This is the video recording of September 3rd 2021 Weekly Jam Session with Sean McLaughlin.

[PLUS] Weekly Town Hall Meeting w/ Willie Delwiche & JC Parets

This is the video recording of the September 2nd Town Hall Meeting w/ Willie Delwiche & JC Parets

09/02/21 2PM ET [Read more…]

Breadth Thrusts & Bread Crusts: In Pursuit of the Unexpected

From the desk of Willie Delwiche.

According to Charles Darwin, you cannot make observations without some kind of underlying theory. And if you have any theories about financial markets, you understand thinking about what could or should happen with your investments.

These concepts can be useful if they help us prepare for what is happening in the markets. But they can also impede or obscure reality.

We can observe and project all we want — so long as we don’t get distracted by the what could and what should that we lose sight of what is.

I don’t see this as an argument in favor of always being bullish or a warning about the risks of needing to be proven right. Instead, it’s an encouragement to agnostically acknowledge and operate within the market as it is rather than as we wish it would be.

It’s about pursuing the opportunities that are before us even when they are unexpected.

Especially when they are unexpected.

[Video] Options Trade of the Week w/ Sean & JC

On September 1st, Sean and JC hopped on a Twitter Live Stream to discuss a recent trade idea for All Star Charts Options Members.

Here’s the play:

“I like an $AMZN February 3800/3900 Bull Call Spread for an approximately $29.00 – $30.00 debit. This means we’ll be long the 3800 strike call and short an equal amount of 3900 strike calls.”

To learn more about the trade and the thinking behind it, click below to watch a replay of the Live Stream. [Read more…]

[PLUS] Weekly Sentiment Report

From the desk of Willie Delwiche.

Key Takeaway: Investors continue to favor stocks as money relentlessly pours into equity ETFs. It’s no wonder, given that the main stock indexes are printing new record highs. Yet, a depressed risk appetite and an unsupportive breadth backdrop accompany the persistent push higher in equities. Though these suspect undercurrents aren’t apparent at the index level, we see signs that short-term attitudes are shifting. Bears are on the rise, with the average of the II and AAII bears trending higher. However, pessimism remains relatively mooted and optimism is still elevated when viewed through either a cyclical or strategic lens. The current environment suggests there is more risk than opportunity for equities from a sentiment perspective.

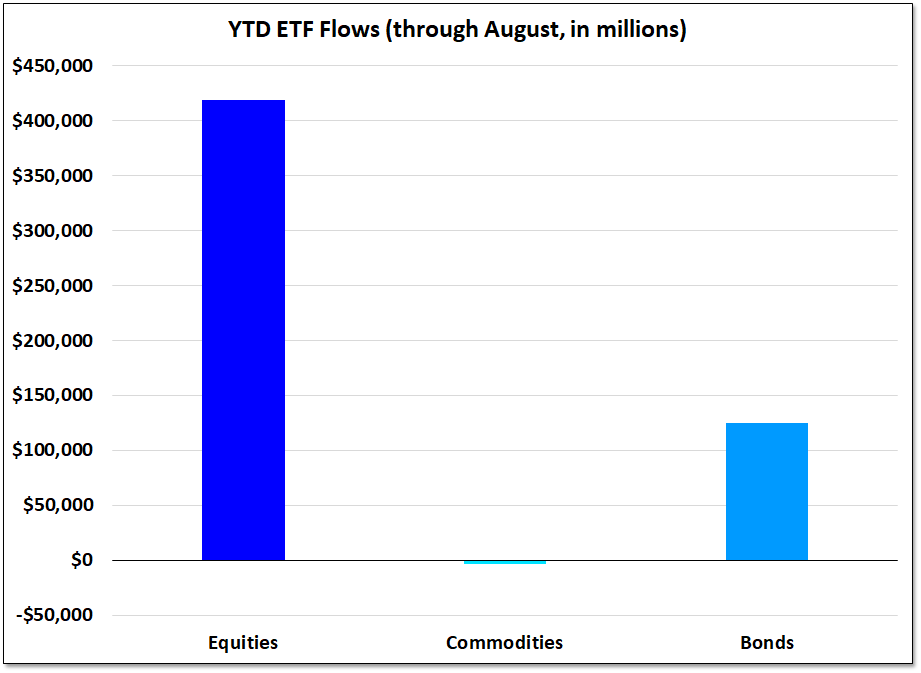

Sentiment Report Chart of the Week: Feel the Flow

Equity ETFs saw another $50 billion of inflows in August, bringing the YTD total to more than $400 billion. This was the 15th consecutive month of inflows for equities (for a total in that time period of more than $600 billion). Commodity ETFs experienced outflows for the second consecutive month in August. Despite YTD gains that surpass stocks (DBC vs SPY), commodities have experienced net outflows in 2021. It’s true that this is driven by flows out of gold (GLD), but that alone speaks to how unloved commodities remain from an asset allocation perspective.

[PLUS] Weekly Market Perspectives – Ready To Get Back In Gear?

Key Takeaways:

- Median stock has gone nowhere for months

- Bond market trusting Powell more than data

- Commodity strength fueled by broad participation

As discussed in yesterday’s Market Notes, last week’s rally has us questioning whether we remain in the choppy market that has been experienced on many levels for the past few months or if we are poised for some degree of resolution to the upside. Today, we’ll take a closer look at what that could mean across stocks, bonds and commodities. As market depth evaporates ahead of the Labor Day weekend, there is no reason to believe that what we talk about has to happen this week.

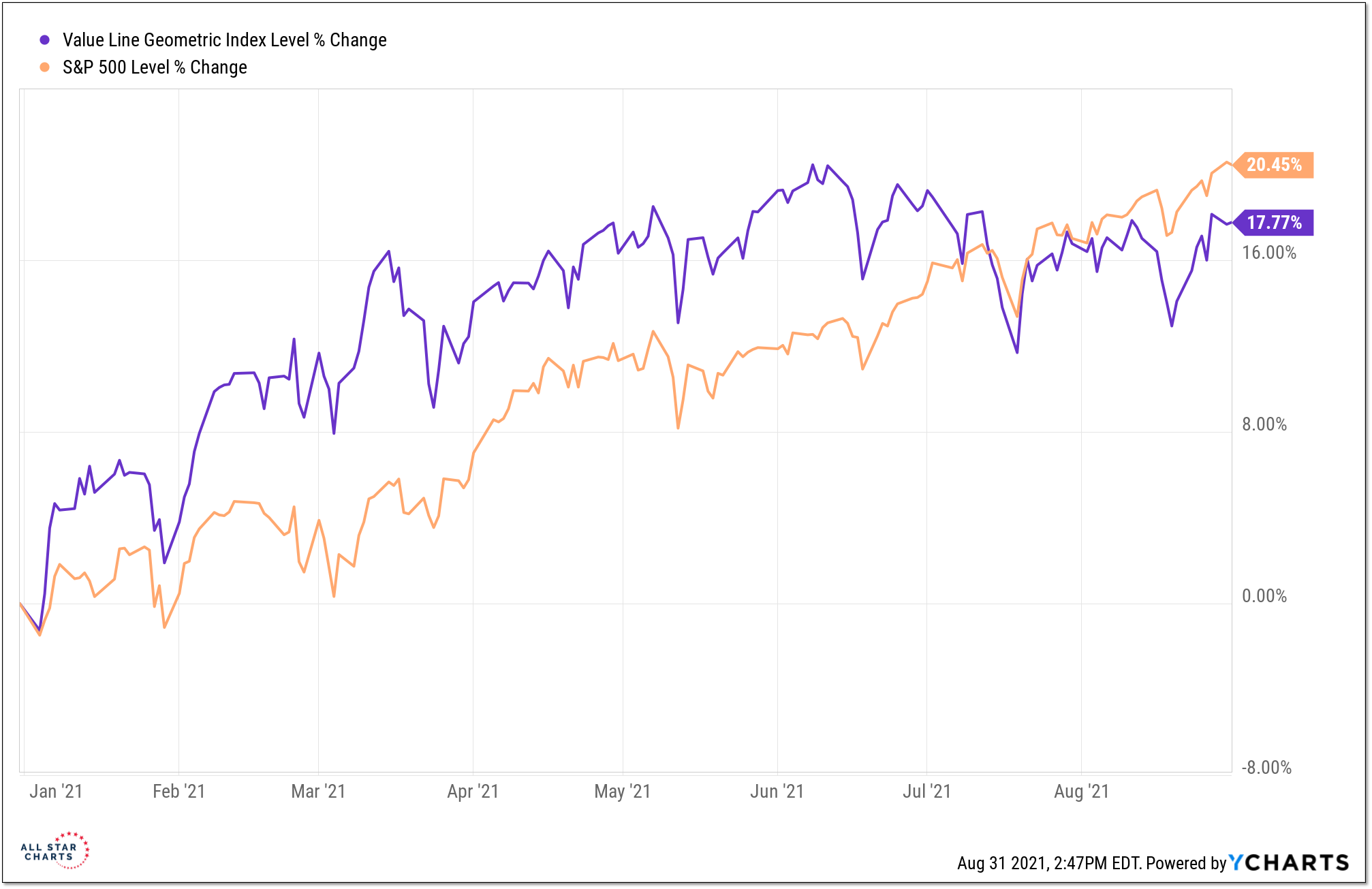

The S&P 500 is getting plenty of press these days for the number of new highs it has made in 2021 (over 50 at this point). I’m more focused, however, on what the Value Line Geometric Index is doing. This index has gone nowhere over the past three months (while the S&P 500 has risen nearly 8%). A new high by this index (and a return to leadership on a YTD basis) would be evidence of the type of broad strength that tends to be sustainable. It’s trying to move in that direction, but there is more work to be done.

[PLUS] Weekly Market Notes & Breadth Trends

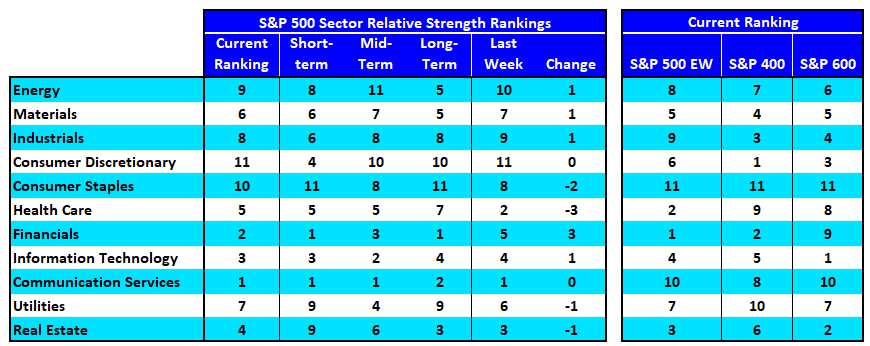

- The Financials sector bounced back in the rankings last week, climbing three spots and moving into the second spot overall. Strength within the sector is broadly based as it is at the top of the rankings from an equal-weight perspective.

- Thanks to FB and GOOGL, the Communication Services sector is in the top spot on a cap-weight basis. On an equal-weight basis it ranks below everything except Consumer Staples.

- At the large-cap level, Transports are near the bottom of our industry group rankings. Mid-caps however, are showing strength and small-caps are improving.

[Video] Options Trade of the Week w/ Sean & JC

On August 25th, Sean and JC hopped on a Twitter Live Stream to discuss a recent trade idea for All Star Charts Options Members.

Here’s the play:

“We’re selling naked short $GDXJ October 39 puts here for an approximately $1.08 credit”

To learn more about the trade and the thinking behind it, click below to watch a replay of the Live Stream.

- « Previous Page

- 1

- …

- 54

- 55

- 56

- 57

- 58

- …

- 79

- Next Page »