish structural view of precious metals, but I refuse to carry positions in metal and mining stocks that are catching lower or chopping sideways while energy names rip higher.

It’s simple: Trading precious metals represents opportunity cost as energy is poised to outperform.

We always want to buy the strongest and sell the weakest. And gold doesn’t fit either description – at least for now.

Gold Rush Report highlights the breakout setups, rotations, and technical signals shaping metals markets — giving traders an edge in gold, silver, and commodities.